{kind=link}

Background: What Drives Monetary Considerations Round Retirement?

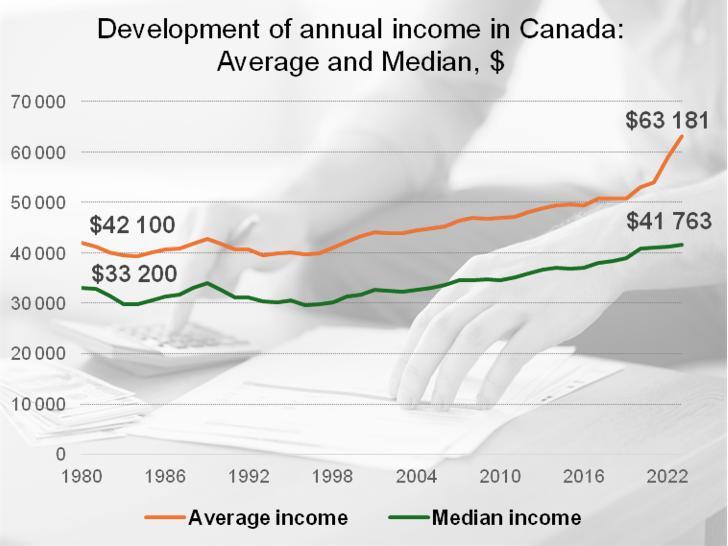

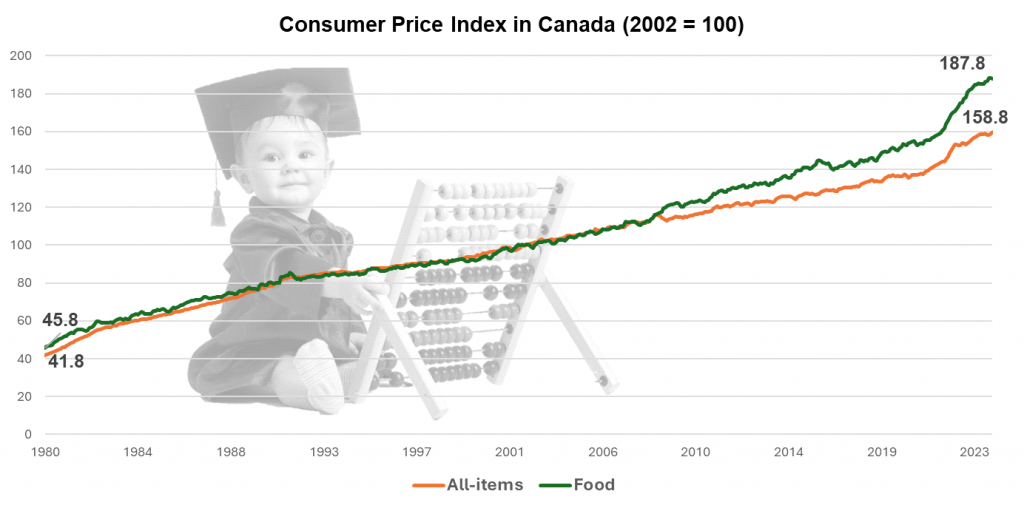

Regardless of hovering prices in Canada, particularly on the actual property aspect, the incomes of Canadians haven’t grown quick sufficient to maintain tempo with the elevated value of residing. Each common and median incomes haven’t climbed as shortly as the buyer value index (CPI).

This implies, the common wage grew solely by 50% and the median wage grew solely by 26% between 1980 and 2022, which ends up in minimal progress year-over-year. Nevertheless, after we have a look at the event of the CPI, it climbed far quicker than salaries; rising nearly 400% between 1980 and 2023.

To place this in perspective, when a loaf of bread at Loblaws prices $3.99, because it averages now at Loblaws in 2024, it will have value a lot within the earlier years:

| 1980 | 1990 | 2000 | 2010 | 2020 | 2024 |

| $1.12 | $1.87 | $2.29 | $2.69 | $3.49 | $3.99 |

It means getting much less for the same sum of money, provided that salaries haven’t elevated on the similar velocity.

If we have a look at actual property costs, this improvement turns into much more drastic, particularly in cities like Toronto and Vancouver. For instance, in 1980 the common value of a Toronto property was $75,694. In 1990 – $255,000, in 2000 – $243,255. In 2010 it was $431,262 and in 2020 it was $939,636. In 2023 prices soared additional to $1,126,591.

On the similar time, life expectancy in Canada elevated from 75.1 years to 82.96 in 2023. This general statistic, although, is watered down by a variety of elements, together with those that have a diminished well being expectancy resulting from well being pre-conditions. What stands out is, at present 5 out of 10 Canadians aged 20 immediately are anticipated to achieve age 90, and 1 out of 10 is predicted to reside to 100 years of age.

It’s no marvel why Canadians are asking themselves if they may have the ability to afford an honest retirement in an setting the place they reside longer than ever, however salaries don’t climb as shortly as client items costs and actual property prices.

How is This Retirement Article Totally different?

There are quite a few articles written on the subject of retirement and the way a lot cash you want. Most of them converge in the direction of a easy “you want 70% of your pre-retirement earnings,” assertion, which is a most popular approach for monetary advisors to plan however it doesn’t take into consideration specifics of specific conditions equivalent to should you hire or personal a home, should you want to gravitate in the direction of a easy or extra luxurious way of life, and many others.

There are a number of themes we are going to cowl on this article. First, we talk about possible situations and for every of them, and we share a ballpark of how a lot cash you want. Subsequent, we are going to speak concerning the cash you want if you wish to retire at a specific age or at a specific wage. Lastly, we dive into insurance coverage merchandise equivalent to entire life insurance coverage, common life insurance coverage, time period life insurance coverage, important sickness insurance coverage that may enable you to plan your retirement higher.

