{kind=link}

Retirement and Monetary Challenges

Regardless of hovering prices in Canada, notably in actual property, the incomes of Canadians haven’t stored tempo with the elevated value of residing. Each common and median incomes have grown at a slower charge than the patron value index (CPI). From 1980 to 2022, the common and median salaries elevated by solely 50% and 25% respectively, leading to minimal year-over-year development. In stark distinction, the CPI has surged practically 400% between 1980 and 2023, indicating that salaries haven’t stored up with the price of items and companies.

This disparity is particularly pronounced in the actual property market. For instance, the common value of a property in Toronto has skyrocketed from $75,694 in 1980 to $1,126,591 in 2023. Comparable traits are noticed in different main cities like Vancouver.

On the identical time, life expectancy in Canada has elevated from ~75 years in 1980 to ~83 years in 2023. Remarkably, 5 out of 10 Canadians aged 20 right now are anticipated to succeed in age 90, and 1 out of 10 could reside to 100. Nonetheless, this elevated longevity, whereas a optimistic growth, raises issues in regards to the affordability of retirement.

In an surroundings the place individuals reside longer however face stagnant earnings development, hovering residing prices, and excessive rates of interest, Canadians are more and more questioning their monetary future and their capability to afford a good retirement.

How A lot Cash Do You Must Retire?

Figuring out the amount of cash you want to retire is complicated and relies on a number of elements. Listed below are some key issues:

- Life-style Expectations: What sort of way of life do you envision to your retirement? What way of life are you accustomed to now?

- Mortgage Standing: Do you will have a mortgage that can nonetheless must be paid off throughout retirement?

- Life Expectancy: How lengthy do you anticipate to reside?

- Well being Situation: What’s your present well being standing, and do you anticipate any important healthcare bills?

- Extra Revenue Sources: Do you will have different sources of earnings or investments?

We explored these elements intimately in one in all our current articles.

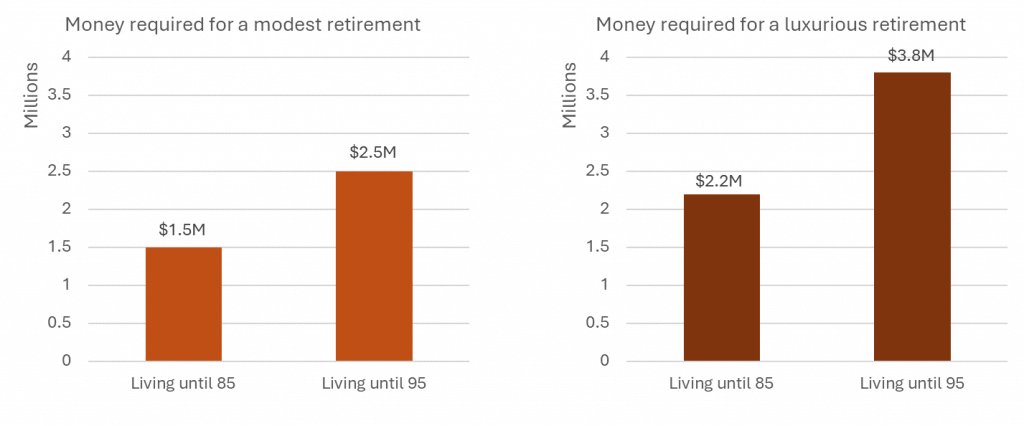

For a easy state of affairs, take into account a modest retirement for a comparatively wholesome, single one who has paid off their mortgage. This particular person ought to plan for about $1.5 million in the event that they anticipate to reside till age 85 and round $2.5 million in the event that they anticipate to reside till age 95.

For these planning a extra luxurious way of life, the numbers improve. Such a way of life would recommend planning for $2.2 million by age 85 and $3.8 million by age 95.

In the end, your retirement financial savings purpose will differ primarily based in your distinctive circumstances and the approach to life you want to preserve.

Understanding the Dimension of CPP and OAS Advantages

The Canada Pension Plan (CPP) and Previous Age Safety (OAS) advantages are essential elements of the Canadian retirement system. These are outlined profit plans that present a steady earnings stream to retirees who’ve contributed to the packages all through their working lives.

