{kind=link}

Due to everybody who responded to the latest ebook giveaway. Your encouragement and type phrases had been uplifting. The responses gave me plenty of matters to concentrate on in 2025. I acquired 104 responses. Congrats to the winners.

Additionally, just a few weeks again, I requested in your assist in getting me over the 1,000 subscriber mark on YouTube. The response was unbelievable, taking me excessive that day! Thanks. I’ve already surpassed 1,200, and I’m trying ahead to the subsequent milestones.

Each January for the previous 20+ years, I’ve analyzed my funding portfolios and adjusted when needed.

Why January?

December is simply too busy for me. January is the calm after the vacation storm, and many people used the time to rethink our funds.

DIY buyers ought to contemplate rebalancing their portfolios yearly — however no extra continuously than yearly.

Much less continuously is OK. Nonetheless, rebalancing must be systematic and unattached to emotional triggers like market fluctuations or private occasions.

Your rebalance date may very well be each 18 or 24 months. Choose your rebalance frequency, set a reminder, and observe via systematically. Each twelve months is an effective rule of thumb, however it doesn’t must be close to the brand new 12 months.

Annual portfolio scrutiny is extra than simply rebalancing. My portfolio is not fairly the place I would like it to be but. So, I take advantage of the annual rebalance course of to streamline.

I streamline by:

- Lowering fund redundancy and overlap, consolidating into core portfolio holdings.

- Promoting particular person shares not serving my funding goals, transferring cash into core index holdings.

A number of Accounts

A typical drawback with portfolio rebalancing is figuring out your present asset allocation when you have a number of accounts and brokers.

A technique round that is to rebalance every account individually. This technique is cumbersome when some accounts are a lot smaller than others. I choose to rebalance by all my holdings collectively.

However with out realizing your present asset allocation, you’ll be able to’t rebalance to the goal asset allocation.

Streamlining to fewer accounts and fewer holdings makes the rebalancing course of simpler.

Between Mrs. RBD and I, we now have:

- Two taxable accounts

- Two conventional IRAs

- Two Roth IRAs

- Two former employer-sponsored accounts

- One SEP IRA

We’ve got some room to consolidate accounts right here and can achieve this when the time is correct.

To maintain issues simpler to handle, I put money into only one fund within the smaller accounts (a complete market fund), then use the bigger accounts to regulate to succeed in our goal asset allocation.

I take advantage of just a few totally different instruments to get a consolidated view of all of our holdings and use this information to make changes to our portfolio.

Discovering Your Present Asset Allocation

Step one in rebalancing is to find out your present asset allocation.

This may be a straightforward activity if all of your cash is in a single place. Some brokers are superb at this. However when you have cash in a number of accounts from a number of account suppliers, it is tougher.

For instance, I’ve spoken to people with a portion of their retirement cash in an IRA with a monetary advisor however one other portion self-managed via an employer-sponsored account or particular person funding account.

I’ve six accounts with Constancy, and it does a surprisingly awful job of giving me portfolio insights throughout my varied accounts. You probably have accounts outdoors the umbrella of a major dealer, it turns into tougher.

I’ve turned to instruments through the years to determine it out. DIY planning instruments like Boldin and ProjectionLab don’t supply this performance but, so we now have to look elsewhere.

The three instruments I take advantage of are the main focus of the companion video I made for this put up. Test it out on YouTube or beneath.