Our Strategy

|

So, let’s begin by stepping away from the usual 70% method and as a substitute develop an approximate schedule of funds which you could anticipate to pay throughout completely different classes equivalent to home, transportation, meals, hobbies, and holidays. For our train, we use the instance of anyone who’s about to retire on the age of 64. Common life expectancy in Canada is at present 84 years however that may be a harmful quantity to plan for as this variability is pretty excessive; you don’t wish to run out of cash by that age. We use 94 as our higher reference quantity, that means that should you retire at 64, you ought to be ready to financially cowl 30 years of your life on the model you’re contemplating. We added extra situations primarily based on two main elements:

|

Professional intro: Paul Foster Paul Foster is the Director of Investments, Japanese Canada, at Hub Monetary. He’s a extremely revered thought chief and knowledgeable within the monetary companies trade, with over 25 years of expertise in monetary companies, investments, and insurance coverage. Previous to becoming a member of Hub Monetary, he held quite a few gross sales roles at Canada Life / Nice-West Life. He additionally spent a major period of time as a monetary advisor with Manulife Securities and BMO Nesbitt Burns. Paul accomplished his BA in Political Science on the College of Windsor. |

So, let’s begin by stepping away from the usual 70% method and as a substitute develop an approximate schedule of funds which you could anticipate to pay throughout completely different classes equivalent to home, transportation, meals, hobbies, and holidays.

For our train, we use the instance of anyone who’s about to retire on the age of 64. Common life expectancy in Canada is at present 84 years however that may be a harmful quantity to plan for as this variability is pretty excessive; you don’t wish to run out of cash by that age. We use 94 as our higher reference quantity, that means that should you retire at 64, you ought to be ready to financially cowl 30 years of your life on the model you’re contemplating.

We added extra situations primarily based on two main elements:

- Having a mortgage versus a home that’s paid off, as it is a massive value driver.

- The kind of retirement you’re gravitating in the direction of – customary versus luxurious. Inside luxurious retirement we thought of a number of holidays all year long, having a dearer automobile, and spending extra on groceries.

Professional intro: Paul Foster

Paul Foster is the Director of Investments, Japanese Canada, at Hub Monetary.

He’s a extremely revered thought chief and knowledgeable within the monetary companies trade, with over 25 years of expertise in monetary companies, investments, and insurance coverage.

Previous to becoming a member of Hub Monetary, he held quite a few gross sales roles at Canada Life / Nice-West Life. He additionally spent a major period of time as a monetary advisor with Manulife Securities and BMO Nesbitt Burns.

Paul accomplished his BA in Political Science on the College of Windsor.

Every situation was calculated each WITH and WITHOUT authorities advantages equivalent to Canada Pension Plan (CPP) or Previous Age Safety (OAS) funds. These advantages have been estimated utilizing the Canadian Retirement Earnings Calculator from the Authorities of Canada.

- This calculation doesn’t embody any jobs or aspect hustles you may be pursuing to reinforce your money stream after retirement.

- We don’t contemplate any financial savings that you simply might need collected (e.g. RRSP, TFSAs, and many others.). If in case you have saved $1M all through your pre-retirement years, you want $1M much less as soon as you’re retired.

- We don’t contemplate extra investments as you would want to think about each the extra earnings stream from these investments and in addition the taxes related to them.

- If in case you have an extra stream of earnings via a pension/annuity, that may additionally change the equation in your favour.

- We do account for inflation utilizing 2.5% as an annual inflation marker.

- We don’t contemplate any extra worth that is likely to be locked in your property that you may entry in numerous methods, e.g. HELOC, reverse mortgage, or downsizing or promoting your property.

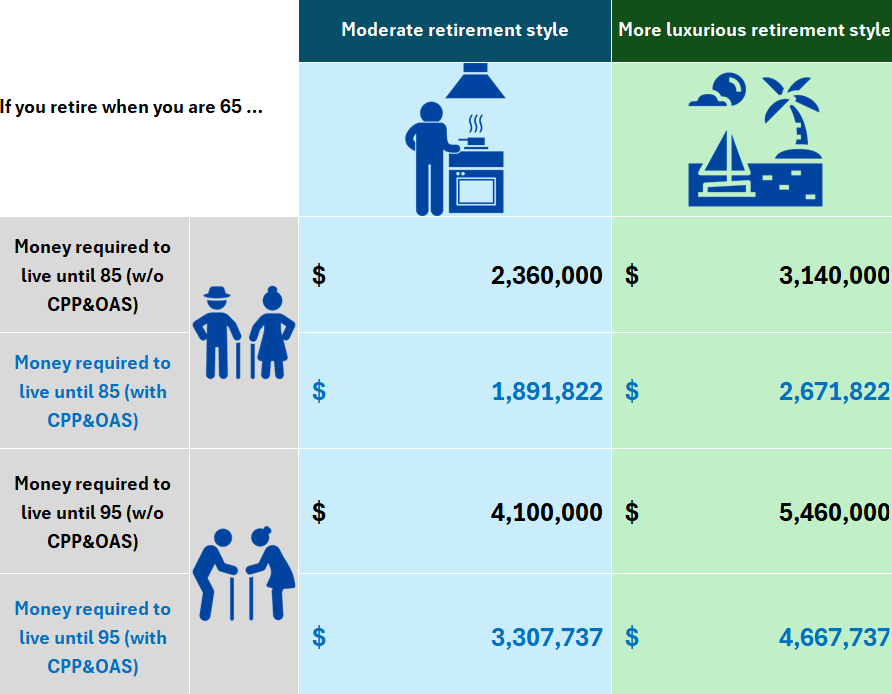

State of affairs 1: Single Individual Family

First, we have a look at the situation of retirement financial savings for a single individual each with and with out a mortgage. For that, we consult with a median mortgage ($469,000) and assume a time period of 20 years.

