{kind=link}

For these of us who’ve a house mortgage, paying it off is probably not an choice. Both you lack ample money, or retiring the mortgage early would go away you money poor and susceptible.

Even for these of us who do have the means, the choice whether or not to repay the mortgage is unclear. We are able to come to an approximate reply by evaluating the price of maintaining the mortgage to the price of paying it off, and select the lesser of the 2.

However whereas the price of the mortgage is knowable, the price of paying it off shouldn’t be. That’s as a result of we can not know the return we’ll obtain by investing the cash elsewhere.

Even when the mathematics favors paying off the mortgage, there are loads of different nuances to think about.

My Dilemma

I purchased my home in 2011, financing it with a 30-year, fixed-rate mortgage at 3.75% curiosity. Two years later, lured by a good decrease charge surroundings, I refinanced to a 7-year, adjustable-rate mortgage at simply 2.625% curiosity. This knocked $212 off my month-to-month mortgage funds, netting me a financial savings of 18%.

My rationale appeared sound. Along with saving greater than $2,500 a 12 months, refinancing locked me in to assured low cost cash for not less than 7 years (an eternity, proper?).

Furthermore, the wonderful print on the notice stipulated that after the 7-year fixed-rate interval expired, my charge may modify up (or down) by not more than 2% per 12 months, and by no means exceed a most of seven.625%.

This quantity is sort of affordable by historic requirements; fairly tolerable, too, I reasoned, ought to it come to move. After a decade of rock-bottom rates of interest—or extra precisely the macroeconomic surroundings holding them down—many predicted charges would by no means go that top once more.

The graph beneath helps illustrate how one is likely to be forgiven for making this assumption.

Associated: What Are the Monetary Benefits of House Possession?

Associated: Renting vs. Shopping for: The True Value of House Possession

Adjustment Time

In June 2020 the fixed-rate interval on my mortgage expired. My charge went up, however by lower than 1% (to three.5% from 2.625%). This was the primary in a sequence of annual charge changes, which have been to be calculated by including 2% to the 1-year LIBOR (since changed by SOFR) within the quarter previous the adjustment.

One 12 months later, in 2021, my charge truly went down. For the subsequent 12 months I might pay simply 2.5% curiosity on my mortgage (was that 2013 refi a stroke of genius or what?).

With 12 years of ultra-low charges within the rearview, there was no motive to imagine my charge would ever modify up once more.

No Earnings, No Mortgage

All the identical, I like certainty. So I made a decision to refi once more, this time to a 15-year, fixed-rate mortgage at ~2.5%. Such was the speed being supplied in the summertime of 2021.

Bother is, I used to be a retiree, and 98% of the mortgage lenders on the market couldn’t wrap their heads round lending to a zero-income borrower, even when that borrower had greater than sufficient belongings to make good on the mortgage. I submitted one software after one other. Every was summarily dismissed.

What of the two% of lenders that would work with me, those who would make me a so-called asset-only mortgage? Properly, they needed to cost me a ~1% premium for the privilege.

I punted, reasoning that so long as charges didn’t go up, I may proceed to journey the low-interest gravy practice, possibly even in the course of my current mortgage. Once more, this was an comprehensible—if not altogether rational—expectation after a decade-plus of ultra-low charges.

Associated: Getting a Mortgage When You Have Belongings However No Earnings

The “I” Phrase

Then got here 2022, and everyone knows what occurred subsequent. Inflation reared its head in an enormous approach, and compelled the Federal Reserve to boost short-term rates of interest, quick and by loads.

This resulted in two consecutive years of two% will increase on my mortgage (keep in mind, this was the utmost annual enhance assured by my lender), pushing my charge as much as its present stage of 6.5%. Now I’m dealing with one other charge adjustment, to the 7.625% most, in June 2024.

Right here’s a desk that paints the image extra concretely. It illustrates the impact of reasonable charge will increase on the precise value of my mortgage.

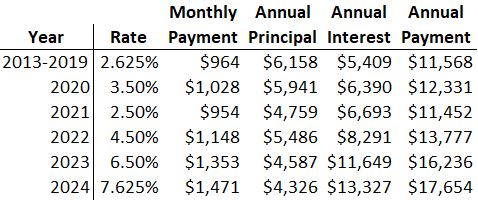

For the primary 7 years of my mortgage—the mounted time period, lasting from 2013 to 2019—I paid $964 a month on my mortgage. I’m at the moment paying $1,353 a month and, as of June 2024, I might be paying $1,471. That’s a rise of 53%, which equates to $507 a month ($6,086 a 12 months) greater than what I paid through the mounted interval of my mortgage.