We have now performed an in depth evaluation, adjusting for inflation, to give you some approximate figures:

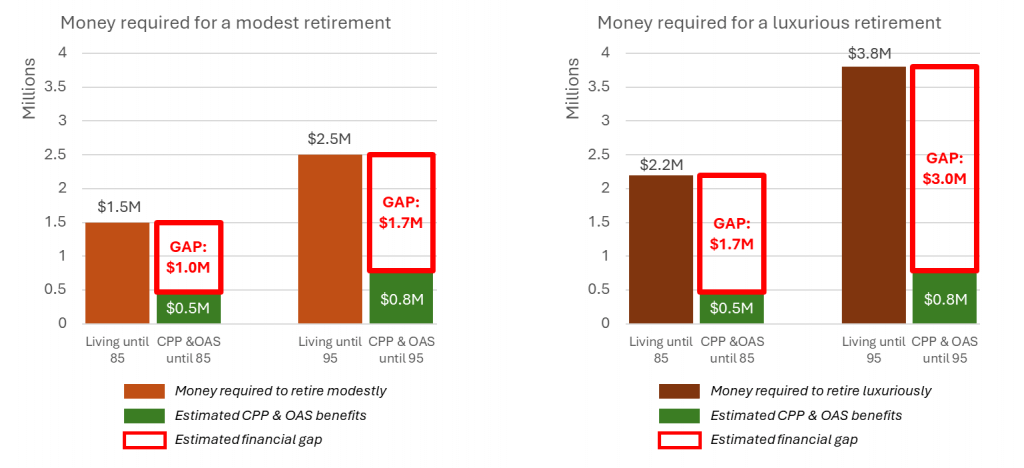

- CPP and OAS collected till the age of 85: ~$500,000

- CPP and OAS collected till the age of 95: ~$800,000

At first look, it’s evident that these quantities alone could not cowl all retirement prices.

The query then turns into, how important is the hole? Given the rising prices of residing, particularly in areas like housing and healthcare, the hole between the advantages offered by CPP and OAS and the precise value of a snug retirement might be substantial.

Many Canadians will discover that they want further financial savings, investments, or earnings sources to bridge this hole and guarantee monetary stability all through their retirement years.

How Large Is the Retirement Hole?

When evaluating the scale of CPP and OAS advantages, it’s important to think about how these quantities stack up towards the full value of retirement. Primarily based on our earlier evaluation, the approximate hole for a modest retirement is important: $1M in case you reside till age 85 and $1.7 million in case you reside till age 95. For these looking for a extra luxurious retirement, the hole turns into much more pronounced, rising to $1.7 million at age 85 and $3 million by age 95. These figures spotlight the substantial distinction between what CPP and OAS present and the precise prices required to keep up a snug lifestyle.

Bridging this hole typically requires further financial savings, investments, and cautious monetary planning to make sure a safe and fulfilling retirement.

Is the Hole Bridgeable and How?

The excellent news is that many of the retirement hole might be bridged with correct preparation. Listed below are a couple of methods to think about:

Actual Property

Traditionally, actual property has been a robust supply of economic safety and development. For instance, in case you bought an average-priced residence in 2000 for $250,000, it could be value roughly $1,125,000 right now.

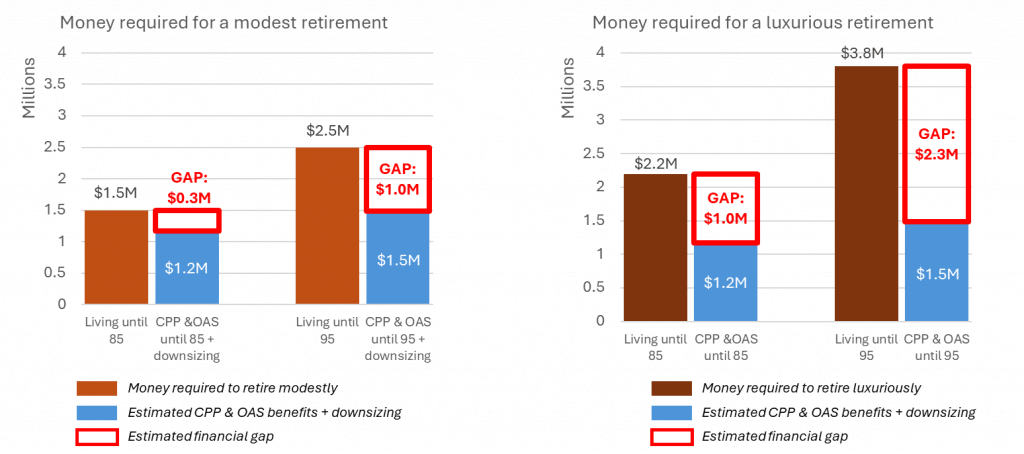

In case you have been to downsize from a $1.5 million home to an $800,000 apartment or transfer to a extra inexpensive space, your monetary retirement hole might be decreased to $200,000 for a life expectancy of 85 years and $1 million for a life expectancy of 95 years.

