{kind=link}

You’ve in all probability heard in regards to the large NAR settlement that would fully change how actual property works going ahead.

However in the event you haven’t, or are not sure of what’s altering, there are two new guidelines set to go into impact August seventeenth, 2024.

The primary is that provides of compensation will likely be prohibited on A number of Itemizing Providers (MLSs).

In different phrases, itemizing brokers gained’t be capable to say they’re providing 2% or 3% to the client’s agent on the MLS.

The logic is that any such co-op fee leaves the client out of the dialog, which isn’t truthful if the client finally pays for it.

Whereas they might not pay it straight, a pre-determined fee may lead to a better gross sales worth.

As well as, there’s additionally not a lot transparency in regards to the charge, nor do shoppers know such charges are negotiable.

Merely put, this transfer is meant to spice up transparency and ideally decrease charges for shoppers by letting patrons negotiate with their brokers individually.

However there may be some unintended penalties because of this, which I’ll get to in a second.

The opposite main change is that patrons should signal a written settlement earlier than they’ll tour a property. At the moment, compensation may even be mentioned.

Actual Property Agent Charges Could Drop, Nonetheless…

Now about these unintended penalties I alluded to. Whereas the usual fee may go down thanks to those new guidelines, from say 2.5% to 1.5% and even 1% on the buy-side, there’s nonetheless the query of who pays it.

As famous, the vendor can proceed to supply purchaser agent compensation, it simply can’t be included on the MLS.

So hypothetically this might be conveyed in different methods, resembling on their very own brokerage web site itemizing, through telephone name, textual content, and so on. Not less than that’s what some assume for now.

That too might change if this evolves right into a state of affairs the place co-op fee is totally banned and decoupled.

However as of now, many actual property brokers assume they’ll nonetheless make affords of compensation through channels aside from the MLS.

In idea, this implies nothing may change in some transactions. For instance, a vendor might inform their itemizing agent to supply 2.5% to a purchaser’s agent. And a purchaser’s agent might ask for two.5% from their purchaser.

The logic right here is that they wish to transfer the property shortly, and being stingy might backfire.

In the event that they solely provide 1%, or provide nothing in any respect, a purchaser’s agent might must make up the shortfall with the house purchaser.

At that time, the client might balk or just be unable to give you the out-of-pocket funds to pay it.

When all is claimed and achieved, the vendor may lose a purchaser and kick themselves for not simply providing compensation and getting an honest gross sales worth.

On the opposite facet of the coin, a purchaser may be OK with getting nothing from the vendor and paying their agent themselves to sweeten their provide (assuming a number of bidders).

So there are quite a lot of situations right here and nonetheless quite a lot of uncertainty about how this might evolve.

However some issues I’ve seen so far are an actual property signal that makes clear the vendor will provide purchaser agent compensation, patrons forgoing an agent and contacting the itemizing agent straight, and a few even signing a type that claims they gained’t tour houses that don’t provide compensation to the client’s agent.

It’s going to be very attention-grabbing. And like I mentioned, it’s nonetheless very fluid and there’s lots we nonetheless don’t know.

How Will Dwelling Patrons Pay for Purchaser Agent Compensation?

Starting August seventeenth, 2024, residence patrons could have a number of choices to pay the client agent compensation.

They’ll preserve the established order and hope the vendor affords it, with the client’s agent charge popping out of the gross sales proceeds.

They’ll go direct to the itemizing agent and request a twin company, the place the itemizing agent represents each purchaser and vendor.

They’ll rent an actual property lawyer and have them information them by way of the method for a flat charge, assuming such a setup is permitted.

Or they’ll foot the invoice themselves by merely paying it out of pocket.

Some people appear to assume patrons are going to more and more pay the client’s agent fee themselves.

Whereas I don’t absolutely agree, given the truth that most Individuals can barely scrape collectively their down fee and shutting prices funds, it’ll seemingly occur extra regularly.

And if and when it does, it might burden some residence patrons, particularly the aforementioned who don’t have deep pockets.

That brings us to the unique query on this publish. In the event that they’re unable to pay money, can actual property commissions be financed as a substitute?

Actual Property Commissions Can’t Be Financed

In the meanwhile, actual property commissions can’t be rolled into the mortgage quantity, aka financed.

This goes for all main mortgage sorts, together with conforming loans backed by Fannie Mae and Freddie Mac, together with FHA loans and VA loans.

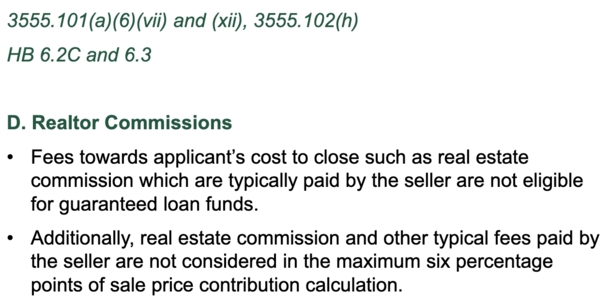

The identical is true of USDA loans for that matter as effectively, as seen within the screenshot above.

Nonetheless, it’s essential to notice that actual property commissions aren’t thought-about within the most celebration contribution (IPC) calculations.

So you may get the vendor to pay your purchaser’s agent and nonetheless get the complete quantity of vendor concessions for different stuff like lender charges and third-party prices, together with title insurance coverage and residential appraisal.

Each Fannie Mae and Freddie Mac issued letters to substantiate that actual property agent commissions gained’t rely in direction of the IPC limits in the event that they proceed to be usually paid by sellers.

And the VA launched a round as a result of their rules specify {that a} veteran can’t pay for actual property brokerage costs.

In mild of the settlement, veterans will likely be permitted to pay it, assuming buyer-broker costs are usually not included within the mortgage quantity. As well as, it gained’t be thought-about a concession.

As for why actual property agent commissions can’t be financed, for one it by no means actually got here up for the reason that vendor would usually pay the client’s agent through gross sales proceeds.

This was primarily a non-issue previous to the landmark NAR settlement.

The opposite wrinkle is loan-to-value ratio (LTV) restrictions. If the borrower had so as to add a further 2-3% of the acquisition worth in actual property agent commissions to their mortgage quantity, they may not qualify.

That is very true when placing down 0% to three.5%, which is sort of frequent as of late. The houses merely gained’t appraise and the max LTVs will likely be exceeded.

May this variation sooner or later? It’s doable however not essentially possible for the problems talked about above.

What About Utilizing a Lender Credit score to Pay Actual Property Fee?

Now let’s speak about a possible answer if the vendor gained’t provide purchaser agent compensation and also you don’t have money to pay it out of pocket.

One viable possibility might be using a lender credit score, which technically can’t be used for actual property agent commissions.

Nonetheless, if the lender credit score have been used for different prices, resembling lender charges and third-party charges, it will liberate money for use elsewhere.

For instance, say you’ve acquired a $500,000 mortgage quantity and the client’s agent needs you to pay them 1%.

A 1% lender credit score frees up $5,000 in money to pay these different prices, permitting a purchaser to compensate their agent with the freed up money.

It’s nonetheless very early goings and unclear if such an association will likely be permitted. In spite of everything, co-op fee may be on the chopping block subsequent. However it’s one thing to think about.

Finally, it’s going to seemingly be finest for many residence sellers to proceed to pay the client’s agent through the gross sales proceeds.

This could maximize the variety of eligible patrons/bidders and never shut out first-time residence patrons, who’re most in danger as a consequence of restricted funds.

The excellent news is these actual property agent charges might come down because of this, saving each patrons and sellers some cash alongside the best way.

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on Twitter for warm takes.