{kind=link}

Working with people and {couples} provides me a front-row seat to how individuals make investments. The view is fascinating.

A number of shoppers have labored with different advisors. Some include collections of high-cost actively managed mutual funds, annuities, and life insurance coverage merchandise they have been bought. Others include dozens or extra mutual funds and ETFs. Some have tons of of particular person shares. It’s nearly like I may predict how their advisors have been paid by their investments.

Some individuals have been DIY buyers. Portfolios typically appear like a stroll down reminiscence lane of current funding traits: one or two I Bonds, shares of ARKK ETF, a handful of particular person tech shares, a number of random cryptocurrencies, and so on…. And solely imprecise explanations of why they personal what they do and the way the items match collectively.

Some individuals admit they began investing, usually of their work retirement plans, with little schooling or steerage. They are often in all places. One portfolio included each accessible goal date fund in a 401(okay) for diversification.

The widespread denominator in each consumer I’ve seen is that we spend important time simplifying their funding portfolio. Listed below are 5 arguments for simplifying your investments.

Simplicity Works

Let’s begin with crucial, and least intuitive, cause to simplify your investments. Simplicity works. This isn’t intuitive as a result of it doesn’t work in just about some other space of life.

Easy Funding Approaches Aren’t Intuitive

Wish to enhance your health? Eat effectively. Train usually. Enhance sleep. Handle stress. All should be carried out with ongoing diligence.

Wish to enhance your relationship? Work on communication. Make high quality time to your companion. By no means neglect the connection.

Wish to advance in your profession? Improve data. Develop new abilities and refine outdated ones. Increase your social community. Sitting again and ready for issues to return to you just about by no means works.

Wish to get higher funding outcomes? Select a easy technique consisting of some low-cost, tax-efficient, broadly diversified index funds/ETFs. Find them in probably the most tax-efficient accounts. Automate it. Then go reside your life. The much less you do, the higher!

Which of this stuff is just not like the opposite? It is smart why that is onerous for buyers to understand.

Proof for Easy Investing

Including to investor’s skepticism of simplicity are two whole industries, funding “advisors” and the monetary press, whose existence depends upon the phantasm of complexity. William Bernstein describes this because the fourth of his 4 Pillars of Investing which he calls The Enterprise of Investing.

Content material that promotes complexity is unending. Regardless of this noise, proof constantly reveals that simplicity works in investing.

SPIVA publishes an annual report evaluating the efficiency of actively managed mutual funds in opposition to their index benchmarks. 12 months after 12 months, throughout areas and asset lessons, actively managed funds underperform.

Performed out over 15-20 years, the percentages improve to larger than 90% in favor of the index. That is true throughout geographic areas and segments of the market.

Current analysis reveals that throughout the index, the overwhelming majority of returns are derived from a tiny variety of shares. The highest 4% of shares create primarily all inventory market returns. The underside 96% cumulatively creates returns roughly equal to T-bills. The median inventory has a destructive return.

It appears logical to simply decide these successful shares. But this has proven to be elusive for the overwhelming majority of buyers.

All this helps John Bogle’s maxim, “Don’t search for the needle within the haystack. Simply purchase the haystack.” This may be achieved with a easy funding strategy of shopping for a number of broad-market index funds and ETFs and calling it a day.

There Are Many Higher Makes use of of Your Time

Complexity reigns in just about all areas of economic planning. There are areas the place you possibly can enhance outcomes by investing time, vitality, and energy.

The US doesn’t have retirement, tax, or well being care “methods.” As a substitute, every is ruled by legal guidelines that have been applied piecemeal over time.

That complexity has solely elevated with all the laws, a lot handed in haste, that got here out of the pandemic. Efforts to grasp key particulars are use of your time.

Even comparatively secure and efficient authorities packages like Social Safety are advanced. Effort is required to develop a framework to assist resolve when to say advantages. Even for those who perceive the fundamentals, this system comprises quite a lot of jargon. Thus it is very important spend time understanding terminology to keep away from pointless errors.

Creating a system to funds or monitor spending is important. This offers insights into whether or not your spending is sustainable and aligned along with your values. Whereas not technically troublesome, this takes ongoing effort and time.

Backside line, many duties require substantial time, effort, and vitality to supply the very best outcomes. Investing doesn’t. Why waste time on complexity that’s pointless at greatest and sometimes detrimental when that point might be higher spent elsewhere?

Your Companion Doesn’t Care About Your Ardour for Investing

A standard sample in {couples} I work with is for one companion to be an investing “fanatic” whereas the opposite is essentially disinterested. A easy strategy of some broad-based index funds is an ideal resolution.

Each companions can perceive and, if wanted, implement this straightforward strategy. Concurrently, it can outperform most different investing methods over the long run.

The disinterested companion usually grasps this and is fast to purchase in. But it’s the investing fanatic, sometimes the one who sought my recommendation within the first place, who pushes again in opposition to the advice of a easy portfolio.

