")

{kind=link}

Introduction

Established in 1935 and headquartered in Mumbai, Cipla Ltd. is a worldwide pharmaceutical firm famend for its sturdy presence in key markets reminiscent of India, South Africa, North America, and different regulated and rising areas. Cipla is devoted to offering high-quality, reasonably priced drugs and has a various portfolio that features therapies for respiratory, cardiovascular, and infectious illnesses, amongst others. With a dedication to innovation and sustainability, Cipla continues to make vital strides in enhancing healthcare entry and outcomes worldwide.

Product Portfolio

– Generics and branded generics

– Over-the-counter (OTC) merchandise

– Specialty and shopper well being merchandise

– Respiratory medication

– Anti-retroviral drugs

– Urology, cardiology, anti-infective, CNS, and different therapeutic segments

– 1500+ merchandise in 65 therapeutic classes obtainable in over 50 dosage varieties

Subsidiaries as of FY23:

– 45 subsidiaries

– 8 affiliate corporations

Progress Methods of CIPLA

– Cipla has achieved gross sales exceeding $500 million up to now 4 years, positioning it because the fastest-growing US generic pharmaceutical firm amongst its rivals.

– The corporate’s Indian operations have skilled sturdy progress of 10% in FY24, pushed by elevated demand for branded prescription drugs and commerce generics.

-Cipla boosted its market share in North America by 15.5% in FY24, pushed by vital shares in key markets reminiscent of Lanreotide and Albuterol.

-South Africa’s Non-public Market witnessed distinctive year-on-year progress of 26% in native forex phrases, surpassing general market progress charges.

-Strategic filings embrace 5 respiratory property, together with gSymbicort and gQvar, with launches anticipated inside the subsequent three years.

-The corporate has filed 12 property in peptides and sophisticated generics, slated for launch over the following 2-4 years, illustrating a centered enlargement into specialised segments.

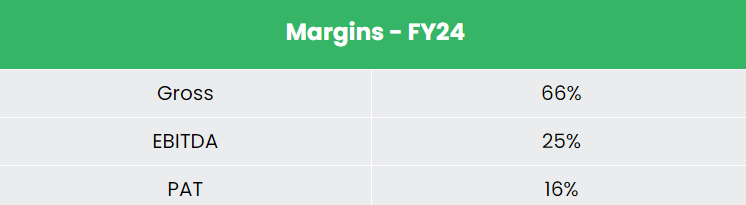

CIPLA Ltd Monetary Highlights

Q4FY24

– Income: Rs.6,163 crore (7% improve YoY)

– Working revenue: Rs.1,316 crore (12% improve YoY)

– Internet revenue: Rs.932 crore (79% improve YoY)

– Working revenue margin: 21% (54 bps YoY enchancment)

– Internet revenue margin: 15% (587 bps YoY enchancment)

– R&D expenditure: Rs.444 crore (19% YoY improve)

FY24

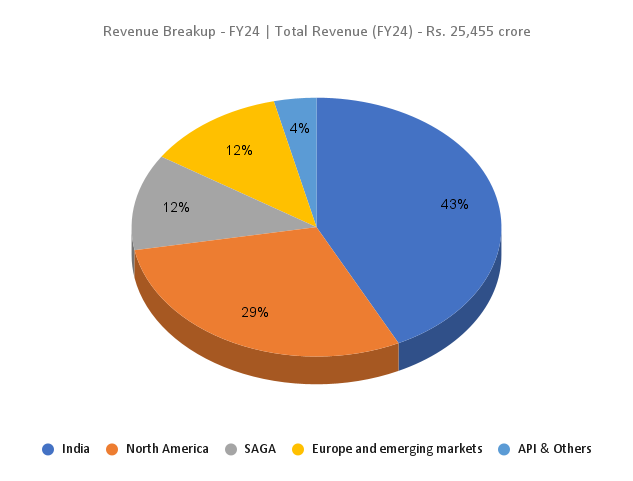

– Income: Rs.25,455 crore (14% improve YoY)

– Working revenue: Rs.6,233 crore (26% improve YoY)

– Internet revenue: Rs.4,106 crore (47% improve YoY)

Monetary Efficiency (FY19-24)

