When discussing the most effective investments for Canadian retirees it’s necessary to grasp upfront that it’s a nuanced matter. There is no such thing as a one-size-fits-all silver bullet reply that may match everybody.

I personally advocate trying out this retirement course that I gave suggestions to the creator on (Kyle writes right here at MDJ as properly). I additionally advocate studying these articles so as to get the total vary of retirement funding choices:

Now it’s time to speak in regards to the nuts and bolts of construct the most effective retirement portfolio in your particular wants. In different phrases, what precise investments to place inside your TFSA and RRSP (or RRIF).

In case you’ve been following my writing right here on MDJ through the years you received’t be shocked to study that I believe Canadian dividend shares and easy Canadian ETFs are the most effective investments for many Canadian retirees. (And most Canadians of any age, actually.)

That stated, I suppose as I get nearer to retirement myself, I assumed it is likely to be value it to dive into the specifics across the precise mechanics of dealing with a retirement portfolio, and what the assorted funding choices are. To be trustworthy, I don’t need to spend so much of time speaking about unique stuff like investing in gold, or numerous cryptocurrencies. I wouldn’t advocate these kinds of investments to anybody – not to mention retirees who’re normally extra risk-averse.

Are You Saving Sufficient for Retirement?

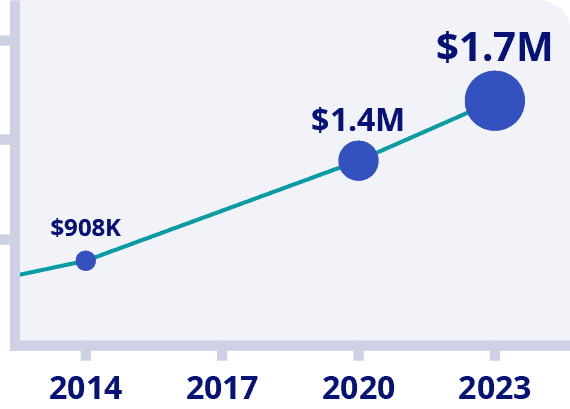

Canadians Consider They Want a $1.7 Million Nest Egg to Retire

Is Your Retirement On Observe?

Change into your individual monetary planner with the primary ever on-line retirement course created solely for Canadians.

Strive Now With 100% Cash Again Assure

*Information Supply: BMO Retirement Survey

Why Actual Property Isn’t the Greatest Funding in Retirement

And whereas I do know that many Canadians have had good luck with shopping for actual property over the previous few a long time, I don’t suppose that’s an excellent funding for Canadian retirees. Right here’s my main reasoning:

- Utilizing loads of leverage to take out a mortgage on a rental property might be very dangerous (as Canadians who bought houses the final couple of years are discovering out proper now).

- The chance of getting a lot of your wealth tied up in 1-3 single homes may work out – however it’s additionally a recipe for catastrophe. All of it is determined by the provision and demand of 1 single neighborhood in a single metropolis.

- The complications of being a landlord get much less and fewer enjoyable as you grow old.

- Canadian housing costs are nonetheless amongst the very best on the earth, even after dropping steam in 2022. I simply don’t see how the asset continues to develop in worth almost as quick because it has been.

- The revenue generated just isn’t tax environment friendly in any respect.

Now in order for you publicity to a broader class of Canadian actual property, you may test our Greatest Canadian ETFs article for extra on which REIT ETFs caught our curiosity.

Like I stated, I do know that it has labored for lots of people through the years – and you probably have a portfolio higher than $2 million or so, then the chance in shopping for an funding property isn’t fairly as magnified – however I simply don’t suppose it’s blanket advice in relation to Canadian retiree investments.

Ought to Canadian Retirees Be within the Inventory Market?

Sure! Canadian retirees needs to be invested within the inventory market!

I’m all the time amazed by what number of of us over the age of 55 are fearful of proudly owning items of the most important corporations on the earth. The reality of the matter is that once you have a look at the longevity statistics for Canadian {couples} as of late, there may be roughly a 50% probability that you simply’ll dwell to be 90-years-old (particularly when you’re feminine or within the prime 30% of Canadians in relation to web value).

