{kind=link}

For many who begin with $100,000, Medicaid will not be a straightforward choice.

As a part of an prolonged research on the dangers confronted by households approaching retirement, we simply accomplished a venture that centered on the dangers related to medical and long-term care prices.

Because it seems, whereas medical dangers are extremely unsure and probably costly, a lot of those dangers are insured by Medicare (and Medicaid for these eligible for each applications). Lengthy-term care dangers, in distinction, should not effectively insured. Solely 3 p.c of all U.S. adults or 15 p.c of these ages 65+ have long-term care insurance coverage. And a significant discovering was that individuals had little thought of the probability of needing long-term care or of the potential prices of that care.

The implications of households underestimating their healthcare dangers are that they could not plan effectively to guard themselves in opposition to these dangers. With out the suitable insurance coverage or assets, older households might need to make substantial changes or take into account less-preferred choices. The query is, how real looking are these contingency plans?

The evaluation was based mostly on a 2024 Greenwald Analysis on-line survey of 508 people ages 48-78 with at the very least $100,000 in investable belongings. The survey included a query relating to what contingency plans respondents would take into account if they might not afford their medical or long-term care bills. These contingency plans have been then in comparison with actuality utilizing information from the Well being and Retirement Examine – a nationally consultant pattern of these over age 50 who’re interviewed each two years.

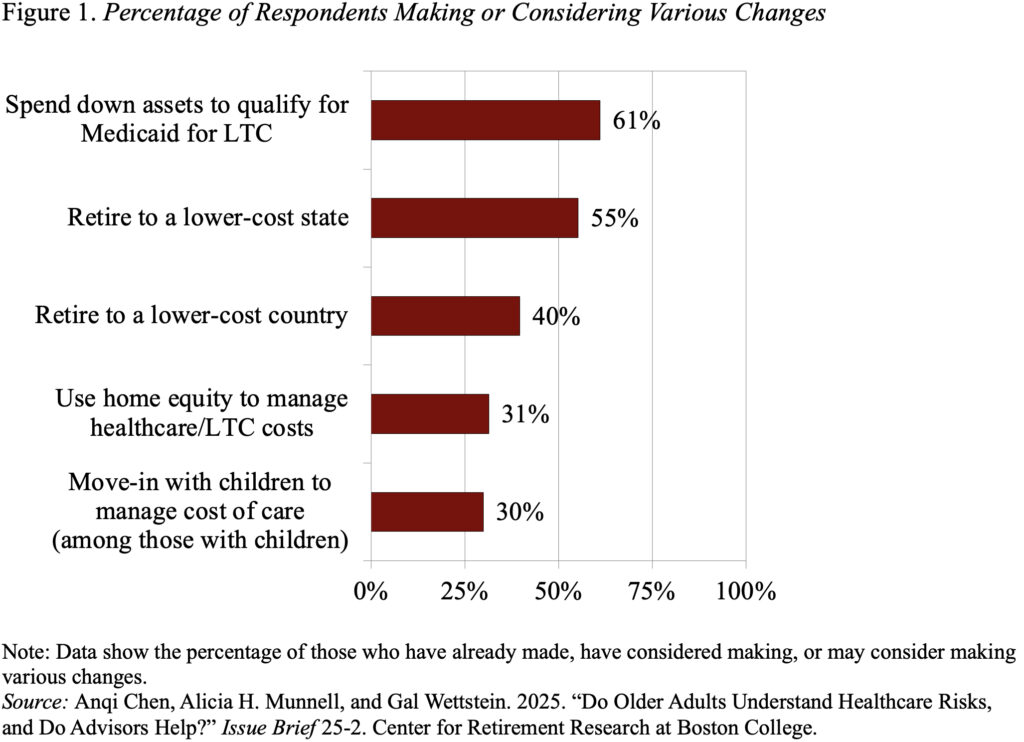

Curiously, about 60 p.c of survey respondents stated they’d take into account spending all the way down to Medicaid, whereas solely 30 p.c stated they’d think about using their house fairness or shifting in with their youngsters (see Determine 1). Nonetheless, many of those preferences might not be real looking.

Many older households who consider they will all the time fall again on Medicaid might not notice that this system’s revenue and asset limits require impoverishment. In 2025, the month-to-month revenue restrict for Medicaid eligibility for these over age 65 is often round $2,800 ($5,600 for {couples}) and the asset restrict is often $2,000 ($3,000 for {couples}), however varies by state.