– Income and PAT CAGR: 10% and 25%

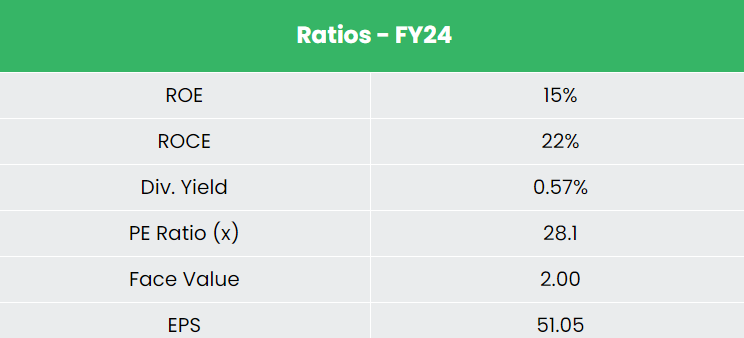

– Common 5-year ROE: 14%

– Common 5-year ROCE: 17%

– Debt-to-equity ratio: 0.02

Trade Outlook

– India is the most important supplier of generic medication globally

– Indian pharmaceutical business: third largest by quantity, 14th largest by worth

– Projected CAGR of over 10% to achieve US$ 130 billion by 2030 and US$ 450 billion by 2047

– Largest variety of USFDA-compliant pharmaceutical vegetation exterior the US

– 2,000+ WHO-GMP authorized services serving demand from 150+ nations

Progress Drivers

– 100% FDI allowed via automated route for Greenfield prescription drugs tasks

– Rs.1,000 crore (US$ 120 million) earmarked for promotion of bulk drug parks in FY25

– PLI scheme for prescription drugs with a complete outlay of Rs. 15,000 crore (US$ 2.04 billion) from 2020-21 to 2028-29

Aggressive Benefit

In comparison with rivals like Solar Prescribed drugs Industries Ltd and Lupin Ltd, Cipla stands out as an undervalued inventory with vital potential for P/E enlargement, supported by its sturdy margin and earnings progress

Outlook

- Cipla Ltd. has been essential in making reasonably priced HIV remedy accessible from India.

- Cipla is growing new merchandise together with inhaled insulin and plazomicin, with extra within the pipeline.

- The corporate goals to rank 2nd in OTC markets and launch peptide property in FY25.

- Cipla is growing advanced ANDA merchandise for its future portfolio.

- Cipla plans to take a position Rs.1,500 crore to reinforce manufacturing and sustainability, with an EBITDA steerage of 24.5% to 25.5%.

Valuation

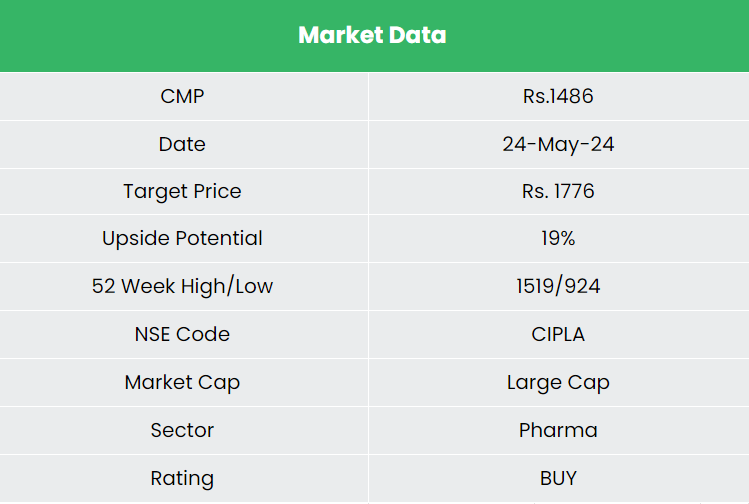

With an improved product combine, deepening distribution community, and technological improvements, Cipla is anticipated to see appreciable progress in income and margins. A BUY ranking is really useful with a goal worth (TP) of Rs. 1,776, 32x FY26E EPS.

Dangers

– Foreign exchange threat attributable to vital operations in international markets.

– Regulatory threat, together with scrutiny by regulatory companies just like the USFDA.