Meaning that there’s a excellent probability that both you or your partner can be withdrawing out of your portfolio for 4 a long time! That’s a fairly stable time horizon to just accept some threat.

Now, that stated, how a lot threat to just accept is admittedly the hardest resolution to make in relation to investing. If all of us agree that we will take a few of the week-to-week volatility out of a portfolio utilizing fastened revenue investments like GICs or bonds, then the query turns into, simply how a lot threat is there in relation to a retirement portfolio that features numerous mixtures of shares and bonds?

(We’ll get into the most effective methods for a retiree to truly make these investments in only a second.)

A variety of sensible individuals declare {that a} good rule of thumb in relation to a retiree’s funding portfolio was: “100 – (your age) = the proportion of your portfolio you must have in fairness”.

So when you have been 60 years outdated, and had a $500,000 portfolio, then you can have $200,000 invested in shares/equities, and $300,000 invested in fastened revenue like bonds or GICs. As you grow old, you’d need to proceed to tilt extra in the direction of fastened investments.

Personally, I might think about {that a} very, very conservative option to deal with my investments. I’ve been satisfied that one needs to be far more open to investing in shares in retirement by the in depth work that Karsten Jeske has completed over on the Early Retirement Now. “Massive ERN” has conclusively confirmed that over longer intervals of time (corresponding to 20+ years) shares are usually not extra dangerous than bonds.

Consequently, I believe it is sensible to have far more of your web value in shares than the normal guidelines of thumb enable. I definitely intend to take action in my very own retirement portfolio.

Now that stated, threat just isn’t a straightforward idea to internalize. Whereas the maths may present that shares make sense as a retirement funding, it doesn’t essentially assist remedy the behavioral pitfalls that people are susceptible to.

Retirees have extra time to consider their funding portfolio, and they’re extra targeted on the day-to-day actions. Which means that the big actions we generally see in shares (40% down in a yr for instance) can really feel further painful.

If you’ll lose sleep and really feel loads of stress when the inevitable market downturns happen, then it is advisable just remember to have deliberate for that – in any other case you’re assured to really feel a ton of strain to promote your shares on the worst attainable time (when the market is on the backside). Consequently, it is advisable decide your individual threat tolerance in relation to inventory/bond allocation.

For me, I believe 90%+ shares is more likely to be the most effective match all through my retirement. I believe loads of different individuals could be extra snug with 60% shares and 40% bonds or utilizing the bonds/age rule of thumb mentioned above.

Retirement Earnings Utilizing “Funding Buckets”

You will notice loads of consultants on the market advocate the concept of splitting up your retirement funding portfolio into three “psychological buckets”.

The concept behind these buckets is that it may reassure you that you’ve sufficient protected retirement investments for the subsequent 1-5 years, whereas additionally making use of the long-term returns related to the inventory market. Right here’s a have a look at one mannequin of this retirement bucket funding technique:

Bucket 1: I Want the Cash This 12 months

This cash needs to be in one in all our Canadian Excessive Curiosity Financial savings Accounts. You’ll want it within the subsequent few months to pay your day-to-day payments, so that you need it “liquid” and readily accessible.

Bucket 2: I Want the Cash Within the Subsequent 5 Years

Often I’d say this cash needs to be in bonds or bond ETFs, however I believe that given how excessive Canadian GIC charges are proper now, GICs truly take advantage of sense.

The concept right here is that the inventory market usually goes down for 1-5 years at a time – so that you don’t need to be pressured to unload your riskier investments at a foul time. Consequently, what you must do is create a “fastened revenue ladder” the place you identify your spending wants every year, after which put that a lot cash in a 1-year GIC, a 2-year GIC, and many others.

Annually, when your GIC matures, you simply take that cash and roll it proper into your excessive curiosity financial savings account for spending functions.

Bucket 3: Your Shares – I Want the Cash In 5 or Extra Years

Shares (aka: equities) are the riskiest funding in most retiree’s portfolios. They’re for the long run, and also you don’t need to be pressured to promote them on the flawed time. Most years (about three-quarters of the time) shares acquire in worth. However there have been years when shares are down 40% or so. These might be scary years when you want cash ASAP!