The vary that’s offered refers to retirement funds required for residing till the ages of 84 and 94.

Along with that, we differentiate between reasonable and splendid retirement residing the place we double bills in some classes (highlighted in pink within the desk under).

| Price classes | |

| Dwelling | • Mortgage • Home upkeep & different charges (e.g. rubbish) • House insurance coverage • Property taxes |

| Utilities | • Cable • Web • Hydro • Fuel/Heating |

| Transportation | • Fuel • Insurance coverage • Automotive upkeep • Automotive change (each 15 years) |

| Meals | • Groceries |

| Healthcare | • Fundamental healthcare bills |

| Attire | • Clothes • Sneakers |

| Leisure |

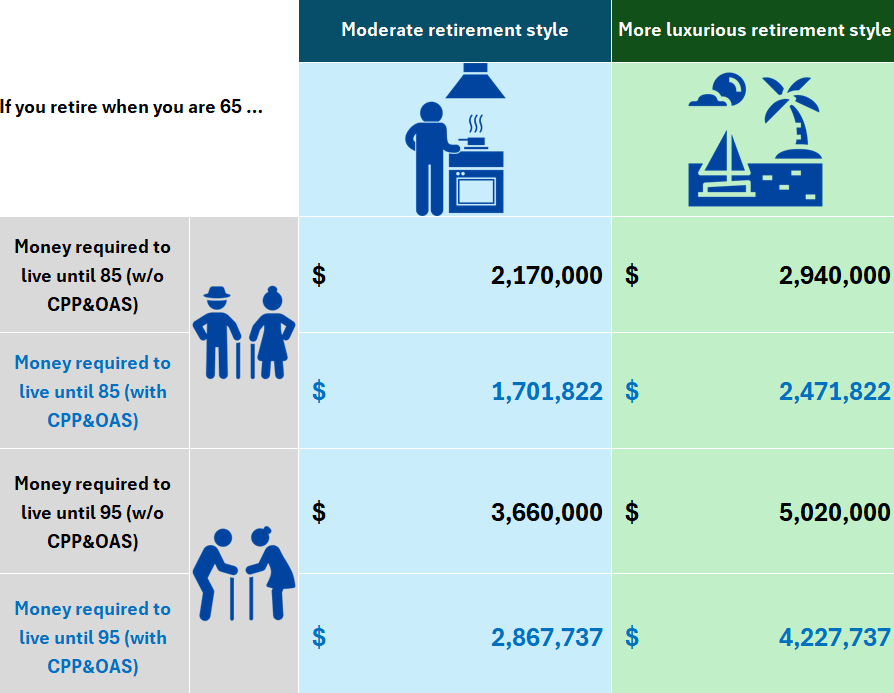

Single Individual Family And not using a Mortgage

In the event you should not have a mortgage to pay if you retire, that units you up for much decrease retirement prices. The primary dwelling-related prices that you may be liable for are:

- property taxes

- upkeep prices

- extra charges (like rubbish charges)

- residence insurance coverage

On this case, your estimated retirement finances may look as follows:

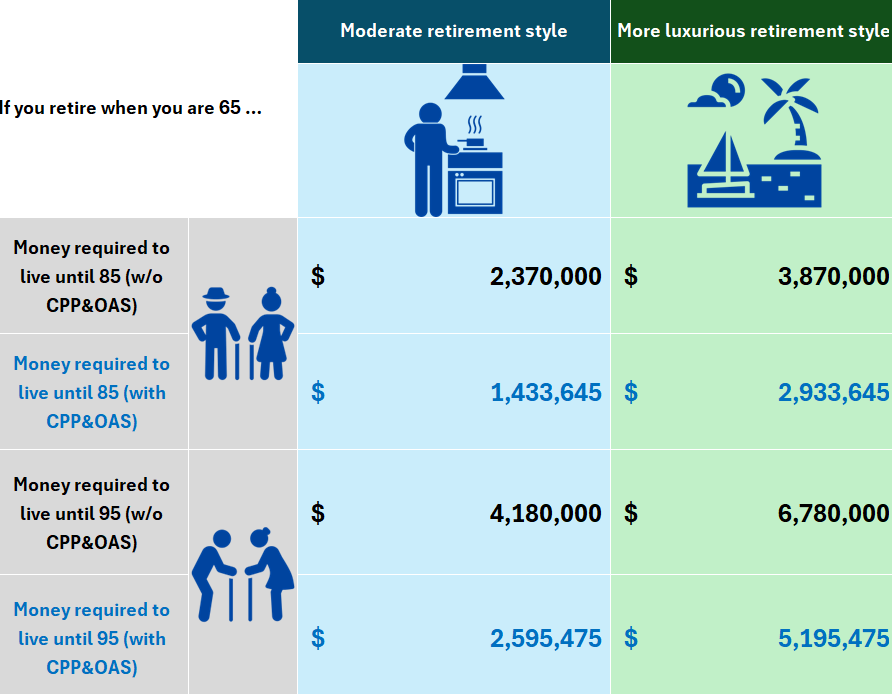

Single Individual Family with a Mortgage

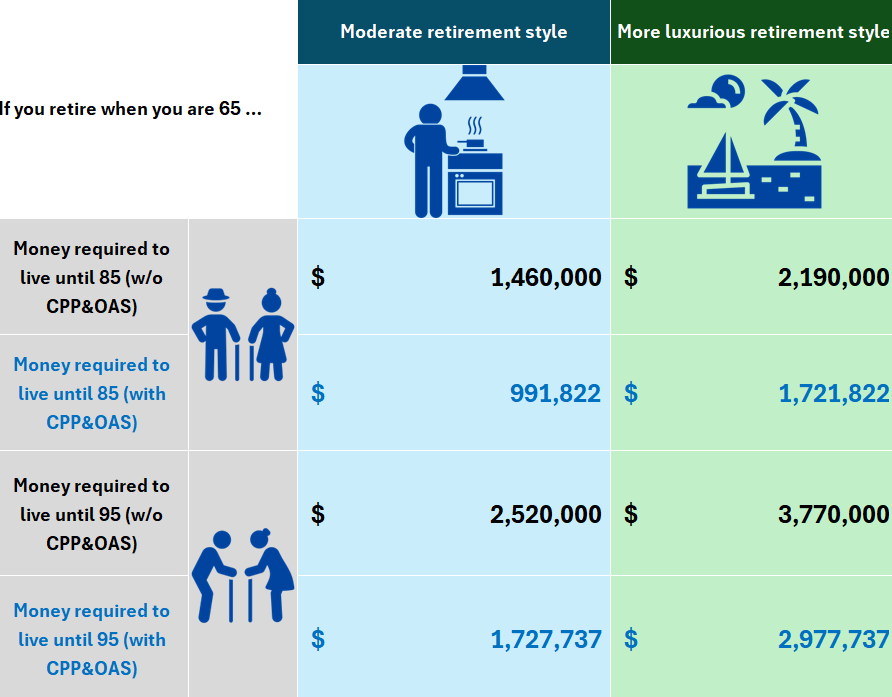

Ought to you’ve got a substantial mortgage if you end up retiring, you have to carry extra prices. On this case, you’re including a median of $2,500/month to your retirement finances. Your estimated retirement finances may look as follows: between $2.2M and $2.9M for reasonable and splendid retirement kinds if you plan till the age of 85, and between $3.7M and $5.0M for reasonable and splendid retirement kinds if you plan till the age of 95.

It is sensible to say that the monetary wants of anyone who’s planning to remain a renter are considerably related as this individual is not going to be paying off a mortgage however will spend a substantial sum of money in rental prices. Rental prices of ~$4,000/month will lead to numbers just like those above.

An individual with {a partially} paid mortgage might need extra sources of money equivalent to unlocking worth in an already paid-off portion of the property (HELOC, reverse mortgage, full property sale, and many others.).

State of affairs 2: Two-person Family

On this situation, we have a look at retirement funds required for a family of two folks round retirement age. We assume that at this stage there aren’t any child-related bills as the youngsters have already grown up and are fully impartial.

We keep on with the identical mortgage, understanding that these prices are unfold throughout two folks.

On the similar time, some prices like attire, holidays, and many others., are doubled (as famous within the desk under in pink) whereas others like meals are elevated by 75% (see the desk under in blue), realizing that there are some financial savings when residing collectively.

Please observe that that is solely an approximation.

| Price classes | |

| Dwelling | • Mortgage • Home upkeep & different charges (e.g. rubbish) • House insurance coverage • Property taxes |

| Utilities | • Cable • Web • Hydro • Fuel/Heating |

| Transportation | • Automotive upkeep • Automotive change (each 15 years) • Fuel • Automotive Insurance coverage |

| Meals | • Groceries |

| Healthcare | • Fundamental healthcare bills |

| Attire | • Clothes • Sneakers |

| Leisure | • Hobbies • Holidays • Going out |

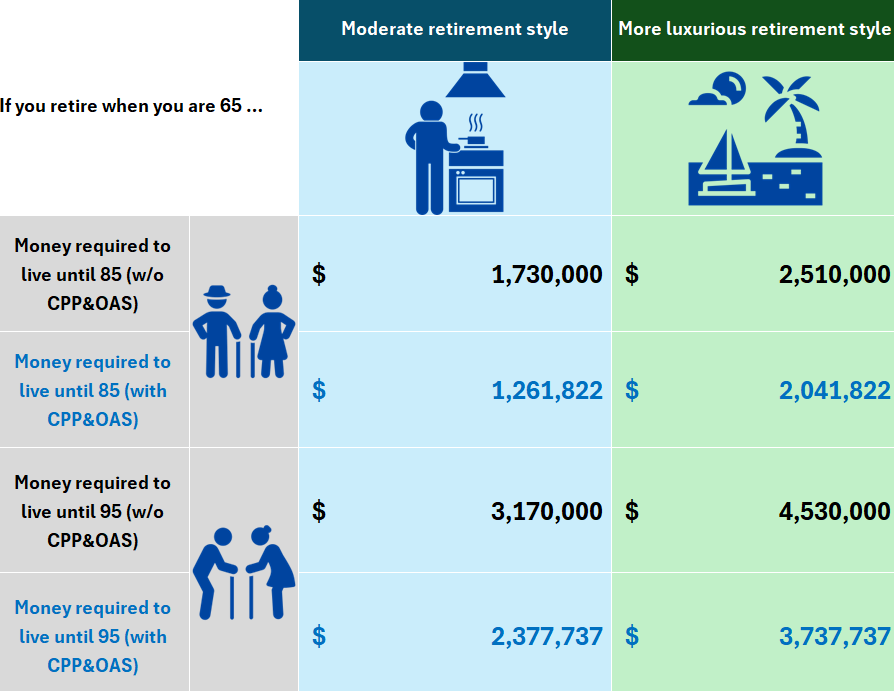

Two-person Family And not using a Mortgage

In case your family doesn’t have a mortgage to pay, that units you up for much decrease retirement prices. The primary dwelling-related prices that you may be on the hook for are property taxes, upkeep prices, extra charges (like rubbish charges), and residential insurance coverage.

On this case, your estimated retirement finances may look as follows:

The numbers above are per family, that means that if each companions or spouses are contributing to the family, every of them may contribute from $1.2M (cash required to reside in a reasonable vogue till the age of 85) to $3.4M (cash required to reside in an expensive vogue till the age of 95).