Spreadsheets

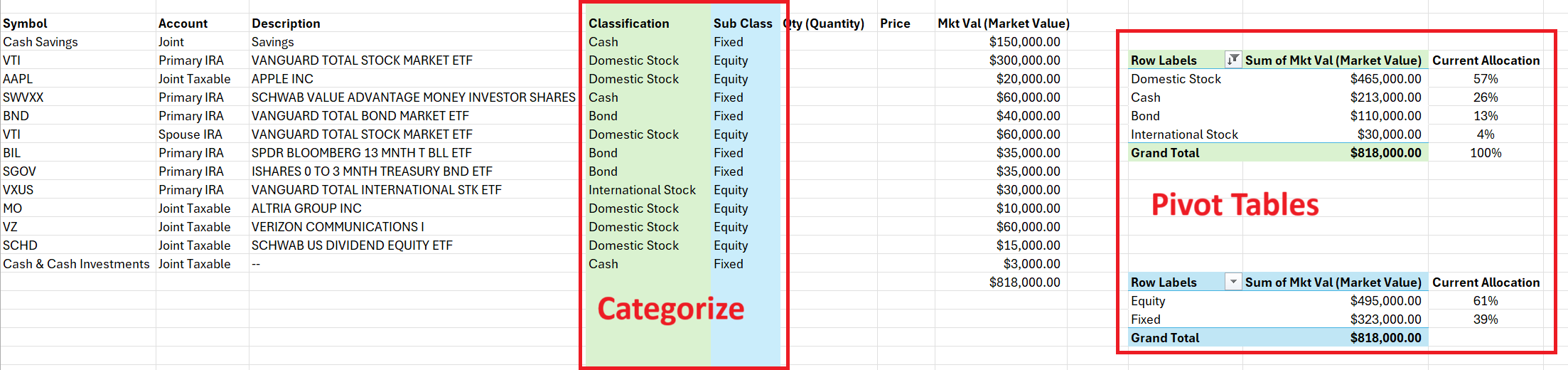

I take advantage of the spreadsheet technique to create the charts on my Portfolio web page however I’ve slowed in updating it commonly as a result of it’s a relatively painstaking course of to make charts like this:

The method entails (see video):

- Downloading spreadsheet information from the holdings view of your a number of brokerage accounts

- Combining all of the holdings and market values right into a desk

- Inserting columns and categorizing every holding (manually)

- Then, pivot tables to calculate the present allocation percentages.

Spreadsheets are free, customizable, and acquainted to most, so they’re an appropriate possibility. However the extra sophisticated your monetary state of affairs, the extra guide this course of turns into.

I’m extra continuously choosing instruments to assist analyze my financials as a result of they work higher than most spreadsheets I can construct.

Morningstar Investor (paid) is a brand new software that I’m experimenting with and like to this point. It does a wonderful job of consolidating information and offering portfolio insights.

Empower (free, with a caveat) does a great job of aggregating account information, amongst its different analytical capabilities.

