{kind=link}

Up to now, 2025 is shaping as much as be a bit higher in the case of mortgage charges.

Whereas the 30-year mounted is just barely under year-ago ranges in the intervening time, it appears to be trending in a greater path in comparison with final 12 months.

It’s at the moment round 6.75%, which is about an eighth under the 6.875% common seen in early March 2024.

However not like again then, mortgage charges may sink additional into spring, as a substitute of rising like they did in April and Might.

And that could possibly be a boon for present owners trying to refinance an present residence mortgage.

Price and Time period Refis Proceed to Achieve as Mortgage Charges Enhance

There are three foremost forms of mortgages – the house buy mortgage, which is self-explanatory.

And the mortgage refinance, which is damaged down right into a price and time period refinance and a money out refinance.

When mortgage charges saved rising and finally hit 8% in late 2023, no one was making use of for a price and time period refinance.

Why? Since you’d solely actually achieve this for those who may acquire a decrease rate of interest within the course of.

That meant the one actual sport on the town, other than some buy lending, was money out refinances, the place present owners had been both consolidating debt or tapping fairness to pay for different bills.

Nonetheless, now that mortgage charges are seemingly falling, and effectively under these scary 8% ranges seen about 18 months in the past, price and time period refinances have made a bit of comeback.

They’ve really been the one vivid spot currently within the mortgage world, with money out refis additionally eeking out some smaller good points as effectively.

Lengthy story brief, these excessive mortgage charges seen over the previous few years have created a chance now that they’re fairly a bit decrease.

Debtors who took out mortgages with charges within the high-7s and even 8s can now commerce them in for one thing extra palatable, like a 6.5% price.

For instance, on a $400,000 mortgage quantity a hypothetical borrower may decrease their principal and curiosity fee by roughly $300 monthly.

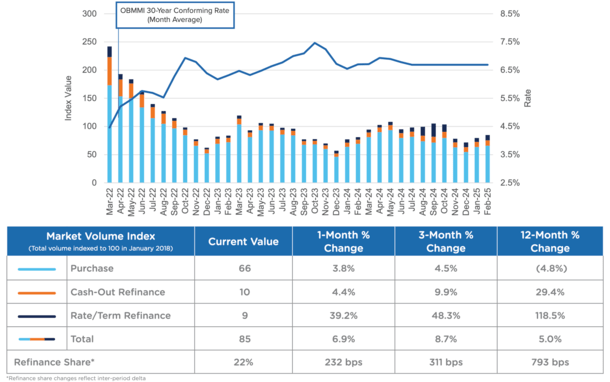

Price and Time period Refi Quantity Up Practically 120% Yr-over-Yr

The most recent Market Benefit report from Optimum Blue revealed that price/time period refinance lock quantity surged almost 40% (39.2%) in February from a month earlier.

And the 3-month change was a good increased 48.3% improve, whereas the 12-month change was a whopping 118.5% improve.

After all, while you take a look at the chart above, you may see that price and time period refis (darkish blue) nonetheless account for a sliver of general mortgage manufacturing.

So whereas they’re having fun with some good proportion good points, they aren’t nearly as good as they appear. However you’ve bought to begin someplace and the current improve is a promising begin to 2025.

As alluded to earlier, if mortgage charges hold trending decrease because the months go by, quantity may actually explode.

For reference, the 30-year mounted was round present ranges final 12 months earlier than turning as much as round 7.50% in April and Might.

It will definitely eased throughout summer time earlier than falling to round 6% on the Fed pivot, which led to an enormous uptick in refinance exercise.

However that was short-lived due to a scorching jobs report, adopted by a Trump presidential victory, each of which propelled charges increased.

Assuming cool financial information continues to come back in, and Trump’s tariffs don’t trigger an excessive amount of hassle (no assure there), charges may revisit these 2024 lows and even go decrease.

If that occurs, there’s a number of pent-up refinance demand ready on the sidelines, presumably some who missed that window final September earlier than charges shot up once more in October.

Sub-6% Mortgage Charges Might Add Tens of millions of Refinance Candidates

When mortgage charges hit 6.125% in September, the in-the-money refinance inhabitants jumped by about 1.3 million, per a report from ICE on the time.

Had charges continued to fall, to say 5.75%, one other two million refi candidates would have materialized.

And if charges went down to five.5%, which many seek advice from as a magic quantity for residence purchases, one other 1.2 million extra.

In different phrases, it could be attainable to unlock three million or extra refinances if/when the 30-year mounted falls again to the mid-5s, which is trying like an actual chance this 12 months.

That would lastly make refinances account for an honest share of general lock quantity once more, as a substitute of merely seeing huge proportion good points from rock-bottom ranges.

On the similar time, if low mortgage charges are pushed by a recession, you may need a scenario the place residence buy lending falls, regardless of improved affordability.

Merely put, decrease demand due to fewer eligible residence patrons means much less residence gross sales.

That too may push up the refinance share of the market, which stood at simply 22% in February.

It was as excessive as 32% final September, so if mortgage charges fall under these ranges, it wouldn’t be unreasonable to see refis seize a 40% share once more.

And that would make 2025 the 12 months of the speed and time period refinance after a tricky few years.

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on X for decent takes.