{kind=link}

Personal sector weighs on GDP

Australia’s GDP rose by a modest 0.2% in Q2 2024, bringing annual development to simply 1%, barely under expectations and underscoring persistent financial challenges, notably within the non-public sector, in line with NAB chief economist Alan Oster (pictured above).

“Financial development stays very weak,” Oster mentioned.

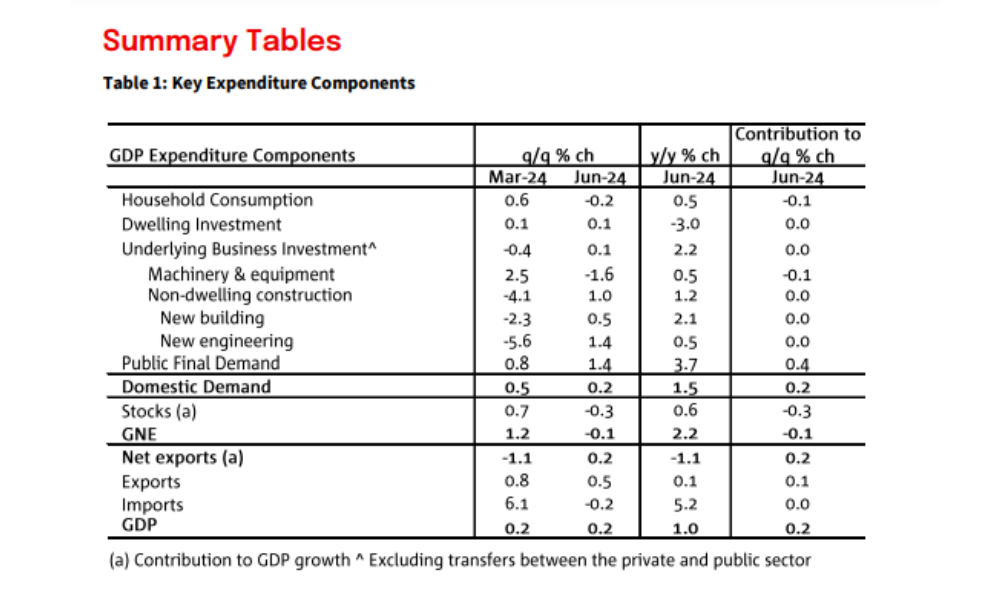

Whereas web exports and public demand supplied some much-needed help, different key areas – notably enterprise and dwelling funding – made no contribution to the financial system’s development.

The Australian financial system has now seen six consecutive quarters of declining per capita GDP, a reality obscured by robust inhabitants development.

“The general public sector has been an essential help with non-public sector elements very weak,” Oster mentioned.

The weak point in non-public sector efficiency continues to place stress on financial restoration, whilst inhabitants development pushes up headline figures.

Family spending declines

Family consumption, which accounts for a good portion of financial exercise, fell by 0.2% in Q2, the primary quarterly decline since Q3 2023.

Notably, discretionary spending dropped by 1.1%, with steep declines in classes resembling transport companies (-4.4%), clothes and footwear (-1.6%), and eating (-1.5%).

“Households are feeling the pinch, particularly in discretionary spending,” Oster mentioned, attributing the declines to the continued results of inflation and excessive rates of interest, which have eroded buying energy.

Nonetheless, spending on important gadgets like electrical energy and family fuels rose by 2.4%, highlighting the shift in family consumption patterns as inflation and rates of interest proceed to chew into budgets.

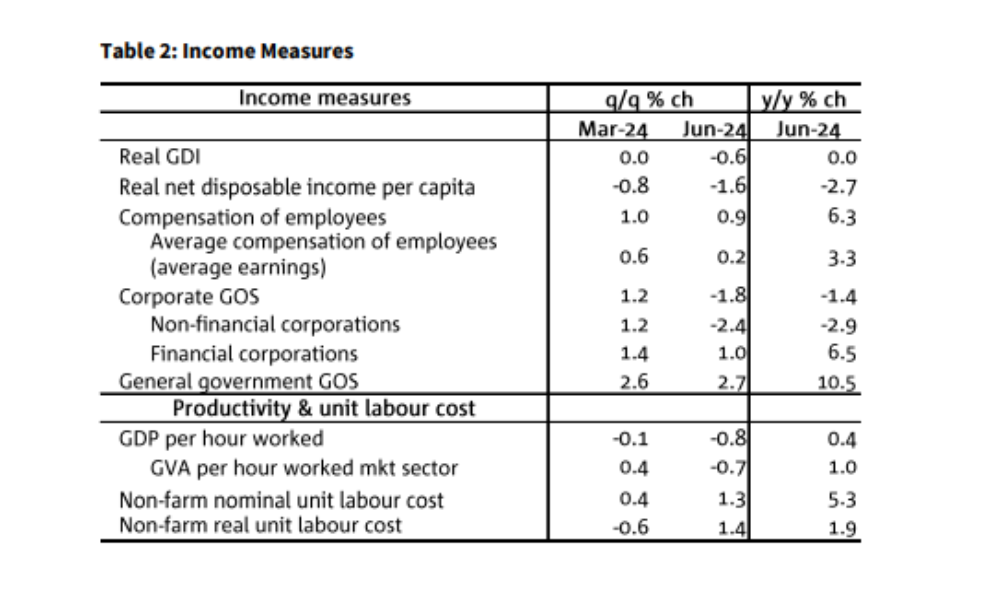

Regardless of a slight 0.9% improve in family disposable incomes, actual shopping for energy stays underneath stress, particularly with revenue taxes ticking up and inflation nonetheless persistent, although easing regularly.

Productiveness stays a key concern

The general public sector continued to be an important driver of financial exercise, with public closing demand rising by 1.4% in Q2.

Authorities consumption, notably in well being companies, was a major contributor to development.

Nonetheless, Oster identified the imbalance between the private and non-private sectors.

“Productiveness has been weighed by weak mining output and robust public sector employment development,” he mentioned.

Enterprise funding remained flat, edging up solely 0.1% in Q2.

Dwelling funding noticed equally weak outcomes, rising by a mere 0.1%, leaving it 3.0% under ranges from a 12 months in the past, NAB reported.

NAB financial outlook: Gradual restoration forward

Wanting forward, Oster believes the Australian financial system may even see slight enchancment within the second half of 2024 however warns that development is more likely to stay under pattern.

“We anticipate development to enhance however stay under pattern in H2,” he mentioned.

Whereas inflation is regularly easing, it stays elevated, and weak productiveness continues to push up unit labor prices. NAB forecasts GDP development of round 1% for the 12 months, decrease than the Reserve Financial institution of Australia’s projection of 1.7%.

As for rates of interest, Oster is cautious about the potential of a charge reduce. “We proceed to anticipate the situations for a reduce won’t be in place this 12 months,” he mentioned, noting that NAB expects the primary charge reduce to happen in Might 2025, though he acknowledged that the timing may change relying on inflation traits and the broader financial surroundings.

Get the most popular and freshest mortgage information delivered proper into your inbox. Subscribe now to our FREE day by day e-newsletter.

Associated Tales

Sustain with the newest information and occasions

Be part of our mailing record, it’s free!