Morningstar Investor

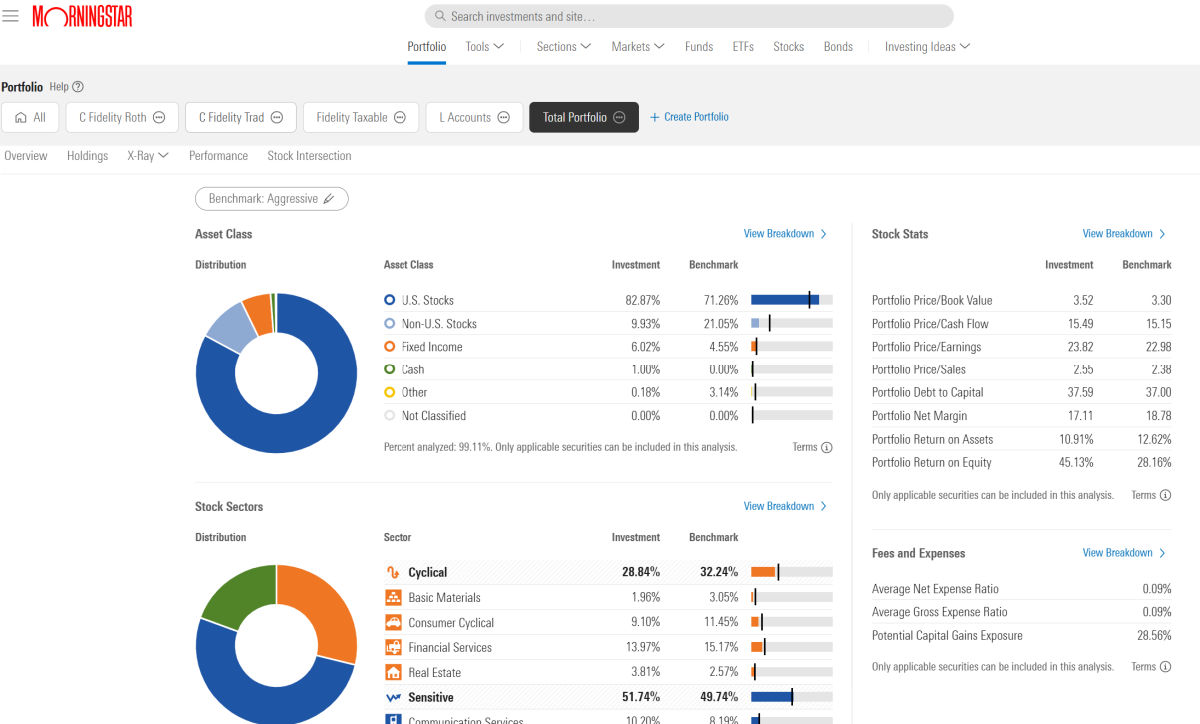

Morningstar Investor is the flagship portfolio monitoring on the Morningstar web site. Identified for its fund scores and retirement insights, Morningstar imports your portfolio information (through third-party connectivity) from a number of sources and offers complete evaluation.

For instance, I’ve related my six Constancy accounts, my spouse’s two, and my M1 Finance account. Then, I mix all of them into one portfolio view (demonstrated within the video).

It mechanically categorizes every fund and ETF and offers your present asset allocation. It could actually additionally take a look at every mutual fund or ETF you personal, and extract particular person inventory insights, then present you the overlap between holdings.

It additionally offers benchmark portfolios to check towards. I choose a extra personalised goal asset allocation:

- 75% U.S. shares

- 15% Worldwide shares

- 10% Bonds

The software shortly tells me that my portfolio is chubby U.S. shares and underweight worldwide shares and bonds.

Now, I can alter my retirement accounts.

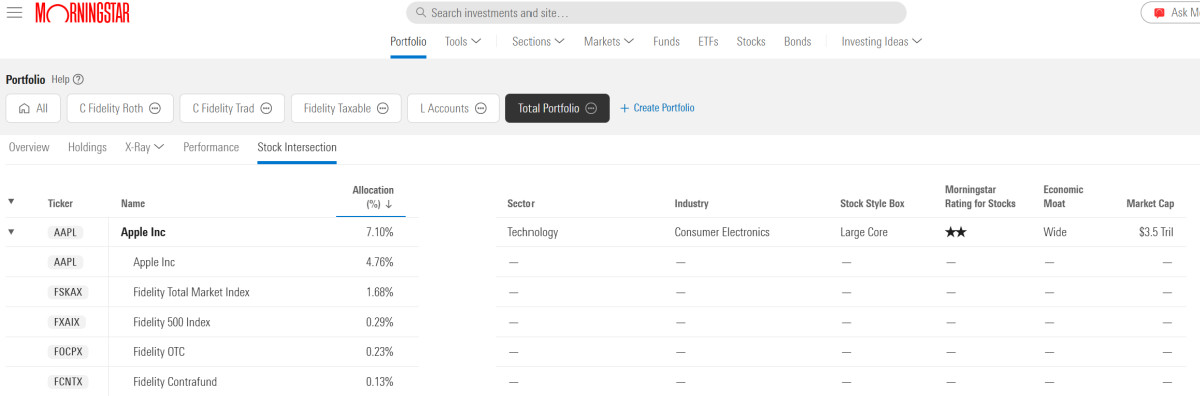

As a bonus, the Inventory Intersection software reveals what funds maintain shares and the way a lot, based mostly on the quantity you’ve invested within the fund.

For instance, I personal Apple inventory, plus just a few funds that maintain Apple as their prime holdings. The software reveals me my whole publicity to Apple throughout all my holdings.