What’s extra, the upper my charge, the larger the proportion of my month-to-month cost that goes to curiosity, not principal. A lot for pondering 7.625% could be a tolerable charge.

A Wider View

It’s instructive to notice that that is very a lot the scenario dealing with loads of companies within the U.S., and is exactly the ache the Central Financial institution goals to inflict when it will increase the federal funds charge.

The upshot for companies is that they spend much less cash. In spite of everything, whenever you’re spending extra on debt service, you’re spending much less on different issues. This cools combination demand, thereby bringing the general worth stage down (or so goes a half-century of macroeconomic idea).

For companies, this implies much less funding in plant and tools, and possibly even layoffs. For individuals like me, it means fewer dinners out, and pondering twice about that journey overseas. By hurting companies and people alike on this approach, the Fed hopes to wrestle inflation again right down to an affordable stage.

Right here’s a graph of the Fed’s coverage charge relationship again to 1970. Should you examine it to the one above, graphing the typical 30-year mortgage charge over the identical interval, the correlation is unmistakable.

I attempt to remind myself that low inflation in the long run is probably going value some ache within the brief (however I’m a silver-lining sort of a man).

Retire the Mortgage?

Why don’t I simply repay the mortgage? Nice query! And one to which I’ve given loads of thought these days.

Paying off my mortgage could be akin to creating a considerable funding in a selected asset class—specifically actual property. It could additionally symbolize a major reallocation of my retirement portfolio. At a 7.625% return on funding, I admit it’s a tempting prospect.

Consolidation of Danger

However paying off my mortgage has downsides, and never an inconsiderable quantity of danger. For one factor, that actual property funding represents a single level of loss.

What if my home burns down? Sure, I’d get cash from the insurance coverage firm, hopefully sufficient to rebuild a liveable construction the place that smoking gap was. However how can I ensure?

Possibly I’d simply stroll away with that insurance coverage cash and grow to be a renter. This could quantity to an enormous loss on my actual property funding. On this sense, paying off the mortgage appears to me like a harmful consolidation of danger.

Liquidity Danger

Then there may be liquidity danger. Paying off the mortgage would tie up a ship load of in any other case liquid capital I’d want for unexpected circumstances; say a brand new automobile if my current one offers up the ghost.

I’d be compelled to promote different belongings to generate money, probably at a loss.

Associated: 3 Unhealthy Monetary Selections That Helped Me Retire Sooner

Tax Implications

Brief Time period

What about taxes? In an effort to increase money to repay the mortgage, I’d must promote belongings–i.e., inventory and bond ETFs and/or mutual funds–in both my brokerage account or my IRA. Both approach, this might end in a considerable, one-time tax legal responsibility.

And if the sale ends in a capital loss? Then I’d should suppose exhausting about promoting at a loss belongings supposed to fund my retirement.

Additionally, as a recipient of ACA subsidies and cost-sharing reductions, I might lose the bulk (if not all) of these advantages within the tax 12 months I bought the belongings. I lean closely into ACA; in actual fact, with out it, I might not have felt snug retiring as I did at age 53.

Lengthy Time period

The image brightens a bit after I take into account the long-term tax implications of paying off the mortgage.

My retirement earnings technique quantities to withdrawing a set quantity from my brokerage account month-to-month, and sustaining a money cushion in that account of a couple of 12 months’s value of bills. In an effort to keep that cushion, I promote inventory and/or bond ETFs periodically on the long-term capital beneficial properties charge.

With the month-to-month mortgage cost gone, I’d should promote fewer belongings to keep up my money cushion. This could have the impact of reducing my tax legal responsibility within the years after that first-year tax hit.

Curiosity Fee Danger

What about rates of interest? What if they arrive again down, say by loads? Then the return on my funding is not anyplace close to the 7.625% I booked after I paid off the mortgage, and by then it’s too late to do something about it.

Psychological Implications

The attract of being fully debt-free is highly effective. Some is likely to be studying this and suppose, boy, if solely I had the money to repay my mortgage, I’d do it in a heartbeat!

You’ll be able to’t put a price ticket on high quality sleep. If paying off the mortgage permits you to sleep higher at evening, the monetary prices could also be value it.

Upshot

The choice to repay a mortgage shouldn’t be as clear-cut as it could appear. Even should you can afford it, there are myriad components to think about. Many of those will rely upon the particulars of your monetary scenario. Every should be factored into the equation, and the return assumptions on paying off your mortgage adjusted accordingly.