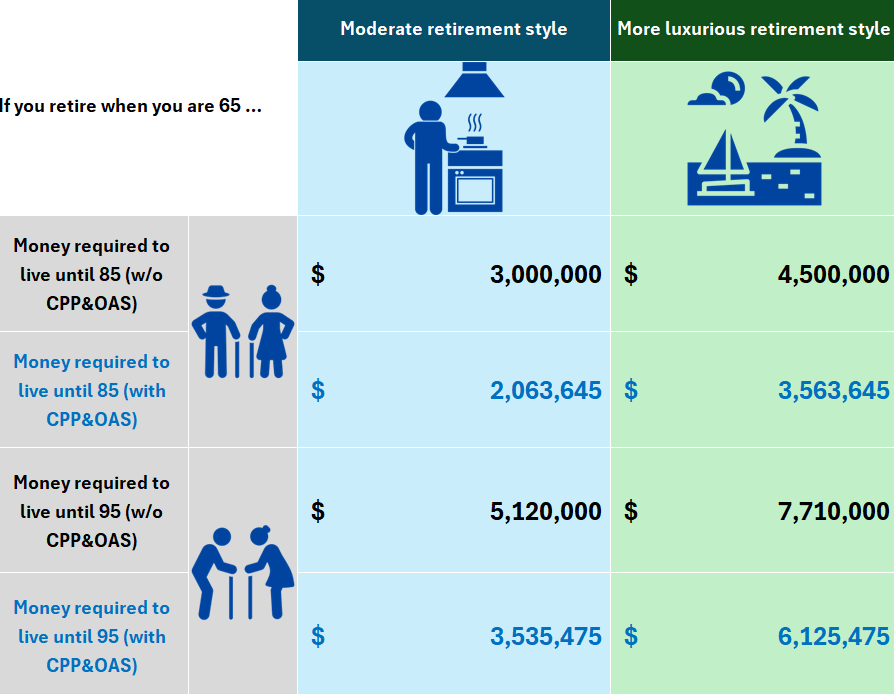

Two-person Family with a Mortgage

In the event you nonetheless have quite a bit to repay in your mortgage if you end up retiring, you have to carry extra prices. On this case, you’re including on a median of $2,500/month to your retirement finances.

Your estimated retirement finances shall be between $3.0M and $4.5M for reasonable and splendid retirement kinds to achieve age 85 in consolation, and between $5.1M and $7.7M for reasonable and splendid retirement kinds if you plan to reside till the age of 95.

State of affairs 3: Single Individual Family with a Critical Medical Situation

As folks become old, their well being tends to deteriorate. It comes as no shock that there is likely to be extra prices related to sustaining a great way of life for individuals who expertise critical medical situations.

The important thing distinction on this situation as in comparison with the primary one (a single individual) is the medical situation of a retiree that requires him/her to spend extra funds on health-related care.

We account for this by including extra homecare bills, principally anyone who helps with on a regular basis duties like a nurse or a private help employee. That provides round $4,000/month to the finances.

For our train, we contemplate that the total quantity is paid out of pocket (personal care possibility), with none authorities help. Observe that the federal government could provide some extra monetary help relying in your case.

Single Individual Family with a Critical Medical Situation and And not using a Mortgage

No mortgage additionally means decrease prices for seniors with medical situations, if they’ll keep in their very own dwelling. The primary dwelling-related prices that you may be on a hook for are property taxes, upkeep prices, normal charges (HOA, rubbish, utilities), and residential insurance coverage.

A typical finances on this situation can appear like this:

Single Individual Family with a Critical Medical Situation with a Mortgage

Ought to you’ve got a substantial mortgage if you end up retiring, you have to carry extra prices. On this case, you’re including a median of $2,500/month to your retirement finances on prime of all of your different bills.

Your estimated retirement finances might be between $2.4M and $3.1M for reasonable and splendid retirement kinds respectively if you plan till the age of 85 and between $4.1M and $5.5M for reasonable and splendid retirement kinds respectively should you reside to the age of 95.

How A lot Cash Do I Have to Retire at a Specific Age?

To reply this query, let’s contemplate a simplified method contemplating that if you wish to preserve your present way of life you have to plan for 70% of your pre-retirement wage for annually of your life. Must you spend your retirement in a extra luxurious approach, dedicating your self to hobbies you’ve got at all times dreamed of plus permitting your self a number of trip journeys a yr, you’d higher plan to your full pre-retirement earnings (100%) for annually of your life in retirement. The concept is that an extra 30% of bills may be saved from not having work bills (much less wanted for transportation, clothes, and many others.). These funds may be diverted to hobbies, extra holidays, and different objects of curiosity.

Since salaries range enormously; we take a number of choose knowledge factors from 2023:

- Median Canadian Wage: $41,763

- Common Canadian Wage: $63,181

Along with that, we additionally have a look at the numbers when a wage is round $80,000 and $120,000 per yr.

