{kind=link}

When did you notice your credit score rating was essential to virtually every part you probably did as an grownup?

For me, it was after I discovered how the bank card choices for folks with nice credit score have been considerably higher than for individuals who had common or beneath credit score scores. If in case you have good to nice credit score, you get entry to bank cards with large sign-up bonuses and rewards.

Should you don’t, your choices are much less engaging and you need to work in the direction of enhancing your rating earlier than you can begin making use of for nice bank cards.

However bank cards are only one small half — should you don’t have good credit score, it may be troublesome to get a rental condominium, a cellphone, and plenty of different seemingly unrelated requirements.

So right now, we’re going to speak about credit score scores and the best way to enhance yours.

To begin, there is just one credit score rating that issues, and that’s the FICO Credit score Rating of Fair Isaac Corporation.

Desk of Contents

- What’s a credit score rating in 30 seconds…

- How you can Enhance Your Credit score Rating

- Establishing Credit score

- Doing No Hurt!

- How you can Enhance Your Rating

- Let’s Hold It Excessive

- Credit score Constructing Instruments

- Experian Enhance

- Secured Credit score Playing cards

- Credit score Constructing Playing cards

- Credit score Builder Loans

- What About Credit score Restore?

On this information, I present you each step you possibly can take to legitimately enhance your credit score rating so you possibly can, on the very least, be higher than the common.

What’s a credit score rating in 30 seconds…

Your credit score rating is a quantity between 300 and 850, greater is healthier. It’s a measure of how probably you might be to default (fail to pay) on a mortgage, the decrease the quantity the higher the danger.

- Wonderful credit score is 781+

- Good is 661-780

- Honest is 601-660

- Poor is 501-600

- Dangerous is something beneath 500

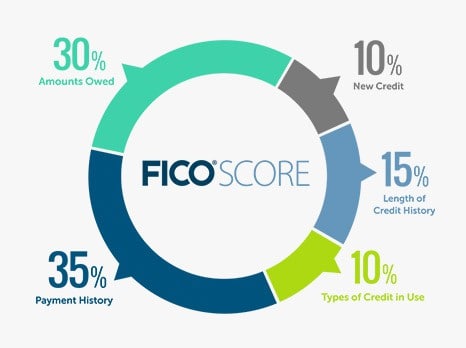

Your credit score rating is made up of 5 elements (picture from FICO):

You’ll be able to overview your credit score rating at no cost with instruments like Credit score Sesame.

That’s it!

How you can Enhance Your Credit score Rating

The important thing to growing your credit score rating is to enhance these 5 elements from the picture above.

This information is damaged up into three sections:

- Establishing Credit score

- Doing No Hurt

- How you can Enhance Your Rating

- And Holding it Excessive

Establishing Credit score

It’s attainable, particularly early on, that you just may not have a credit score rating in any respect or the dreaded “not sufficient credit score historical past.” It’s arduous to get a mortgage whenever you’ve by no means had a mortgage earlier than. However there are some things you are able to do to determine a credit score historical past.

If used responsibly, these choices will begin reporting constructive info to your credit score report. This may set up some credit score historical past and show to future lenders that you just do repay your loans.

One word: Solely grow to be a licensed consumer on somebody’s bank card if they pay their payments on time. In the event that they pay late, that may go in your credit score report as nicely. You may get that eliminated, however it’s a problem that may be prevented should you choose somebody reliable.

To study extra about establishing credit score, overview our information to How you can Set up Credit score.

Doing No Hurt!

Be further diligent and keep away from the next in any respect prices.

They are going to cut back your credit score rating excess of any options we make about enhancing it.

- Don’t miss funds or pay late (Cost Historical past) – That is a very powerful mistake to keep away from, because it accounts for over a 3rd of your rating. Should you miss a cost or flip it in late, you’ll sink your rating.

- Opening new traces of credit score (New Credit score): In case you are attempting to extend your rating, don’t apply for something that might probably end in a suggestion of credit score, resembling a bank card. Additionally, credit score inquiries may even decrease your credit score rating by just a few factors for some time. So, it’s higher to not apply for brand new credit score proper now.

- Closing any open traces of credit score (Quantities Owed, Size of Credit score Historical past) – Whenever you shut a line of credit score, say a bank card, it impacts two elements. By decreasing your complete accessible credit score, you’ll enhance your credit score utilization (unhealthy). You additionally shorten the size of your reported credit score historical past, which might be unhealthy should you shut one in all your older bank cards.