For these looking for a extra luxurious way of life, these numbers can be $1 million and $2.3 million for all times expectations of 85 and 95 years, respectively.

Extra Investments/Financial savings

Many Canadians have numerous sorts of investments and financial savings, together with however not restricted to RRSPs, TFSAs, GICs, and shares. These investments can present an extra supply of funds for retirement. Nonetheless, it’s vital to notice that some investments carry increased dangers than others (e.g., high-risk funding portfolios). Incorporating danger issues into your retirement monetary technique is essential to make sure a steady and safe retirement.

Proceed Working

Not everybody plans to retire absolutely. Some people could get pleasure from their work and select to increase their skilled life. Others may personal companies and handle them throughout retirement, both personally or with the assistance of further assets. Moreover, hobbies comparable to gardening, baking, portray, pictures, or writing can generally be become worthwhile ventures, offering a sustainable supply of earnings.

Rental Revenue

With excessive lease ranges in Canadian cities like Toronto, Montreal, and Vancouver, proudly owning a number of rental properties—particularly these which might be largely paid off—can generate further earnings. This rental earnings, mixed with actual property appreciation, may also help deal with retirement monetary wants. Rental properties may also be bought comparatively simply, probably leading to a big lump sum that can be utilized for retirement bills.

Dwelling with a Partner/Associate

When residing with a partner or companion, you successfully pool assets from each family members whereas needing just one property to reside in. This shared strategy can cut back the general monetary burden and assist bridge the retirement hole extra effectively.

Reverse Mortgage

A reverse mortgage is a monetary association that permits owners aged 55 and older to entry the fairness of their residence whereas persevering with to reside there. Not like conventional mortgages, the place the borrower makes funds to the lender, in a reverse mortgage, the lender makes funds to the house owner primarily based on the house’s fairness. The mortgage doesn’t must be repaid till the house owner sells the property, strikes out, or passes away.

Such a mortgage can present retirees with a gradual stream of earnings or a lump sum to cowl residing bills, healthcare prices, or different monetary wants. The quantity out there to borrow relies on elements comparable to the house’s worth, the house owner’s age, and rates of interest.

Whereas the reverse mortgage may also help enhance monetary liquidity, particularly for retirees, it is very important perceive that it reduces the house’s fairness and should influence inheritance.

Revenue-Producing Insurance coverage

Sure sorts of life insurance coverage mix each insurance coverage and wealth accumulation elements.

Complete life insurance coverage is a flexible monetary device that not solely offers lifelong protection but additionally contains a money worth element that may develop over time. Not like time period life insurance coverage, which affords safety for a selected interval with out accumulating worth, complete life insurance coverage builds money worth via common premium funds. This money worth grows at a assured charge and might be bolstered by dividends from the insurance coverage firm. Because the coverage matures, the collected money worth might be accessed for numerous monetary wants, comparable to loans or withdrawals.

Moreover, the money worth might be invested in several methods, permitting policyholders to probably develop their wealth. This twin good thing about insurance coverage safety and wealth accumulation makes complete life insurance coverage a beneficial element of a complete monetary technique. Over the long run, the coverage not solely offers monetary safety but additionally serves as a rising asset that may improve general monetary stability.

Infinite Banking

Infinite banking is a private finance strategy that makes use of an entire life insurance coverage coverage as a “private financial institution.” This strategy entails taking loans towards the coverage and rising money movement via the coverage’s dividends. On the coronary heart of infinite banking is a taking part complete life insurance coverage coverage. With such a coverage, you’ll be able to borrow cash utilizing the coverage’s money worth as collateral, eliminating the necessity to pay curiosity to exterior lenders. This setup creates a private banking system, offering fast entry to further funds via the insurance coverage firm.

This strategy affords flexibility and entry to collected funds, although it comes with its personal set of constraints. We have now a separate article that delve deeper into the main points of the infinite banking technique.

Remaining Phrases

As demonstrated, the funds required for a worry-free retirement are increased than ever, typically reaching into the thousands and thousands. Authorities packages like CPP and OAS usually are not enough to shut this hole on their very own, however quite a few methods may also help bridge it. Exploring these choices and incorporating them into your retirement planning can considerably enhance your monetary outlook.

In case you’re all in favour of discovering how some insurance coverage merchandise can improve your retirement planning, full a quote on the sidebar or go to this hyperlink.