Now these buckets don’t all correspond properly to what needs to be in your RRSP and TFSA, so to completely optimize this technique, I like to recommend re-reading Kyle’s primer on withdrawing out of your RRSP, TFSA, and non-registered accounts in retirement.

There may be nothing horrible about this retirement bucket funding technique. If it helps you sleep at night time, and allows you to keep on with your plan – then I believe it’s a good suggestion. That stated, I don’t imagine that it’s the optimum answer.

Once more, Mr. Jeske’s analysis and reasoning has led me to the conclusion that funding buckets aren’t (mathematically talking) the easiest way to go.

Now – it bears repeating – math doesn’t take behaviour under consideration. An important consideration to make when taking a look at what share of your retirement portfolio to have in equities, and the way a lot to have in fastened revenue, is that you simply perceive your self, and your response to what you is likely to be taking a look at in a 2008-type of situation for shares.

Okay, with that warning in place, we truly see from Jeske’s analysis that shares are usually not the truth is riskier over the long run. So for me, personally, I’ll seemingly solely have two buckets:

1) The money I’ll want this yr – which I’ll put in a excessive curiosity financial savings account.

2) My long-term investments. These will nearly assuredly be all shares. Provided that I’ve a excessive publicity to Canadian dividend shares in my non-registered portfolio (together with my Smith Manoeuvre investments), I’ll seemingly spend the dividends that I obtain every year first, after which make additional liquidity choices from that time.

Slicing Charges On Your Canadian Retirement Portfolio

When you’ve determined in your private finest investments for a Canadian retiree, the subsequent two questions turn out to be:

1) How do I purchase and maintain these investments for the bottom attainable value?

2) If I need to make it just a little simpler, am I ready to pay just a little extra?

In case you’re a longtime MDJ reader then you recognize that I preserve our Greatest Canadian On-line Brokers article up to date month-to-month, and that buying your individual shares, bonds, and ETFs by way of a dealer is the bottom value option to make investments.

Proper now, my favorite on-line dealer (Qtrade) has an impressive RRSP season promotional provide:

With Qtrade, you get a really beginner-friendly platform that may mean you can purchase and promote ETFs at no cost. Your dividend shares will value you a couple of dollars each time you purchase and promote them.

A Fast MER Charges Rationalization

Administration Expense Ratios (MERs) are an important quantity to grasp in relation to investments for retirement.

MER charges are form of awkward for Canadians to grasp, as a result of we’re used to paying for issues in Canadian {Dollars}. We go to the dentist and we pay a pair hundred {dollars} for a cleansing. We go to a lawyer they usually inform us the associated fee can be $250 per hour.

The funding business, alternatively, way back realized that when you cost individuals in a bizarre manner that nobody understands – then you may cost them much more! MER is proven as a share. That share quantity is all the time a small quantity – BUT what you need to understand is that the proportion you see applies to each single greenback that you’ve invested (whether or not your investments made cash that yr or not).

Canadian mutual funds (a quite common option to spend money on shares and bonds) have the very best mutual fund charges on the earth at about 2% in 2022 based on Morningstar mutual fund knowledgeable Ian Tam. That implies that you probably have a $500,000 portfolio, you’re paying about $10,000 yearly in MER charges.

The earlier that every one Canadians get out of mutual funds the higher. Their excessive MERs are a scourge on investor returns. Don’t let anybody else let you know otherwise. There is no such thing as a proof that mutual fund managers can decide shares any higher than your pet cat – simply steer clear of them.

Again to regularly-scheduled programming…

MERs on fundamental index ETFs are about 0.10% to 0.25%. In different phrases, they’re about 10% the price of a mutual fund. They’re additionally extra tax environment friendly than mutual funds, and have a vastly superior long-term monitor document in relation to funding efficiency than the common mutual fund in Canada.

After all, when you purchase your individual shares, then you definately don’t should pay any MER. In that case you solely pay the transaction value to purchase or promote the inventory.

Whereas paying no MER sounds fairly good (and it’s), it may be tough and time consuming to construct a really diversified portfolio of particular person shares. Consequently, lots of people will use index fund ETFs to simply and shortly make investments their retirement nest egg.

