Balances Masks the Reality About Lengthy-Time period Efficiency – Middle for Retirement Analysis")

{kind=link}

Significant balances require steady protection and for that we want a nationwide mandate.

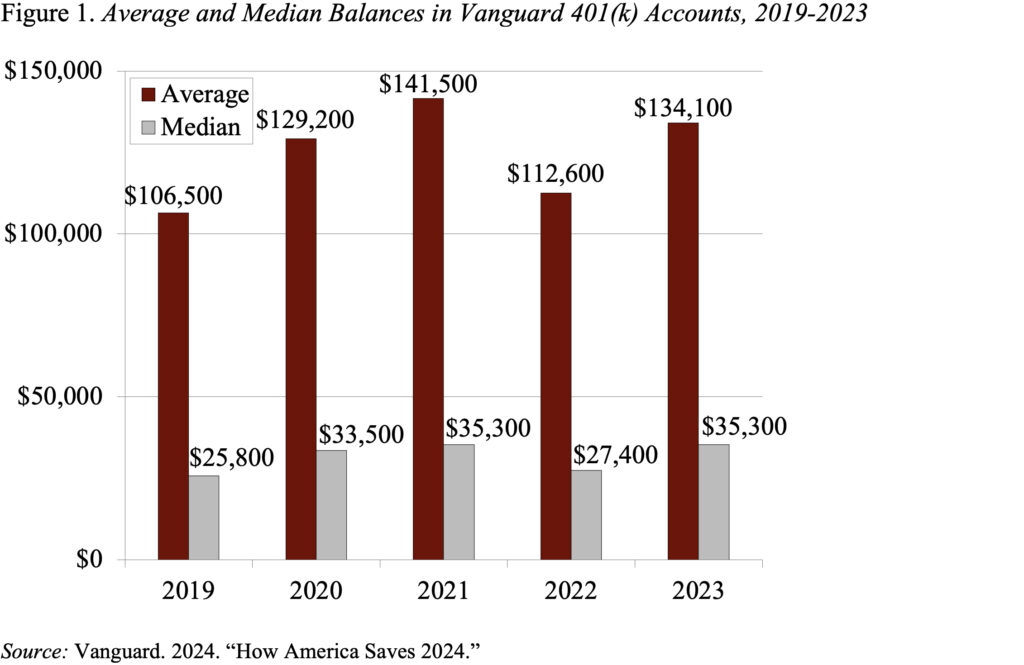

It’s all the time fascinating to take a look at Vanguard’s most up-to-date version of “How America Saves.” And it’s notably fascinating to get the numbers for 2023 – a great 12 months for each the financial system and the inventory market. Certainly, participation price, contribution charges, and median and common balances are near an all-time excessive.

Common balances rose from $112,600 in 2022 – a horrible 12 months for the inventory market – to $134,100 in 2023, and median balances from $27,400 in 2022 to $35,300 in 2023 (see Determine 1). The large distinction between the median and the typical is because of a small variety of accounts which have actually massive balances. Common balances are extra typical of long-tenured, extra prosperous contributors, whereas the median represents the standard participant.

The great efficiency of all the indications in 2023, nonetheless, doesn’t imply all is effectively. Balances are literally fairly puny. Take into account the holdings of these approaching retirement – ages 55-64. As one would count on, these balances are a lot bigger than these for the complete participant inhabitants. However nonetheless, the median is just $87,600, which signifies that half of contributors have lower than this quantity and half have extra. Furthermore, Vanguard tends to manage bigger plans, so the plans are higher designed than common and contributors have larger incomes. In different phrases, it presents one of the best face of the 401(okay) system.

However, the balances at any single firm don’t present a whole image of retirement preparedness. First, when contributors change jobs, their 401(okay) accounts might stay with their outdated employer, so people might have multiple 401(okay) account. Second, 401(okay) balances are sometimes rolled over to an IRA, and monetary providers corporations can not observe mixed 401(okay)/IRA holdings. Third, by necessity, balances are offered on a person, fairly than a family, foundation. Whereas a whole image solely emerges from family surveys, the Vanguard report all the time supplies fascinating data on traits.