In case you are that particular person in your relationship, I current a number of questions:

- Do you perceive that you’re placing your monetary targets, AND these of your companion, in danger primarily based in your hunch about choosing particular person shares, investing in your good friend or neighbor’s undertaking, or your thesis about cryptocurrencies?

- If one thing occurs to you, what is going to your companion do with the advanced portfolio you’ll depart them?

- Are each companions absolutely conscious and comfy with this?

What If You’re Proper?

Some individuals prefer to set a small portion of the portfolio apart for speculative investments. It’s enjoyable for them.

They will restrict this to a small share of the portfolio they might afford to lose in the event that they’re incorrect. They argue that in doing so there may be little draw back and large upside.

However what for those who’re proper….for some time? As famous above, beating the market is difficult over lengthy intervals. It’s more easy for brief intervals.

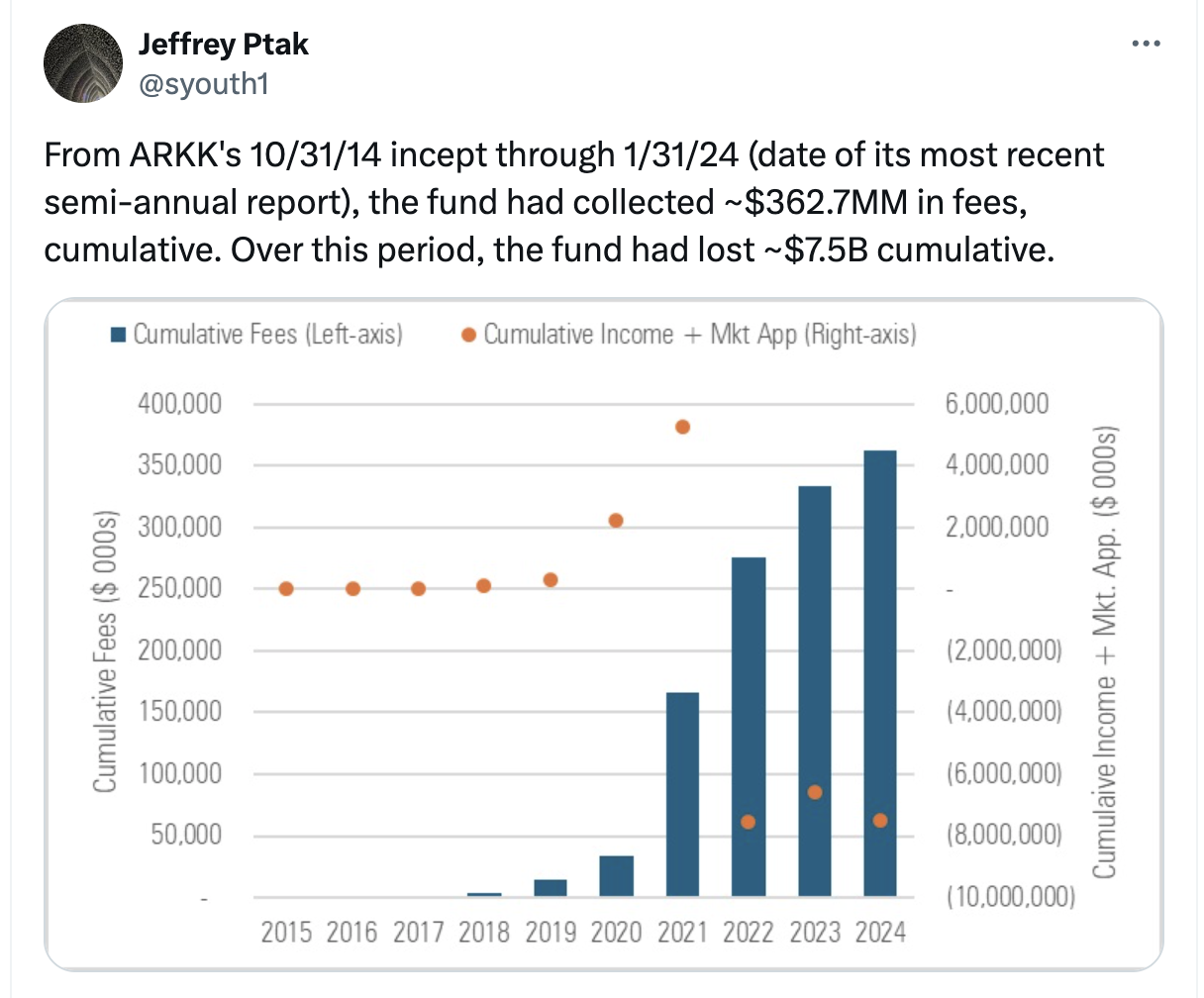

A couple of years in the past, ARK Innovation ETF (ARKK) had an unbelievable four-year run between 2017 and 2020. In 2020 alone it returned 153%. The fund and its star supervisor, Kathie Wooden, attracted large consideration within the monetary press and super inflows of property. Fund house owners needed to be feeling very good.