In my view, I’ve determined to not repay my mortgage…not less than not but. I’m betting that rates of interest will come down ahead of later, thereby decreasing my month-to-month mortgage funds. If/when that occurs, I’ll revisit a refi. Conversely, if by 2026 or 2027 I’m nonetheless paying 7.625%, then I’ll revisit a payoff.

Errors

Some would possibly argue I made a mistake taking an adjustable-rate mortgage within the first place. I’d agree. However that’s water beneath the bridge. There’s nothing I can do about it now, and I’m not going to waste mind cells dwelling on it.

Extra pertinent (and irksome) to me was giving up so simply on my efforts to refinance in 2021. In hindsight, that 1% premium asset-only lenders have been going to cost me seems to be like a cut price.

I’d be paying ~3.5% on a 15-year fixed-rate mortgage now, as an alternative of the 6.5% (quickly to be 7.625%) I’m paying on my current mortgage. Blindly assuming charges would keep low perpetually was a mistake, and that dangerous assumption is costing me now.

A part of my determination to punt on the 2021 refi was simply plain laziness. I discussed I like certainty. However I traded the knowledge of a fixed-rate mortgage for the comfort of not having to cope with a number of asset-only lenders; notably all of the ceremony that accompanies a mortgage refinance–gathering financial institution and brokerage statements, signing paperwork, getting value determinations, coping with third events, and so forth.

Going Ahead

Charges might certainly come down once more, thereby nudging my mortgage again right down to an affordable stage. Even within the best-case situation, that isn’t more likely to occur any time quickly.

The Fed has indicated it intends to chop its coverage charge in 2024, maybe as many as thrice. Nevertheless it takes a very long time for the federal funds charge to ripple by way of to the longer-term charges that have an effect on mortgages.

Silver-lining man that I’m, within the meantime I’ll do my half to tame inflation by spending much less cash on different stuff.

What Do You Assume?

Do you might have a mortgage? In that case, have you considered paying it off? What components did you take into account that I didn’t?

Be happy to share your insights within the feedback beneath, in order that I and others would possibly be taught one thing out of your perspective or expertise.

Programming Be aware

I might be rafting the Colorado River the day this submit will get revealed, which implies I received’t have the ability to learn or reply to your feedback till after I get again later this month.

Please don’t let this discourage you from leaving a remark, nevertheless, and/or discussing this matter amongst yourselves.

* * *

Precious Assets

- The Greatest Retirement Calculators will help you carry out detailed retirement simulations together with modeling withdrawal methods, federal and state earnings taxes, healthcare bills, and extra. Can I Retire But? companions with two of the perfect.

- Free Journey or Money Again with bank card rewards and join bonuses.

- Monitor Your Funding Portfolio

- Join a free Empower account to realize entry to trace your asset allocation, funding efficiency, particular person account balances, internet value, money movement, and funding bills.

- Our Books

* * *

[I’m David Champion. I retired from a career in software development in March 2019, just shy of my 53rd birthday. To position myself for 40+ years of worry-free retirement, I consumed all manner of early-retirement resources. Notable among these was CanIRetireYet, whose newsletters I have received in my inbox every Monday morning for the last ten years. CanIRetireYet is one of exactly two personal finance newsletters I subscribe to. Why? Because of the practical, no-nonsense advice I find here. I attribute my financial success in no small part to what I have learned from Darrow and Chris. In sharing some of my own observations on the early-retirement journey, I aim to maintain the high standard of value readers of CanIRetireYet have come to expect.]

* * *

Disclosure: Can I Retire But? has partnered with CardRatings for our protection of bank card merchandise. Can I Retire But? and CardRatings might obtain a fee from card issuers. Some or all the card presents that seem on the web site are from advertisers. Compensation might affect on how and the place card merchandise seem on the positioning. The location doesn’t embrace all card corporations or all obtainable card presents. Different hyperlinks on this web site, just like the Amazon, NewRetirement, Pralana, and Private Capital hyperlinks are additionally affiliate hyperlinks. As an affiliate we earn from qualifying purchases. Should you click on on considered one of these hyperlinks and purchase from the affiliated firm, then we obtain some compensation. The earnings helps to maintain this weblog going. Affiliate hyperlinks don’t enhance your value, and we solely use them for services or products that we’re aware of and that we really feel might ship worth to you. In contrast, we have now restricted management over many of the show adverts on this web site. Although we do try to dam objectionable content material. Purchaser beware.