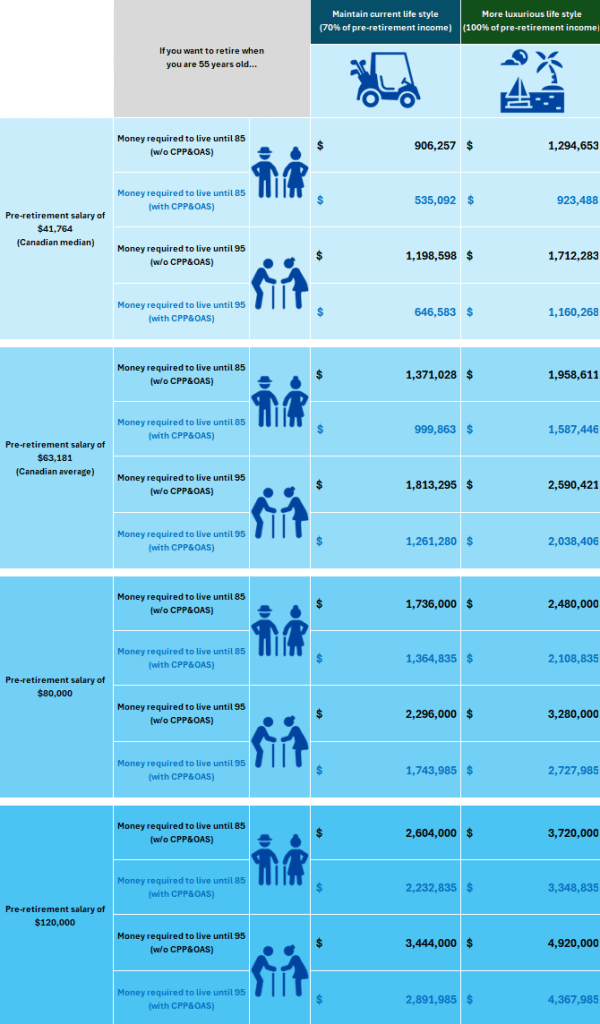

How A lot Cash Do I Have to Retire at Age 55?

To retire on the age of 55 whereas having a wage simply shy of $42,000 (once more contemplating the Canadian median earnings of $41,763), you would want roughly $0.9M to comfortably attain the age of 85 and $1.3M to achieve 95. Nevertheless, to retire on full pre-retirement earnings, you want roughly $1.2M to achieve 85 and $1.7M to achieve 95. Observe that in case your pre-retirement earnings is larger, it’s best to plan for larger retirement funds, based on the desk under.

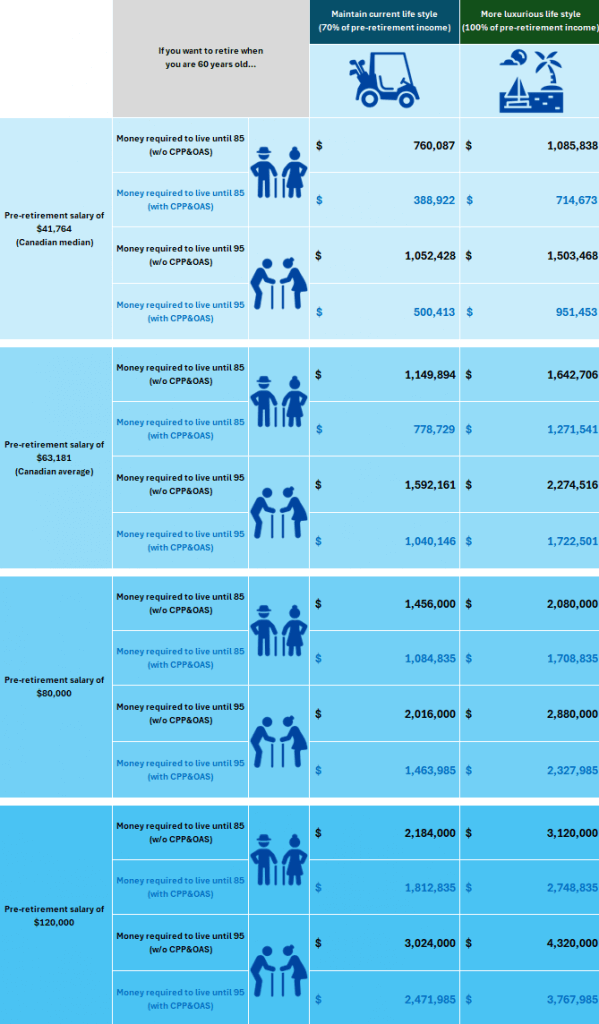

How A lot Cash Do I Have to Retire at Age 60?

At age 60, whereas having a wage simply shy of the median at $42,000, you would want roughly $0.8M to retire at 85 and $1.1M to retire at 95.

In the event you plan to depend on your full pre-retirement earnings, plan for roughly $1.1M for age 85 and $1.5M for age 95.

Ought to your pre-retirement earnings be larger, let’s say $120,000, you would want considerably larger pre-retirement funds. In the event you determine to keep up your present way of life (whereas planning for 70% of your pre-retirement earnings), you’d want $2.2M and $3.0M to reside till 85 and 95 accordingly, or $3.1M and $4.3M to reside till 85 and 95 accordingly.

In case your pre-retirement earnings is larger, then it’s best to plan for larger retirement funds, based on the desk under.

How A lot Cash Do You Have to Retire with a Specific Annual Earnings?

Let’s have a look at a simplified method contemplating sustaining your present way of life. Right here, you have to plan for 70% of your pre-retirement wage for annually of your life. Must you spend your retirement residing in luxurious, plan to your full pre-retirement earnings for annually of your life in retirement.