And the traits needs to be good, as a result of a lot of adjustments have improved the functioning of 401(okay) plans. Virtually 60 % of the Vanguard plans now have auto-enrollment; target-date funds at the moment are nearly the common default funding; and costs have declined markedly. Regardless of these enhancements, nonetheless, the longer-term image isn’t encouraging – notably as soon as one accounts for inflation.

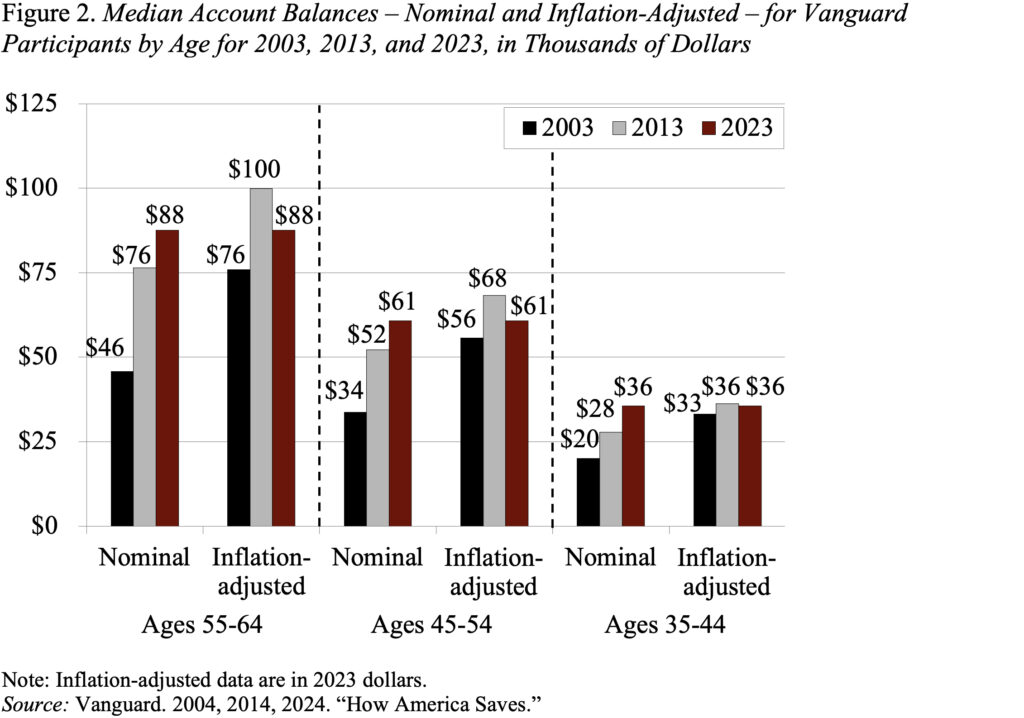

Determine 2 exhibits balances by age for 3 years – 2003, 2013, and 2023 – for 3 completely different age teams – 55-64, 45-54, and 35-44. Beginning first with the pre-retirees – in nominal phrases, 2023 balances of $88,000 had been larger than balances in 2013 and nearly double these in 2003. However taking inflation into consideration produces a fairly completely different image – 2023 balances had been solely barely larger than these in 2003 and truly decrease than the 2013 quantity. The sample for youthful teams is comparable – rising nominal balances over time, however roughly flat balances as soon as the numbers are adjusted for inflation.

For my part, the trade and policymakers have accomplished every little thing they’ll to make the 401(okay) system work as successfully as doable. Because of this, people who find themselves constantly coated by 401(okay) plans can and do amass substantial quantities of cash. However the typical employee, who strikes out and in of protection, can not. In actual phrases – adjusted for inflation – 2023 balances for the standard participant in every age group are under what they had been in 2013. No system can work successfully with out steady protection, and that purpose will solely be achieved with a nationwide mandate that gives for computerized office financial savings for everybody.