That is the primary software I’ve seen that’s able to this:

Subscribers can click on into any particular person holding to search out fund and inventory experiences, proprietary scores, charts, and key statistics.

New customers can get a 14-day free trial. After that, it’s $199 for the primary 12 months.

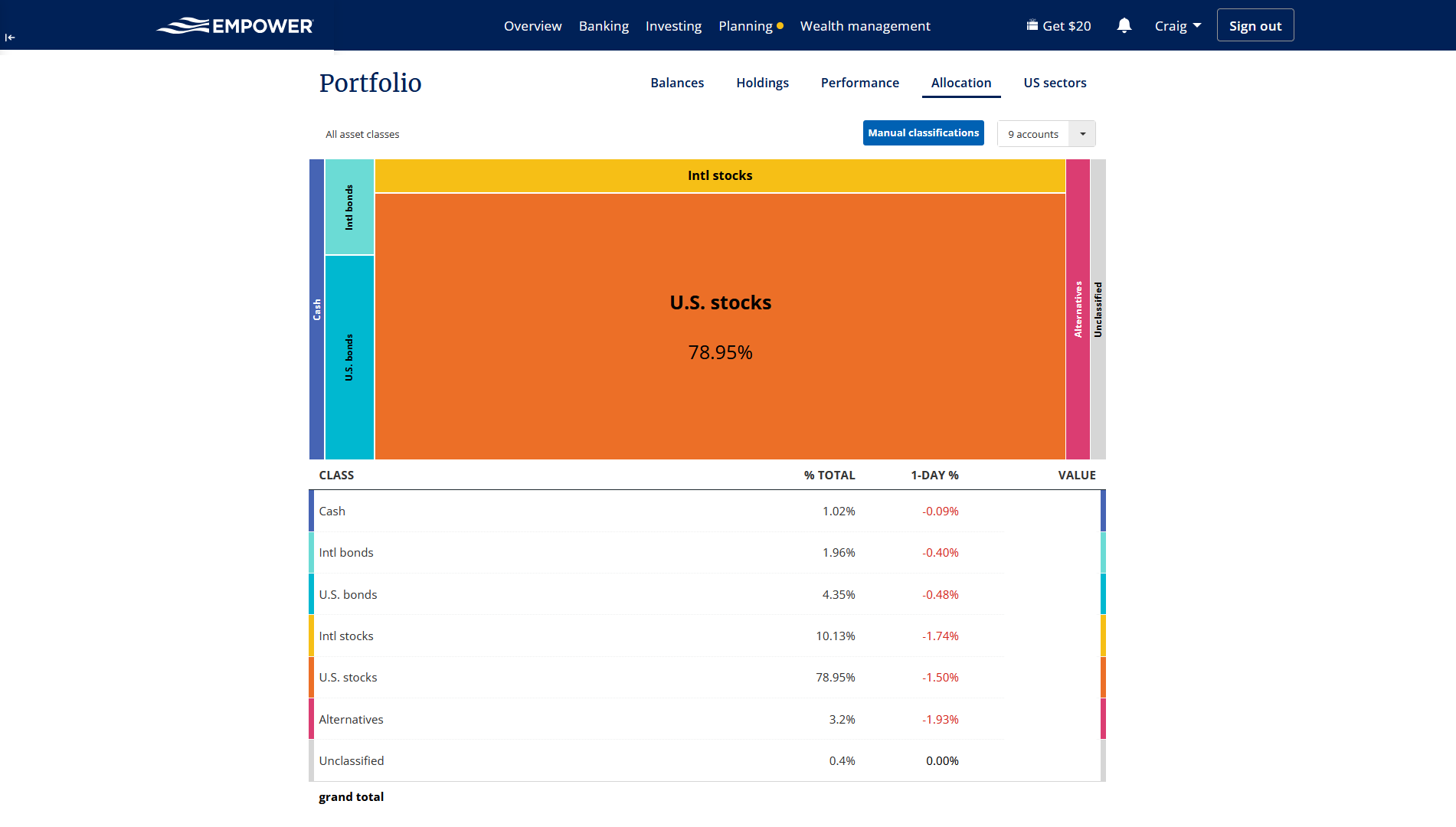

Empower

Empower is a free software that I’ve been utilizing for about 10 years. Previously often called Private Capital, Empower is a portfolio aggregator and internet value monitoring that analyzes all of your monetary accounts into visualizations.