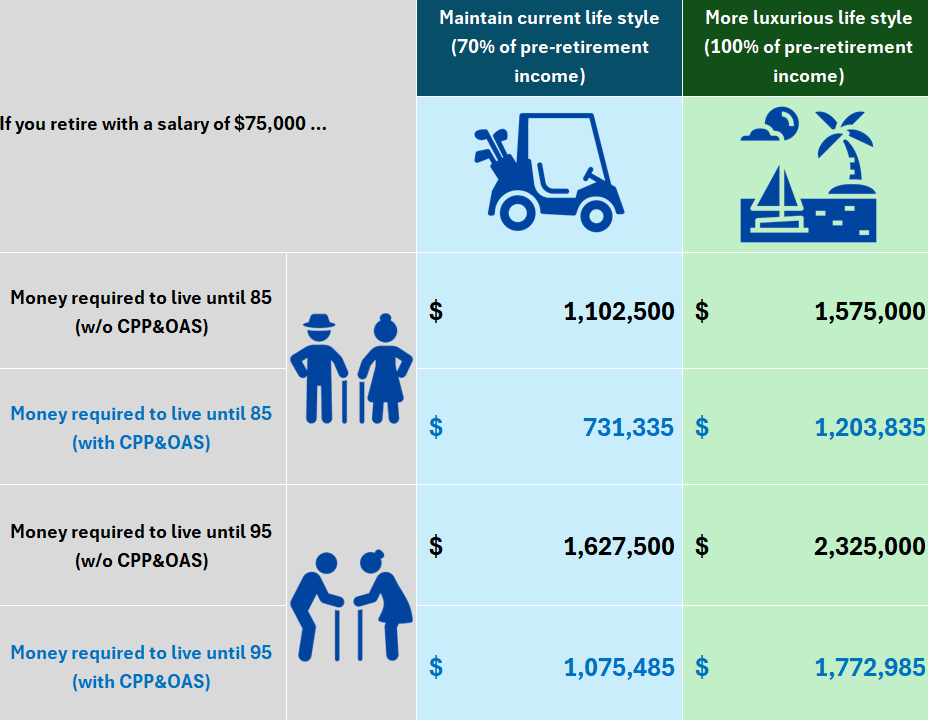

How A lot Cash Do You Have to Retire With $75,000 a 12 months Earnings?

To retire at 65 whereas having a wage of $75,000, you want roughly $1.1M should you reside till the age of 85 and $1.6M should you reside till the age of 95. For a full pre-retirement earnings, you would want roughly $1.6M to comfortably get to 85 and $2.3M to make it to 95 whereas sustaining your present way of life.

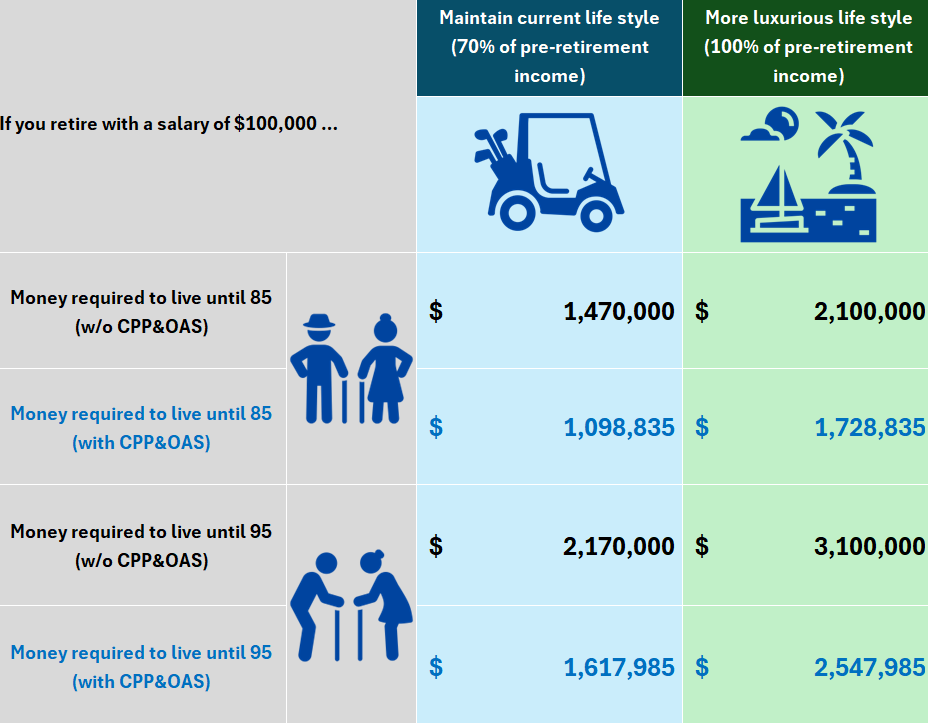

How A lot Cash Do You Have to Retire With $100,000 a 12 months Earnings?

To retire at 65 whereas having a wage of $100,000, you want roughly $1.5M should you plan to reside till the age of 85 and $2.1M should you plan to reside till the age of 95. Must you determine to reside retirement in luxurious and depend on a full pre-retirement earnings, you want roughly $2.2M to achieve the age of 85 and $3.1M to achieve 95 in consolation.

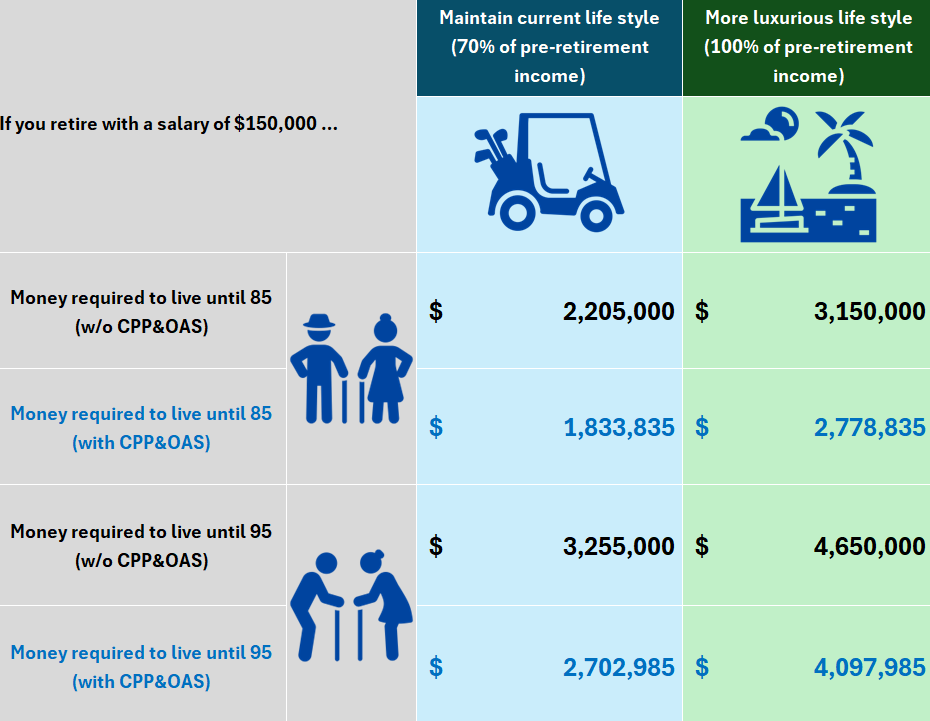

How A lot Cash Do You Have to Retire With $150,000 a 12 months Earnings?