Since then, returns have been a bit much less stellar: -23% in 2021 and -67% in 2022. This led to large losses for shareholders. Morningstar’s Jeffrey Ptak lately posted the next astounding statistics on this fund.

Once you complicate your portfolio with speculative investments, one danger is underperformance. This may be managed by limiting your publicity.

What for those who get fortunate, complicated that for talent? An even bigger potential danger could also be a brief interval of overperformance.

Would you observe a disciplined rebalancing plan to reap your outperformance? Or would you be tempted to double down in your methods? Don’t underestimate this danger!

Future You Will Thank You

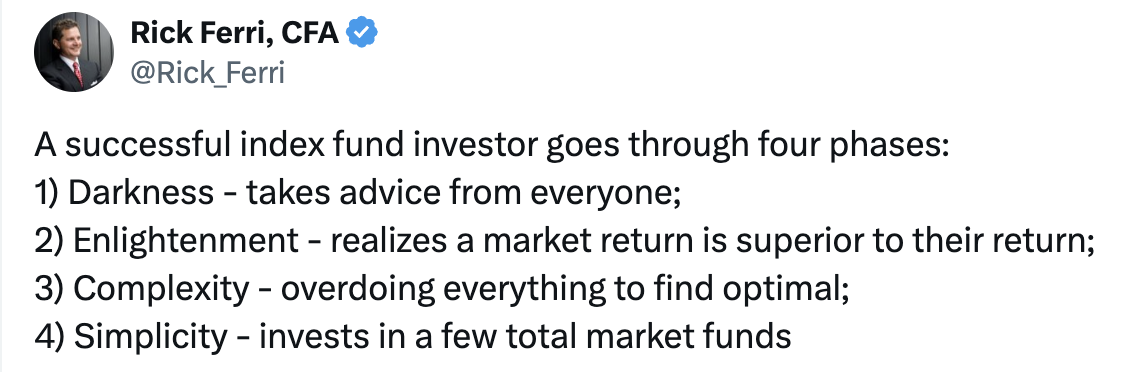

Rick Ferri has a saying in regards to the phases each index fund investor goes by means of. In my brief time working with shoppers, I’ve come to understand these insights:

Folks generally come to me as they strategy or navigate early retirement with questions on optimizing ACA tax credit or contemplating Roth IRA conversions. They’re stunned to study that earlier funding selections may restrict their choices.

Some individuals have collections of actively managed mutual funds or balanced funds of their taxable accounts. These funds kick off pointless taxable earnings within the type of capital good points and/or certified dividends that fill their decrease tax brackets.

Others include a handful of extremely appreciated particular person shares. These shares current a major focus danger if they aren’t diversified, however create a tax bomb if they’re bought off to diversify.

In both case, it may take years to unwind the implications of earlier funding selections made (or bought to you) in what Ferri calls section one and section three.

In case you are studying this weblog and different sources like this, you’re seemingly no less than someplace between phases one and two. Get your self to section 4 as rapidly as potential. The longer term you’ll thank the present you!

* * *

Worthwhile Sources

- The Finest Retirement Calculators can assist you carry out detailed retirement simulations together with modeling withdrawal methods, federal and state earnings taxes, healthcare bills, and extra. Can I Retire But? companions with two of the very best.

- Monitor Your Funding Portfolio

- Join a free Empower account to achieve entry to trace your asset allocation, funding efficiency, particular person account balances, internet price, money circulate, and funding bills.

- Our Books

* * *

[Chris Mamula used principles of traditional retirement planning, combined with creative lifestyle design, to retire from a career as a physical therapist at age 41. After poor experiences with the financial industry early in his professional life, he educated himself on investing and tax planning. After achieving financial independence, Chris began writing about wealth building, DIY investing, financial planning, early retirement, and lifestyle design at Can I Retire Yet? He is also the primary author of the book Choose FI: Your Blueprint to Financial Independence. Chris also does financial planning with individuals and couples at Abundo Wealth, a low-cost, advice-only financial planning firm with the mission of making quality financial advice available to populations for whom it was previously inaccessible. Chris has been featured on MarketWatch, Morningstar, U.S. News & World Report, and Business Insider. He has spoken at events including the Bogleheads and the American Institute of Certified Public Accountants annual conferences. Blog inquiries can be sent to chris@caniretireyet.com. Financial planning inquiries can be sent to chris@abundowealth.com]

* * *

Hyperlinks on this web site, just like the Amazon, Boldin, Pralana, and Private Capital hyperlinks are additionally affiliate hyperlinks. As an affiliate we earn from qualifying purchases. When you click on on considered one of these hyperlinks and purchase from the affiliated firm, then we obtain some compensation. The earnings helps to maintain this weblog going. Affiliate hyperlinks don’t improve your value, and we solely use them for services or products that we’re acquainted with and that we really feel might ship worth to you. In contrast, we’ve restricted management over a lot of the show adverts on this web site. Although we do try to dam objectionable content material. Purchaser beware.