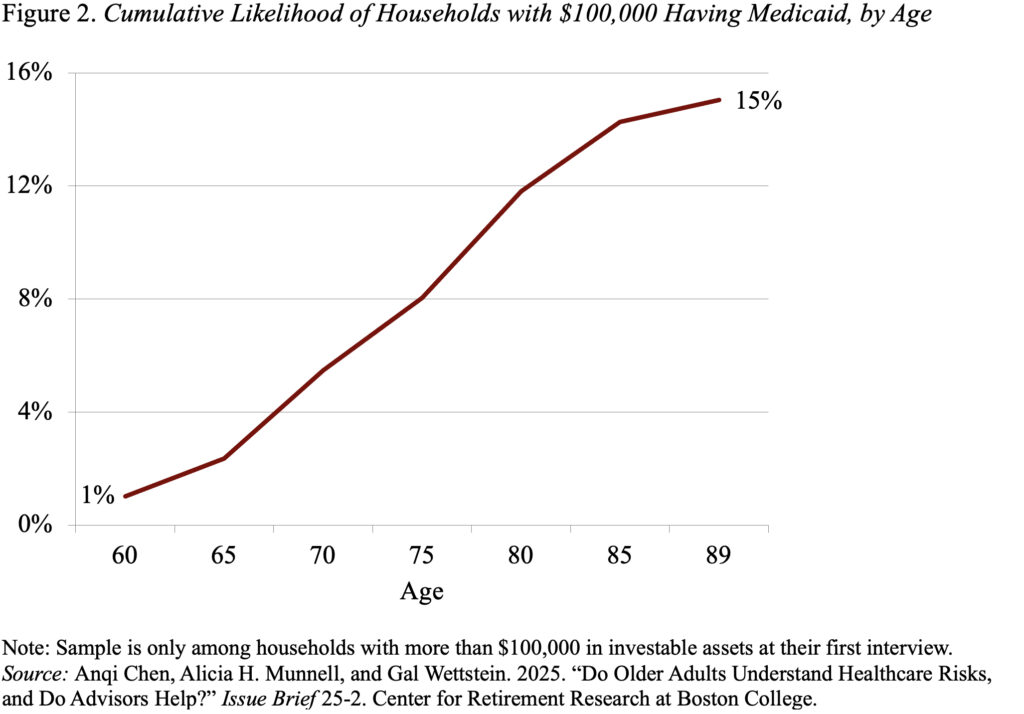

Amongst households with greater than $100,000 in investable belongings, like these in our survey, virtually none would qualify based mostly on the usual revenue guidelines as a result of their Social Safety profit and outlined profit revenue would put them above the restrict. A number of states have particular revenue guidelines for long-term care with barely increased limits. Even then, 70 p.c of households in our pattern wouldn’t qualify. In actuality, solely 15 p.c of households with greater than $100,000 in preliminary belongings will truly find yourself on Medicaid (see Determine 2), in comparison with the 60 p.c of households who assume that spending all the way down to Medicaid is an choice for them.

