: A Complete Information")

{kind=link}

Kisan Vikas Patra (KVP) is a small financial savings instrument launched by the Indian Authorities to encourage long-term financial savings. Initially aimed toward farmers to advertise small financial savings in rural areas, KVP has grown well-liked amongst individuals on the lookout for a protected funding avenue with predictable returns.

What’s Kisan Vikas Patra?

Kisan Vikas Patra is a fixed-rate financial savings scheme accessible at India Submit Places of work and choose public sector banks. The scheme provides assured returns on funding and supplies capital appreciation by doubling the funding over a hard and fast tenure. KVP is well-liked as a consequence of its authorities backing, offering a low-risk funding possibility that appeals to conservative traders.

Key Options of Kisan Vikas Patra

| Characteristic | Particulars |

| Minimal Funding | ₹1,000 (in multiples of ₹100) |

| Tenure | Round 115 months (9 years and seven months) |

| Curiosity Charge | 7.5% each year (varies per quarter) |

| Tax implications | No tax profit on preliminary funding; curiosity is taxable |

| Untimely Withdrawal | After 2.5 years, with lowered returns |

| Assure | Backed by the Authorities of India |

| Nomination Facility | Accessible |

Word: The rate of interest on KVP is topic to periodic modifications by the federal government, sometimes introduced each quarter.

How Does Kisan Vikas Patra Work?

Once you spend money on KVP, your cash is assured to double in 115 months on the present rate of interest of roughly 7.5%. The scheme makes use of a compound curiosity system, that means your funding grows steadily over the time period. KVP certificates can be found in denominations from ₹1,000 upwards, and there’s no higher funding restrict.

Eligibility Standards for KVP

· People: Indian residents above 18 years of age can make investments.

· Minors: Investments on behalf of minors are allowed.

· NRIs: Non-Resident Indians will not be eligible for KVP.

Advantages of Kisan Vikas Patra

1. Authorities Safety: Since KVP is a government-backed scheme, it supplies excessive safety for traders.

2. Assured Returns: Traders obtain a assured return, with the reassurance that the funding will double within the prescribed interval.

3. Ease of Entry: KVP certificates can be found in any respect publish places of work and choose banks, making it straightforward to buy.

4. Transferable Certificates: KVP certificates will be transferred from one particular person to a different or from one publish workplace/financial institution to a different, providing flexibility.

5. No Funding Cap: There is no such thing as a most restrict on funding, making KVP appropriate for these with excessive investable surplus looking for low-risk returns.

Evaluating Kisan Vikas Patra with Different Small Financial savings Schemes

| Scheme | Curiosity Charge (approx.) | Lock-in Interval | Tax Profit (Sec 80C) | Untimely Withdrawal |

| Kisan Vikas Patra | 7.5% p.a. | 9 years, 7 months | None | After 2.5 years |

| Public Provident Fund (PPF) | 7.1% p.a. | 15 years | Sure | Partial after 5 years |

| Nationwide Financial savings Certificates (NSC) | 7.7% p.a. | 5 years | Sure | Not allowed |

| Senior Residents’ Financial savings Scheme (SCSS) | 8.2% p.a. | 5 years | Sure | Penalty after 1 yr |

| Fastened Deposit (Financial institution) | Varies (5-7% approx.) | Versatile | Sure | Penalty on early withdrawal |

KVP Tax Implications

1. No Tax Deduction beneath Part 80C: In contrast to PPF or NSC, investments in KVP don’t qualify for tax deductions beneath Part 80C.

2. Tax on Curiosity Revenue: The curiosity earned is added to the investor’s taxable revenue annually and is topic to tax as per relevant revenue tax slabs.

3. No TDS on KVP Curiosity: No Tax Deducted at Supply (TDS) is utilized on the quantity withdrawn publish maturity. Nevertheless, this doesn’t exempt you from declaring the curiosity revenue in your revenue tax returns (ITR) and paying tax accordingly.

Who Ought to Put money into Kisan Vikas Patra?

KVP is right for conservative traders who prioritize security and assured returns over excessive progress. It’s significantly suited to:

1. People with Low-Danger Urge for food: KVP supplies assured returns with out publicity to market volatility.

2. Traders Searching for Lengthy-Time period, Protected Investments: The scheme is helpful for individuals who need to develop their cash steadily with out taking dangers.

3. Senior Residents and Rural Traders: These teams sometimes want safe investments with authorities backing.

The way to Put money into Kisan Vikas Patra?

1. Go to a Submit Workplace or Licensed Financial institution: Go to a close-by publish workplace or approved financial institution department that provides KVP.