As we’ve beforehand talked about, an index fund is a common time period that covers a couple of completely different particular kinds of investments. After we discuss an investing “index” – that’s simply code for “all the belongings in a given market”. That given market could possibly be all the shares in Canada, or it could possibly be a broad sampling of presidency bonds within the USA. An index may also be a a lot smaller and considerably sophisticated area of interest, corresponding to one which tracks the costs for agricultural corporations and known as “COW” (I’m not making this up).

Do not forget that ETFs are the nanaimo bars of investments. By shopping for one small sq. (“unit” in funding phrases) you get to learn from many tasty layers of shares or bonds.

Most Canadian retirees solely have to concentrate on essentially the most fundamental indexes and index funds. These massive, easy, index funds are very low cost to purchase and listing each single one of many largest corporations on the earth, or all the authorities bonds in Canada.

In case you Google “index funds” you’re more likely to be bombarded by advertisements for a monetary business that’s attempting to promote you high-fee merchandise underneath the guise of being pleasant to low-cost buyers. What occurred right here is that the massive monetary corporations realized that low-cost index buyers, who didn’t need to pay loopy excessive charges to spend money on mutual funds, have been killing their golden goose. So, they began to invent completely different merchandise that stole the frequent names that had been utilized to this newer, cheaper type of index investing.

ETFs are going to unfold your funding {dollars} out so that you simply’re assured to get the common of that particular market (for about 10% of the associated fee that you simply’d pay for mutual funds in Canada).

For instance:

- The VCN ETF takes your funding greenback and makes use of it to purchase small chunks of the 185 largest corporations in Canada. You’ll get the common return and the common dividend from this various group of corporations.

- The VXC ETF buys small chunks of the 11,400 largest corporations outdoors of Canada. (Greater than half of them are within the USA.)

- The VAB ETF splits your funding greenback into a whole lot of the lowest-risk bonds in Canada. You’ll get the common rate of interest that these bonds are charging their debtors, and the common of the very small capital acquire motion that they may expertise as properly.

Ought to Canadian Retirees Use a Robo Advisor?

ETFs are the most affordable option to harness the facility of index investing.

There are two essential ways in which Canadian retirees can select to deal with their index funding portfolio.

1) Go surfing, open a reduction brokerage account, put cash into that account, and purchase the ETFs immediately utilizing the Toronto Inventory Trade (TSX).

2) Open an account with a robo advisor (which can then buy index ETFs in your behalf routinely).

Now, opening a reduction brokerage and going full DIY as you deal with your individual investments may be very doable for most individuals. You’ll in all probability should dedicate a couple of hours to the studying and paperwork as a way to get correctly arrange. After that, it can take you actually a couple of minutes every year to deal with your investing – when you keep on with easy index investing, that’s.

Nevertheless, lots of people get intimidated by this course of. A variety of the terminology might be form of scary, and whereas we’re usually positive with spending a whole lot of {dollars} to buy garments on-line, shopping for a whole lot of {dollars} of ETFs on-line proves to be a a lot simpler course of to endlessly procrastinate.

I, personally, have really useful index investing by way of low cost brokerages to a whole lot of individuals through the years, and I guess near 90% left our chats saying that they have been positively going to do it.

The most typical consequence?

They did nothing. They didn’t open a reduction brokerage account. They didn’t purchase ETFs. They didn’t begin investing.

Possibly I’m simply not a lot of a motivational speaker!

That psychological hurdle of getting began and truly clicking “purchase”, mixed with the small paperwork impediment, has confirmed to be a really giant mountain to climb for many people who find themselves busy of their day-to-day lives.

This result’s nothing wanting a monetary tragedy.

Something that stops individuals from investing or not directly funnels them into the clutches of slick-talking monetary salespeople implies that of us are giving up a ton of monetary freedom of their lives. They’re giving up household journeys or early retirement. They’re giving up the unbelievable feeling of monetary independence. They usually’re giving it up as a result of the monetary business has labored actually exhausting to inform them that they’ll’t make investments on their very own, and to confuse the mathematical information of how long-term investing really works.

Into this gaping chasm of data and motion stepped the robo advisors. About ten years in the past a service started to exist that mainly stated:

“Ship us a small amount of cash every month [or each year…or whenever] and we’ll immediately make investments it right into a pre-arranged batch of index ETFs for you. Oh – and we’ll even be round to reply any questions you may need about use the platform, or how taxes work on this investing stuff.