This software additionally mechanically categorizes your funding however doesn’t provide the granularity that Morningstar does throughout the funds (there’s no Inventory Intersection equal).

Right here’s the view I reveal within the video:

Empower struggles a bit with funding categorization, however customers can modify categorizations to their liking and choose which accounts to incorporate on this view.

Empower struggles a bit with funding categorization, however customers can modify categorizations to their liking and choose which accounts to incorporate on this view.

On this case, I can see the place my portfolio shouldn’t be aligned with my targets, and I can alter my holdings.

Empower is free to make use of. It helps third-party information connectivity, so you’ll be able to herald all of your accounts for complete evaluation. Connectivity has improved lately.

It has a good retirement calculator, too, related however not as customizable or sturdy as Boldin or ProjectionLab.

The principle downside of Empower is that it’s a lead era software for the corporate, providing wealth administration providers.

So, when you enroll and join your accounts, a wealth advisor might attain out to you. Saying no is okay, however some folks discover this to be intrusive. Most individuals are OK with that tradeoff as a result of it’s a highly effective free software.

Decide Your Goal Asset Allocation

Your very best goal asset allocation is the proportion of portfolio property invested in shares, bonds, and money.

We will decide our asset allocation utilizing a easy rule of thumb I name “minus your age“, which seems at age and threat tolerance.

To search out your very best asset allocation, subtract your age from one of many following numbers related together with your threat tolerance:

- Conservative – 120

- Reasonable – 130

- Aggressive – 140

The result’s the quantity to allocate towards shares. The steadiness is then invested in bonds or different fastened property.

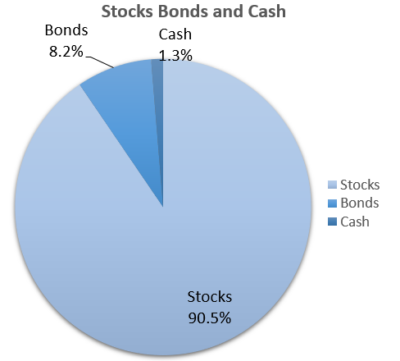

For instance, my threat tolerance is aggressive, and I’m 49 years outdated.

=140 - 49 = 91

So, I’d goal roughly 91% shares and 9 % bonds. See above.

Rebalance to Your Goal Allocation

After you have your present asset allocation and your goal, calculate the distinction between the 2. Then, go into your brokerage account and make the changes.

Within the video instance, I take advantage of the next instance the place I break it out to incorporate U.S. shares, worldwide shares, bonds, and money:

With the distinction calculated, the ultimate step is to enter the brokerage account and:

- Promote $56,000 of home inventory funds

- Promote/switch $49,400 of money held in a cash market account

- Purchase $53,600 value of bond funds

- Purchase $52,800 in worldwide shares

As I identified just a few occasions within the video, this doesn’t must be a exact train. The market fluctuates each day. However you need to get near your goal asset allocation yearly to take care of your retirement plan.

Why Ought to We Rebalance?

Craig Stephens

Craig is a former IT skilled who left his 19-year profession to be a full-time finance author. A DIY investor since 1995, he began Retire Earlier than Dad in 2013 as a inventive outlet to share his funding portfolios. Craig studied Finance at Michigan State College and lives in Northern Virginia together with his spouse and three youngsters. Learn extra.

Favourite instruments and funding providers (Sponsored):

Boldin — Spreadsheets are inadequate. Construct monetary confidence. (assessment)

Morningstar Investor — Trusted fund and ETF analysis + portfolio monitoring. 7-day free trial.

Certain Dividend — Analysis dividend shares with free downloads (assessment):

Fundrise — Easy actual property and enterprise capital investing for as little as $10. (assessment)