- Don’t repay that charge-off (Cost Historical past) – If a lender “charged off” a mortgage, which implies they’ve given up on it, it should damage your credit score rating for seven years. If it’s already occurred, the harm is finished and is slowly subsiding. Should you pay it off, it’ll reset the clock until you’ve negotiated (get it in writing!) with the lender to have them take away it.

How you can Enhance Your Rating

Sufficient doom and gloom, what are you able to do to extend your rating?

- Pay down money owed – The decrease your credit score utilization, the higher. An individual who makes use of simply 5% of their complete credit score is a safer guess than somebody who’s utilizing 50%. Fairly apparent the quickest manner to try this is to pay down some present debt.

- Enhance your credit score limits – Along with paying down debt, growing your credit score limits will assist along with your credit score utilization. For instance, when you have a $5,000 credit score restrict and a $2,000 stability, your credit score utilization is 40%. Nevertheless, should you enhance your credit score restrict to $6,000, your credit score utilization is now 33%. Right here’s the best way to ask a bank card the best way to enhance your restrict.

- Dispute errors – Your finest shot at enhancing your rating is to seek out errors and repair them. Test your credit score studies and undergo them very fastidiously for any damaging marks. Do you see any accounts that aren’t yours? Dispute them. Each credit score bureau has a course of for disputing errors, and these can take a very long time however supply the perfect bang to your buck (that’s why you need to be monitoring your studies on a regular basis, not simply whenever you want good credit score). For extra on this, Credit score Karma has a information on disputing errors.

- Repair omissions – Credit score bureaus aren’t good (shocker!) so test that they’ve all of the accounts you might be liable for. Chances are you’ll discover they’re lacking ones that might enhance your Cost Historical past, Size of Credit score Historical past, Quantities Owed, and even Sorts of Credit score In Use.

- Ask for Forgiveness – If in case you have a late cost, ask the lender for a “goodwill adjustment.” This works finest when you have an ideal relationship with the lender since you’re asking them to take away the mark out of your credit score report. Click on right here for a template however be sure you edit it to construct a stronger customized case.

- Negotiate Removing – Should you don’t have an ideal relationship (like should you’re behind on funds), you possibly can attempt to negotiate a take care of a lender that entails eradicating these marks in return for an installment cost plan or lump sum cost.

- Attempt to take away charged-off accounts – If in case you have this in your report, attempt to get it eliminated. Right here’s recommendation on how to try this.

- Dispute late funds, collections, and so on. – Some consultants don’t advocate that you just dispute reliable late funds or different damaging marks. I’m telling you that it is a technique loads of folks use with nice success. Let your individual ethical compass information you. This technique works as a result of typically the creditor can’t confirm the small print, and the mark shall be eliminated.

✨ Associated: What Will Occur to Your Credit score Rating if You Do Not Handle Your Debt Properly

Let’s Hold It Excessive

From right here, it’s easy – maintain making these funds and keep watch over your credit score studies.

How do you be sure you by no means miss a cost?

Two steps:

- Use not more than two playing cards. You don’t want 5 bank cards; you want at most two playing cards. The extra playing cards you’ve gotten, the extra statements you get and the extra funds you need to make. It’s sucking up your time and may result in errors; get it down to simply two playing cards.

- Arrange computerized funds. I be certain I get an electronic mail notification just a few days earlier than each computerized cost, so I can overview the assertion for errors and make sure my checking account has enough funds.

How do I keep watch over your credit score studies?

The regulation states you can get entry to your credit score studies each single yr. I overview every credit score report on a rotating schedule, one each 4 months. Equifax within the Spring, Experian within the Summer season, and Transunion within the Fall – all by way of AnnualCreditReport.com – the one place to go to your credit score report.

Monitor “rating” with free providers

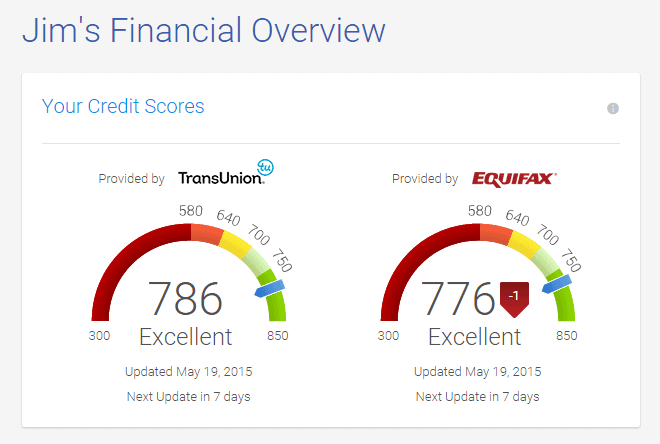

On a extra common foundation I log into providers at Credit score Sesame, Credit score Karma, and Quizzle that monitor my scores at no cost. They don’t present FICO credit score scores however they do supply the proprietary scores from the credit score bureaus, which is sweet sufficient to behave as a “canary within the coal mine” sort of alert to modifications.