Principally, e-mail us or use our on-line chat, and we’ll reply your questions. In return for this comfort, we’re going to cost you someplace within the neighbourhood of about $60 yearly for each $10,000 that you simply make investments with us (an MER of .60%).“

Initially, I used to be skeptical of any monetary service, however these platforms have been sticking to index investing, and utilizing a lot of the identical ETFs that I used to be – in order that they couldn’t be all dangerous. I began to advocate them to a couple of my buddies who hadn’t been capable of climb the DIY low cost brokerage mountain.

Then a magical factor occurred: almost all the individuals who I really useful the robo advisor choice to truly did it!

My buddies opened an instantaneous index investing portfolio and connected their financial institution accounts inside minutes. They liked how easy it was. They liked that they might ignore the maths concerned with rebalancing their asset allocation. I liked that that they had somebody on the robo advisor to reply all of their questions – as a result of then we may discuss extra enjoyable issues at dinner events!

All of that being stated, I nonetheless really feel barely hypocritical at instances recommending a product that I don’t personally use. I really feel that for my particular person preferences, opening a reduction brokerage and reducing my funding prices to the bone is well worth the tradeoff in time and comfort. That stated, I’m additionally a geek who likes to learn monetary books for enjoyable – so I’m not an excellent check group. You’ll should determine if the associated fee is value it for you.

Our article on the most effective all-in-one ETFs in Canada totally explains the trade-offs of prices and comfort in relation to the assorted other ways to spend money on shares in Canada. I actually suppose it’s value every retiree’s time to contemplate a robo advisor in the event that they don’t need to deal with their very own investments. The charges are considerably decrease than those from mutual funds and it’s actually simply so extremely simple to make use of one.

Greatest ETFs for Retirement Earnings in Canada

Whereas I believe that there’s a actually stable argument for a plain vanilla all-in-one ETF being a superb choice, I do know that many retirees are searching for income-based ETFs so as to get pleasure from retirement money move.

Right here’s a fast comparability of three attention-grabbing choices when you’re seeking to prioritize reliable revenue in Canada:

| Function Longevity Pension Fund | Non-Assured Annuity at 65 | Vanguard VRIF | |

| Focused Funding Return | 3.5% | Varies broadly. Not likely related to the shopper, as they’re assured a sure payout in trade for his or her principal. | 4.3% |

| Annual Cash Yielded Into Your Financial institution Account as a % of Authentic Contribution | Hopefully 6.15% | 5-7% Relying on what situations you connect to your particular annuity. | Varies primarily based on market situations. Will seemingly be fairly near 4% over the loooong time period. |

| What occurs if I go away comparatively younger? | You get what’s left of your authentic capital funding, however not one of the funding returns that your cash has generated. | Will depend on specifics – however most annuity applications both say, “Thanks in your contributions” or they permit for some quantity payable to a surviving partner. | It’s 100% your funding – so no matter your final will and testomony says, that’s what can be completed with it. |

| Is the return assured? | No | Sure | No |

| Administration Charges | .6%-1.1% (mutual fund price construction) | 1-3% – paid upfront and in annual charges which are pre-calculated into your promised payout. | .29% |

| Sorts of Investments | 47% shares, 38% fastened revenue, and 15% different investments that embrace gold and commodities, picked investments by mutual fund supervisor (utilizing principally ETFs) | The amount of cash to you just isn’t actually depending on investments… however most annuity corporations normally make investments by way of stock-based mutual funds. | 30% shares, 70% bonds, utilizing Vanguard’s index ETFs |

These are three very completely different merchandise, however they’re all created with retirement revenue in thoughts.

I’m not going to go too far into Canadian annuities as a result of we’ve acquired a superb article on the location already that goes fairly in-depth. Suffice it to say, I believe loads of Canadian retirees could be properly served to switch the “fastened revenue” portion of their portfolio with an annuity.

Vanguard’s VRIF might be the most effective ETF for retirement revenue in Canada, because it makes use of a conservative asset allocation, additional juiced by choices so as to squeeze out essentially the most revenue attainable. It additionally has fairly a low MER.

