{kind=link}

Firm overview

Integrated in 2001 and headquartered in Gurugram, Vishal Mega Mart is a hypermarket chain that sells a variety of merchandise like attire, groceries, electronics, and residential necessities by means of its portfolio of personal manufacturers and third-party manufacturers. The corporate sells its merchandise although a pan-India community of 645 Vishal Mega Mart shops (30 September 2024) and Vishal Mega Mart cellular software and web site throughout three main product classes – attire, normal merchandise and FMCG. As of 30 September 2024, it has presence in 414 cities in 28 states and two union territories. The corporate was ranked as one of many prime two offline-first diversified retailers in India.

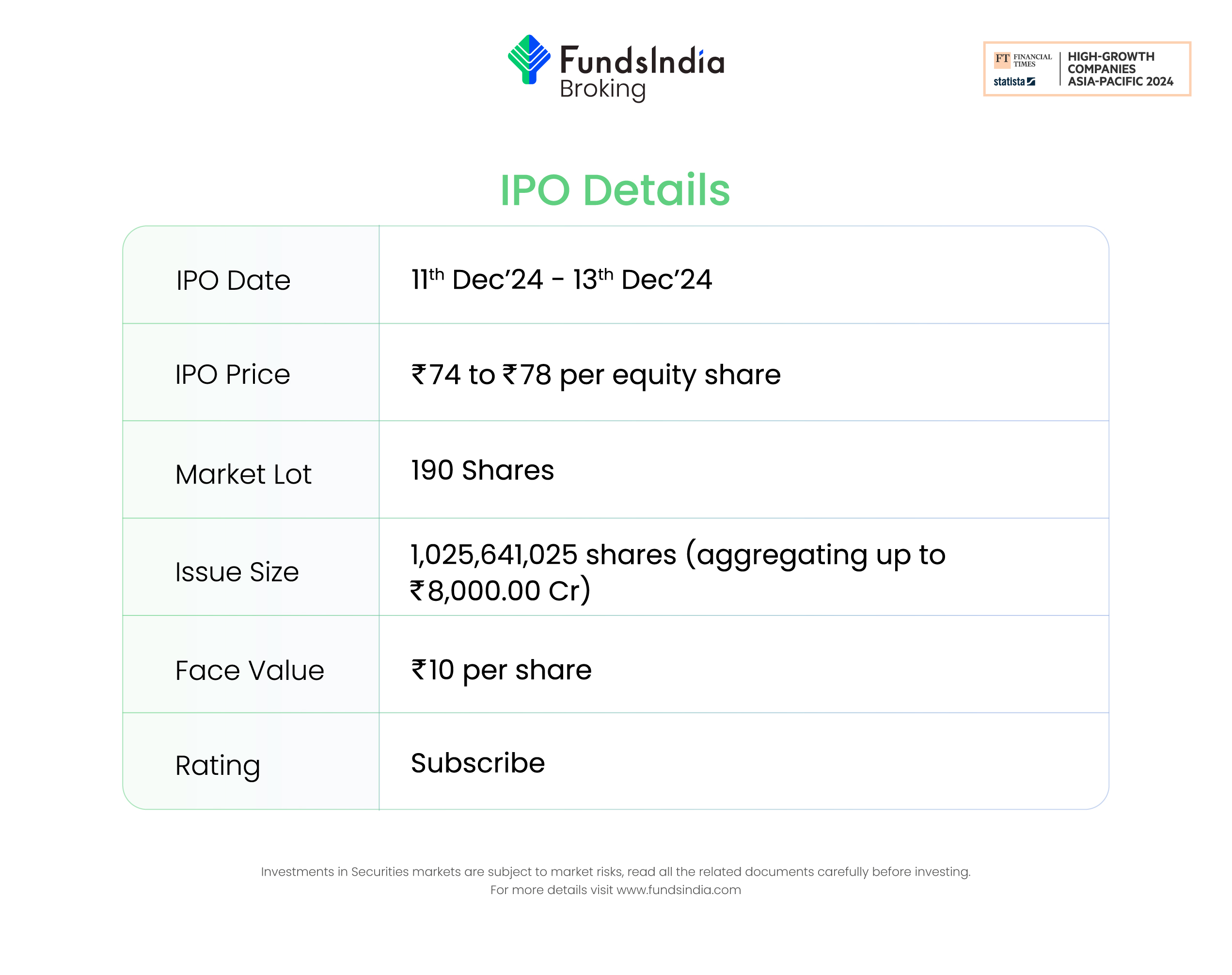

Objects of the provide

- To attain the advantages of itemizing the Fairness Shares on Inventory Exchanges.

- Perform the provide on the market of fairness shares aggregating Rs.80,000 million by the Promoter Promoting Shareholder.