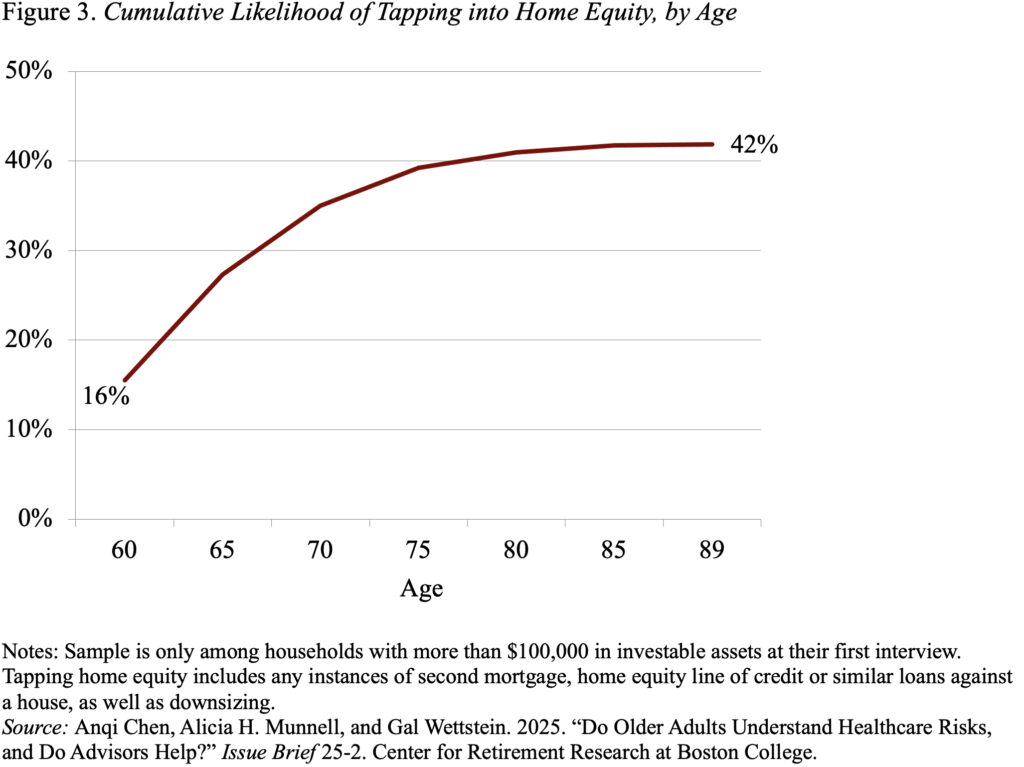

One of many least widespread contingency choices for financing healthcare prices is tapping house fairness. Lower than a 3rd of households stated they’d take into account it. Nonetheless, in actuality, over 40 p.c will faucet house fairness in retirement – both by getting a second mortgage, making use of for a house fairness line of credit score or different loans in opposition to the home, or downsizing and shifting to a much less beneficial home (see Determine 3).

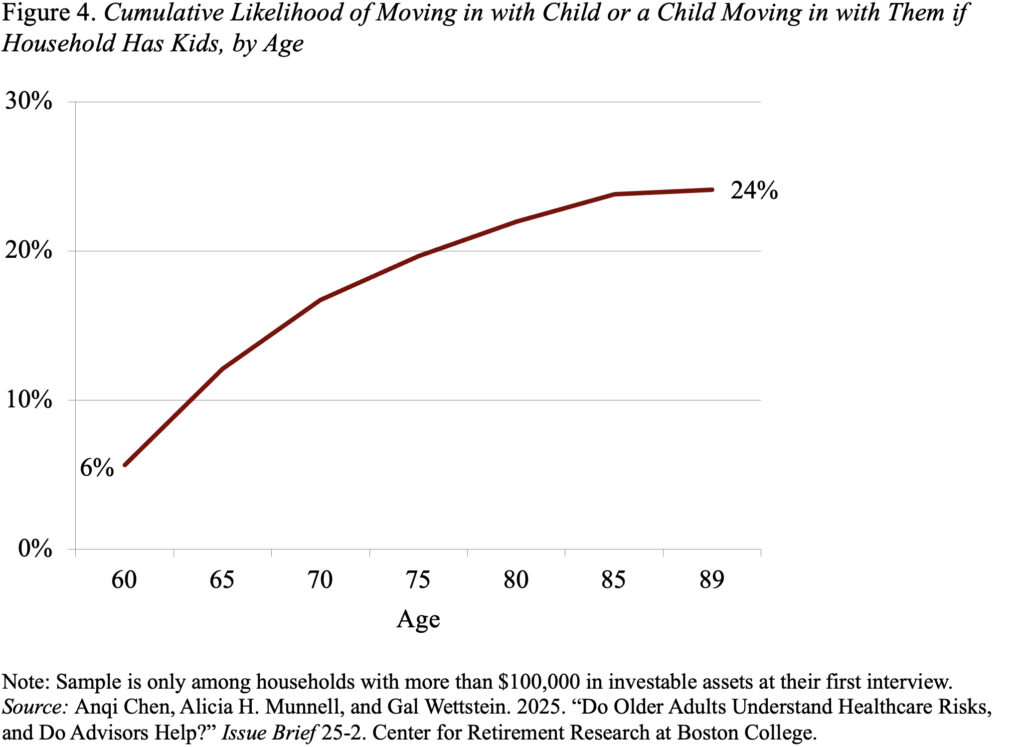

Lastly, one other unpopular choice for managing healthcare wants amongst respondents is shifting in with youngsters. Once more, lower than a 3rd say they’d take into account this selection. Curiously, in the actual world, solely a couple of quarter of older households in our wealth group find yourself residing with their youngsters (see Determine 4). So, this selection does look like the least most well-liked back-up if plans fail.

Briefly, the uninsured parts of healthcare prices in retirement – notably these related to long-term care – may be substantial, and older households wouldn’t have an correct notion of those dangers. Because of this, many will find yourself with insufficient assets. When members in our survey – people having $100,000 or extra in investable belongings – have been requested how they’d cope with such a scenario, about 60 p.c stated they’d spend all the way down to qualify for Medicaid. That’s not an affordable choice for many given this system’s tight revenue and asset necessities. Actually, solely 15 p.c of this group is ever more likely to qualify for Medicaid. Respondents have been much less passionate about tapping their house fairness, however many (over 40 p.c), actually, do faucet house fairness as a supply of help.