2. Full KYC Course of: Submit proof of identification, handle, and different KYC paperwork.

3. Fill Out the Utility Type: Fill within the required particulars, together with nominee particulars.

4. Fee: Make the fee in money, cheque, or demand draft.

5. Obtain KVP Certificates: Upon verification, the KVP certificates is issued within the investor’s identify.

Historic Curiosity Charges for Kisan Vikas Patra

| YEAR | RATE OF INTEREST (%) |

| 23-09-2014 to 31-03-2016 | 8.7(100 Months) |

| 1.4.2016 to 30.9.2016 | 7.8 (110 Months) |

| 1.10.2016 to 31.3.2017 | 7.7 (112 Months) |

| 1.4.2017 to 30.6.2017 | 7.6 (113 Months) |

| 1.7.2017 to 31.12.2017 | 7.5 (115 Months) |

| 1.1.2018 to 30.9.2018 | 7.3 (118 Months) |

| 1.10.2018 to 30.6.2019 | 7.7 (112 Months) |

| 1.07.2019 to 31.03.2020 | 7.6 (113 Months) |

| 1.4.2020 to 30.09.2022 | 6.9(124 Months) |

| 1.10.2022 to 31.12.2022 | 7.0(123 Months) |

| 1.01.2023 to 31.03.2023 | 7.2(120 Months) |

| 1.04.2023 to 31.12.2024 | 7.5(115 Months) |

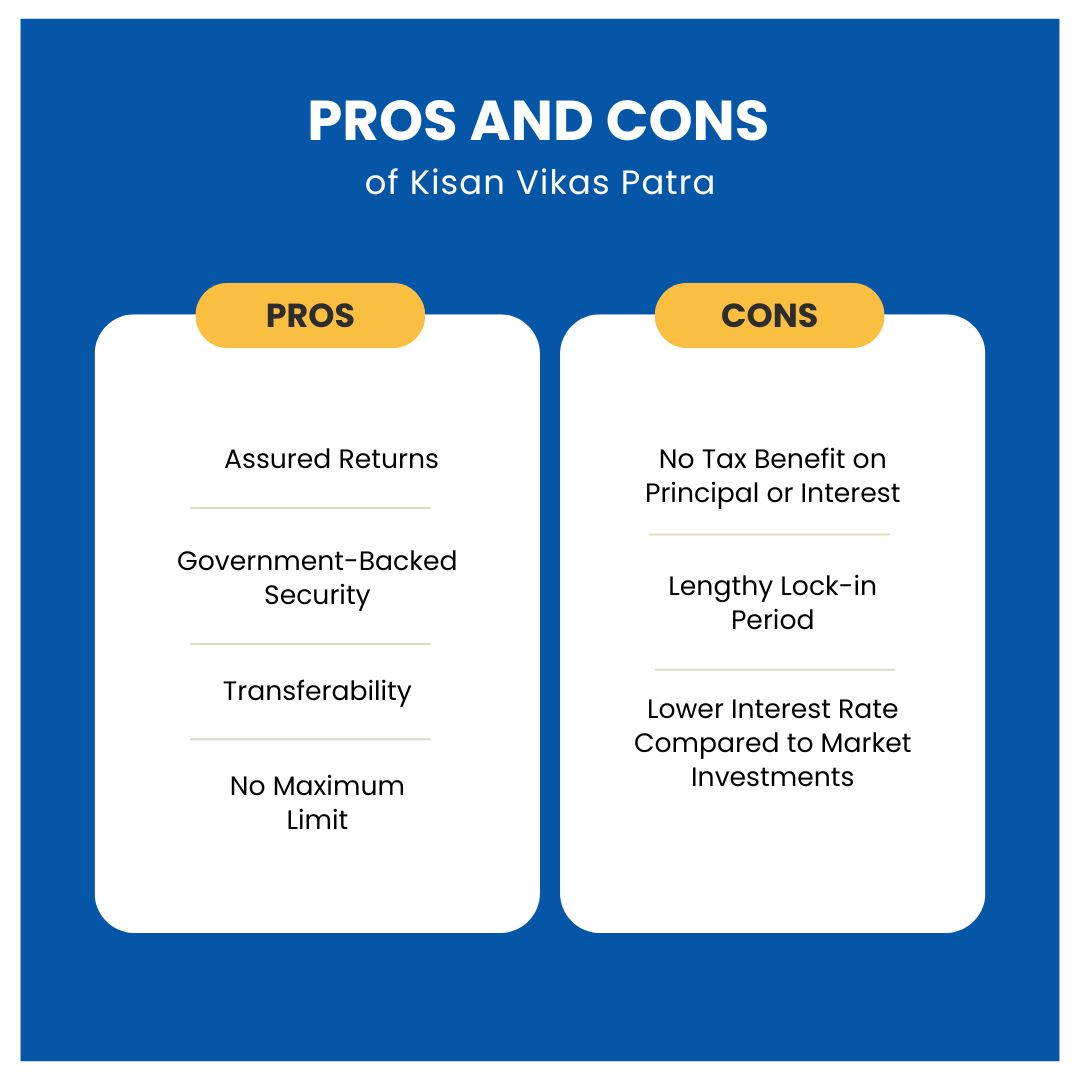

Professionals and Cons of Kisan Vikas Patra

Professionals

· Assured Returns: Assured return on funding.

· Authorities-Backed Safety: Low threat as a consequence of authorities assist.

· Transferability: Can switch possession, making it versatile.

· No Most Restrict: No higher restrict on the quantity invested.

Cons

· No Tax Profit on Principal or Curiosity: Curiosity earned is taxable.

· Prolonged Lock-in Interval: Maturity interval of 10 years and 4 months can restrict liquidity.

· Decrease Curiosity Charge In comparison with Market Investments: The speed of return is decrease than some market-linked merchandise like mutual funds.

Conclusion

Kisan Vikas Patra is a strong funding alternative for risk-averse people who worth safety and guaranteed returns. Whereas the returns is probably not as excessive as market-linked investments, the assure of doubling the funding makes it a dependable possibility, significantly in occasions of financial uncertainty. Nevertheless, potential traders ought to weigh the dearth of tax advantages and think about their liquidity wants earlier than committing to KVP.