Lastly, the Function Longevity Fund is an attention-grabbing mixture of annuity-style threat pooling and funding returns. It’s a bit sophisticated, however primarily the product is ready to maintain very conservative investments – whereas paying out over 6%, as a result of it solely continues to pay you when you’re alive. In case you go, your property will get most of your authentic fee again, however your funding returns will keep within the fund – thus benefiting those who dwell the longest. Listed here are the small print on the aim longevity pension fund.

Sunlife Retirement Earnings

In late 2024 Solar Life (a big Canadian insurance coverage firm) got here up with yet one more product geared toward offering revenue for Canadian retirees. The product is solely known as MyRetirement Earnings.

One factor to remember when taking a look at all of those merchandise is that the underlying investments by no means actually change. It’s nearly all the time some mixture of shares and bonds (similar to what you’d discover in an all-one-ETF).

Often there’s a tweak corresponding to just a little little bit of choices income, or just a little little bit of publicity to gold. The higher ones have an annuity-esque facet the place you’re form of pooling threat (with the monetary threat we’re speaking about not truly dying sooner – however dwelling longer).

MyRetirement Earnings is a bit completely different in that it’s geared toward of us who’ve outlined contribution pension plans. For a fast primer take a look at Kyle’s article on pensions in Canada. Outlined contribution (DC) plans are utilized by many non-public employers (versus the federal government – which makes use of principally outlined profit plans). Solar Life facilitates a giant share of Canadian DC plans, so it is sensible that they may need to develop a product for this market.

MyRetirement Earnings permits shoppers to simplify their retirement funds. Principally, the day you go from saving to retirement, to spending in retirement, you may let Solar Life know the date you need to obtain cheques till (say your ninetieth or ninety fifth birthday) and Solar Life will ship you a cheque every month for a corresponding quantity.

In an effort to assure these funds, Solar Life goes to place your cash into a really conservative pot of investments. As a result of it takes age into consideration (like an annuity or the Function Longevity Fund) Solar Life can afford to pay out a reasonably excessive share of the cash within the fund (as some of us will go away before others and never accumulate all of their month-to-month cheques).

For instance, when you retire at age 65 and begin amassing funds – choosing the 95-year-old choice – you’ll get an revenue charge of 5.9% of the cash you place into MyRetirement. It’s not correct to say that it’s an funding return, as a result of loads of that’s your individual cash being withdrawn and handed to you.

However right here’s the actual crux of the matter… The mutual funds used inside the SunLife MyRetirement product have an MER of about 2%. That’s insanely excessive!

For that cause alone, it’s actually not value wanting into the product in any respect. You’d be a lot better off simply taking a look at some mixture of annuities and inventory market investments corresponding to VRIF.

Greatest Investments for Canadian Retirees – FAQ

Select Your Private Greatest Investments for Retirement

No person can let you know prematurely what the most effective investments for the subsequent 20 years can be. There are in all probability many individuals who declare they’ll let you know this data due to their magical crystal ball – however they’re mendacity.

In case you ask any of the most effective monetary advisors in Canada, they’ll all inform you an identical factor: Selecting the most effective investments for retirement is all about defining your private targets and threat tolerance. After that, deciding on the suitable asset allocation to shares and bonds is fairly easy.

Along with determining what your threat tolerance is and choosing the proper asset allocation technique in your nest egg, you will want to determine what platform you need to use to spend money on these belongings. Some of us simply aren’t snug with DIY-ing their retirement funding portfolio utilizing a reduction brokerage account.

In case you’re searching for the final word mixture of security and comfort in your retirement investments, I like to recommend trying out Kyle’s retirement course by clicking right here. In that course, he breaks down why the most effective answer for most individuals might be a mixture of an annuity, and a easy broad-based all-in-one ETF. He additionally solutions any questions that you’ve in his on-line classroom.

Are You Saving Sufficient for Retirement?

Canadians Consider They Want a $1.7 Million Nest Egg to Retire

Is Your Retirement On Observe?

Change into your individual monetary planner with the primary ever on-line retirement course created solely for Canadians.

Strive Now With 100% Cash Again Assure

*Information Supply: BMO Retirement Survey

{kind=link}