To retire at 65 whereas having a wage of $150,000, plan for $2.2M for age 85 and $3.2M for age 95. To depend on your full pre-retirement earnings, you want roughly $3.3M to achieve age 85 comfortably and $4.7M to achieve 95.

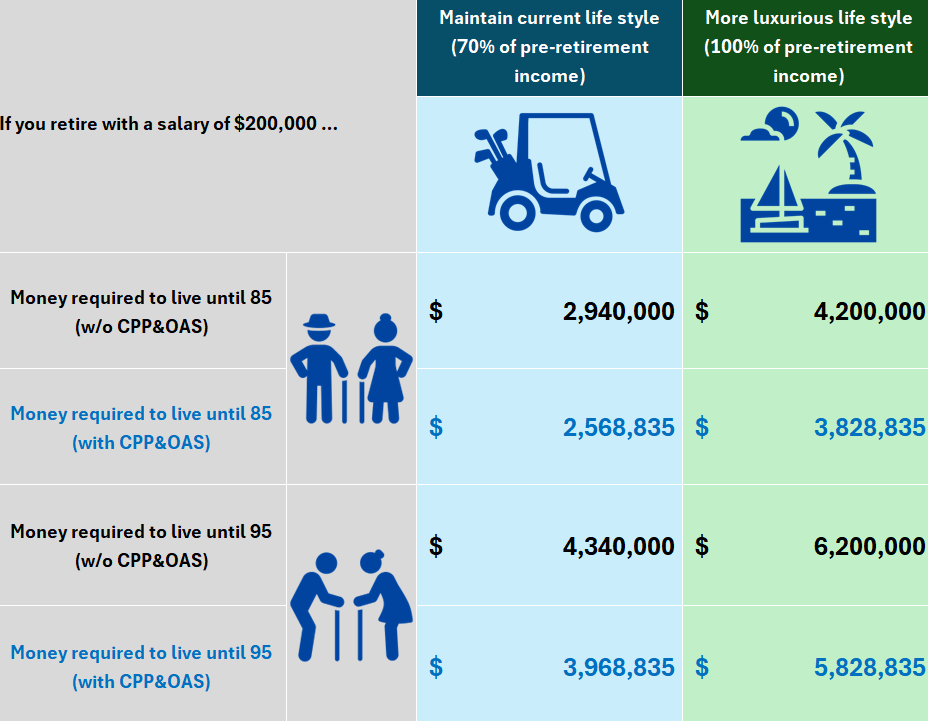

How A lot Cash Do You Have to Retire With $200,000 A 12 months Earnings?

To retire at 65 on a wage of $200,000, intention for round $2.9M for age 85 and $4.2M for age 95. In the event you want your full pre-retirement earnings you want roughly $4.3M should you plan to reside till the age of 85 and $6.2M should you plan to reside till the age of 95.

What Monetary and Insurance coverage Merchandise Can Assist with Retirement Planning?

Each funding and insurance coverage merchandise play a job when planning for sufficient monetary protection for retirement.

| Typical Monetary / Funding merchandise taking part in a job within the retirement | Typical Insurance coverage merchandise taking part in a job within the retirement |

| • Mutual funds • ETFs • RRSPs • TSFAs • Segregated funds |

• Low prices time period insurance coverage for varied functions e.g. closing bills, mortgage protection, and many others. • Complete life Insurance coverage common life Insurance coverage • Vital Sickness Insurance coverage |

Folks want to speculate based on their age and supreme wants. These with longer time horizons can and may tackle extra danger to make sure reaching their targets. They need to additionally benefit from making scheduled periodic deposits to their investments to benefit from volatility available in the market.

Mutual funds are an effective way to benefit from skilled administration and ETFs can present an answer for these which can be in search of decrease prices.

Additionally, typical monetary merchandise like RRSPs and TFSAs have their position in saving/augmenting your funds whereas leveraging tax alternatives.

As shoppers become old and wish to shield their investments, they’ll look to segregated funds, which have ensures inbuilt together with different advantages like bypassing probate by with the ability to title a beneficiary on non-registered holdings.

It’s advisable to work with a monetary advisor who understands your present scenario, long-term plans, and has your greatest curiosity at coronary heart.

On the insurance coverage aspect, it is very important have a look at each want and money stream.

Some in style options with youthful households are lower-cost time period insurance coverage options to cowl bills (closing bills, mortgage, training, and many others.) and earnings substitute in case of the loss of life of 1 companion.

These a bit of older can be everlasting insurance coverage like entire life insurance coverage or common life insurance coverage to make sure family members are taken care of as the prospect of sickness is bigger. Lastly, you may have a look at important sickness insurance coverage and incapacity insurance coverage. Vital sickness is rising in popularity as a result of the prospect of falling sick with some type of life altering sickness is bigger than ever, particularly as we live longer.

Some extra superior insurance coverage methods, like infinite banking, leverage everlasting insurance coverage insurance policies like one’s personal mini financial institution which you could borrow in opposition to as a substitute of paying larger lending charges to monetary establishments.

Our advisors are very nicely versed in all insurance coverage merchandise to help you with monetary and retirement planning. LSM Insurance coverage (a division of Hub Monetary) works with extra insurance coverage corporations than most brokerages. We anticipate finding out extra about your scenario and serving to you propose to your retirement.