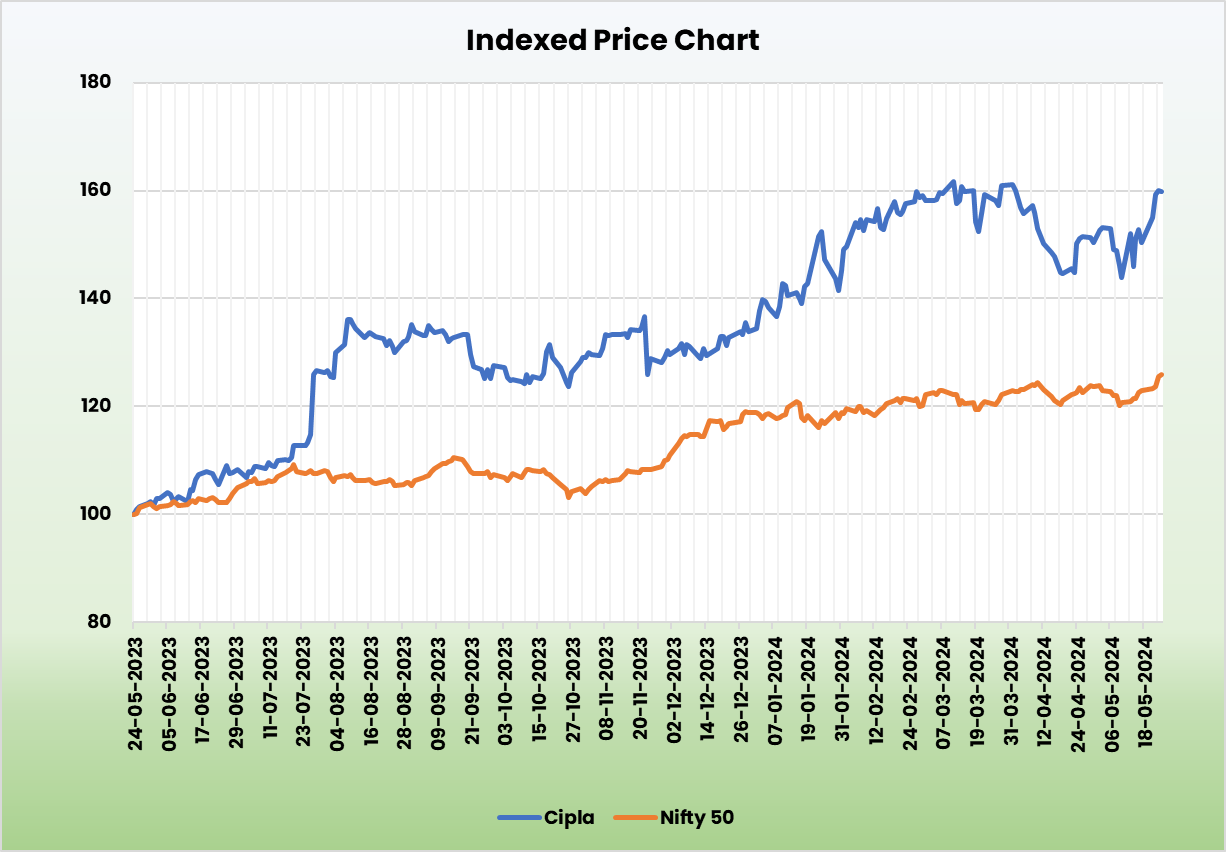

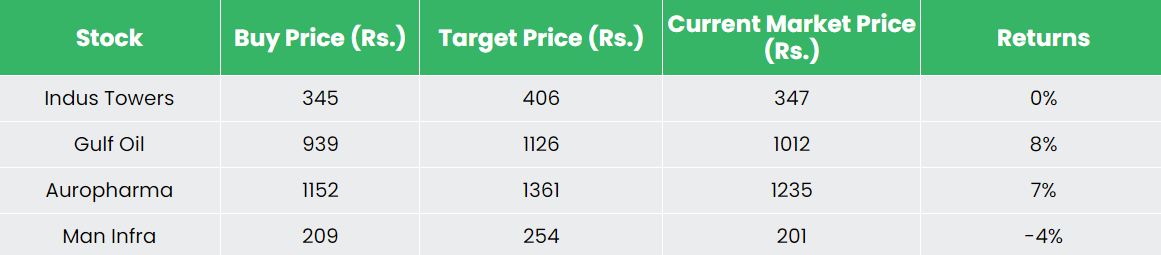

Recap of our earlier suggestions (As on 24 Might 2024)

Different articles you might like

Put up Views:

1,537