Funding Rationale

- Deal with center and decrease revenue inhabitants – The corporate primarily caters to the massive and rising center and lower-income segments of the Indian inhabitants. It operates an intensive community of shops in Tier 2 cities and past. With growing entry to digital channels, shoppers in these areas have gotten extra uncovered to new services, which drives demand and opens new retail alternatives as they search to undertake higher-tier city existence. The corporate gives a broad vary of merchandise beneath each its personal and third-party manufacturers. It stands out amongst offline-first diversified retailers by offering a well-rounded mixture of merchandise that meets the wants of center and lower-income shoppers. Its product vary spans numerous value factors, together with attire and a wide range of objects corresponding to clothes, denims, t-shirts, shirts, bedsheets, spin mops, casseroles, pet bottles, butter cookies, savory snacks (like navratan namkeen), sanitary napkins, oats, fruit juice, noodles, and extra.

- Diversified portfolio and geographical footprint – The corporate gives a broad portfolio of its personal manufacturers throughout numerous classes, together with attire for males, ladies, kids, and infants, in addition to family items, house furnishings, journey equipment, kitchen home equipment, utensils, crockery, footwear, and life-style merchandise throughout the normal merchandise class. Within the fast-moving client items (FMCG) sector, the corporate gives meals merchandise, non-food objects, and staples. In FY24, 19 of its personal manufacturers achieved gross sales exceeding Rs.1,000 million every, with six manufacturers surpassing Rs.5,000 million every in gross sales. The corporate’s income from the sale of its personal manufacturers grew at a compound annual progress charge (CAGR) of 27.72% between FY22-24. Over the previous three years, the corporate has considerably enhanced its product choices within the non-apparel section, introducing objects corresponding to air fryers, garment steamers, egg boilers, beard trimmers, juicers, sound bars, journey audio system, induction cooktops, vegetable choppers, peanut butter, cashew almond cookies, fruit and nut cookies, chips, hair oil, and biscuits, amongst others. As of March 31, 2024, the corporate ranks second among the many main offline-first diversified retailers in India, based mostly on the variety of cities it operates in.

- Monetary observe file – The corporate reported a income of Rs.8,954 crore in FY24 towards Rs.7,619 crore in FY23, a progress of 18%. The income has grown at a CAGR of 26% between FY22-24. The EBITDA of the corporate in FY24 is at Rs.1,429 crore, a 40% YoY progress in comparison with Rs.1,021 crore of FY23. The web revenue of the corporate in FY24 is Rs.462 crore. The web revenue elevated by 44% in comparison with Rs.321 crore in FY23. The CAGR between FY22-24 of EBITDA is 33% and PAT is 51%.

Key dangers

- OFS Danger – The IPO consists of solely an Provide for Sale of Fairness Shares value as much as Rs.80,000 million by the Promoting Shareholders, together with the corporate Promoter. The whole proceeds from the Provide for Sale might be paid to the Promoting Shareholders, together with Promoter and the Firm is not going to obtain any such proceeds. The provide includes the sale of stake value Rs.80,000 million by promoter Samayat Providers LLP.

- Dependence on third social gathering distributors – The corporate doesn’t have any in-house manufacturing amenities and is dependent upon third social gathering distributors for the manufacture of all of the merchandise beneath its personal model. Any lack of ability by the third social gathering distributors in assembly the product specs, high quality, and manufacturing requirements would possibly impression the operations, money circulate and monetary situations of the enterprise.

- Danger of strategic inertia – If the corporate fails to establish and successfully reply to altering client preferences in a well timed method, the demand for its merchandise would possibly lower, impacting the market share and outcomes of operations.

Outlook

The corporate has achieved constant progress in its monetary efficiency over the reported intervals and we anticipate the corporate to proceed its progress momentum. The aspirational retail market in India, fueled by client demand for merchandise that mix top quality and affordability, will proceed to be a key driver of the nation’s retail sector the place the corporate has suitably positioned itself to seize an growing market share. In accordance with RHP, Avenue Supermarts Restricted and Trent Restricted are the one listed opponents for Vishal Mega Mart Restricted. The friends are buying and selling at a mean P/E of 130.91x with the very best P/E of 163.59x and the bottom being 98.23x. On the larger value band, the itemizing market cap of Vishal Mega Mart might be round ~Rs.35,168 crore and the corporate is demanding a P/E a number of of 76.13x based mostly on submit problem diluted FY24 EPS of Rs.1.02. Compared with its friends, the difficulty appears to be absolutely priced in (pretty valued). Primarily based on the above views, we offer a ‘Subscribe’ score for this IPO for a medium to long-term Holding.

Notice: Please observe that this isn’t a suggestion and is meant just for instructional functions. So, kindly seek the advice of your monetary advisor earlier than investing.

Different articles you might like