For instance, after I log into Credit score Karma I see a VantageScore 3.0 from TransUnion and from Equifax.

If I see any massive numerical strikes, I do know I must overview that credit score report. A small dip, like 1 level on Equifax, isn’t value investigating.

The next instruments can be found for these with poor or no credit score. The important thing to getting a mortgage when you’ve gotten poor credit score is to cut back the danger to the lender as a lot as attainable.

For instance, secured bank cards require you to place down a deposit, then your credit score restrict is the quantity of your deposit. This protects the lender as a result of should you don’t pay again the mortgage, they will use your safety deposit to recoup the funds. Since there is no such thing as a danger of the lender dropping cash, they’re prepared to take an opportunity on you and provide the alternative to construct a constructive credit score historical past.

Experian Enhance

Experian Enhance isn’t a mortgage, it’s a free service provided by Experian that may enhance your rating by reporting on time funds you make to your payments. So should you pay issues like hire, utilities, and insurance coverage, your on-time funds might be reported to Experian.

This permits for a constructive credit score historical past with out taking out a mortgage. You simply pay your payments like regular.

Right here’s our full Experian Enhance overview to study extra.

Secured Credit score Playing cards

Secured bank cards work identical to common bank cards, besides you need to put down a deposit. How a lot you set down will decide your credit score restrict. So should you submit a $500 deposit, you’ll have a $500 credit score restrict.

When you obtain the cardboard, nevertheless, it really works identical to another bank card. You make purchases, and every month, you may be required to make at the very least the minimal cost by the due date. Your cost historical past shall be reported to the credit score bureaus.

Some secured playing cards mechanically improve to an unsecured card after a time frame, often round six months — assuming accountable use.

Credit score Constructing Playing cards

A few of the newer fintech corporations are providing what they’re calling “credit score constructing playing cards.” These are bank cards that work equally to secured playing cards, however you don’t must put down a deposit. As a substitute, the playing cards are tied to your checking account, and whenever you spend cash on the cardboard, the cash is immediately withdrawn out of your checking account and put aside. The cash that’s put aside is then used to pay the cardboard in full on the due date.

The on-time cost is then reported to the credit score bureaus, and also you construct a constructive credit score historical past.

One instance of that is the Chime Credit score Builder Card.

Credit score Builder Loans

Credit score builder loans are a little bit of a misnomer as a result of they don’t actually work like loans. As a substitute, it’s extra of a pressured financial savings plan that additionally builds credit score.

With conventional loans, whenever you take out a mortgage, you immediately obtain the proceeds after which repay the debt over time. A credit score builder mortgage works in reverse. You make funds right into a financial savings account with the lender, and when your mortgage is full, you’ll obtain the stability of the account.

Let’s have a look at a simplified instance. Say you’re taking a $1,000 credit score builder mortgage with $100 funds for 10 months. Every month, you’ll pay $100, and after 10 months, you’ll have $1,000 in a financial savings account that shall be launched to you.

Observe that in an actual mortgage, there are charges concerned, so you wouldn’t get the total $1,000. Nevertheless, you’ll have 10 months of on-time funds reported to credit score bureaus and a superb quantity of financial savings constructed up, so the price could also be value it.

An instance of this sort of mortgage is the Self Credit score Builder Mortgage.

What About Credit score Restore?

In case your rating is low due to beforehand made errors with credit score, credit score restore generally is a viable choice to attempt to enhance it. Each time there are unhealthy marks in your report, these marks keep on for a time frame and maintain your rating low. These are occasions like a late cost or chapter.

What credit score restore corporations do is take some motion to attempt to take away these black marks. They are going to do issues like dispute damaging objects or take different steps to get them eliminated. They’re going to be costly however when you have a necessity, they are often value it if they’re profitable. They’re solely growing your rating by eradicating the damaging objects.

Alternatively, it’s also possible to use credit score restore software program (as an alternative of corporations) that can assist you with the method for a smaller value. The advantage of credit score restore software program is that you are doing the work, so precisely what is occurring. It takes extra time, however it prices much less, and you might be in full management.

If in case you have no damaging objects (or no credit score historical past in any respect), they can not allow you to.