")

{kind=link}

Indus Towers Ltd. – Connecting Lives Throughout the Nation

Fashioned by the merger of Indus Towers and Bharti Infratel Restricted, Indus Towers Ltd. is without doubt one of the largest telecom tower firms globally. Integrated in 2006 and headquartered in Gurugram, the corporate gives tower and associated infrastructure sharing companies. As of March 31, 2024, Indus Towers operates over 219,736 towers and 368,588 co-locations throughout all 22 telecom circles in India, serving main gamers like Bharti Airtel, Vodafone Thought, and Reliance Jio.

Product Portfolio

- Tower Options: Providing quite a lot of designs—from ground-based and rooftop towers to hybrid poles and monopoles—for mounting operator antennae at optimum heights.

- Energy Options: Guaranteeing uninterrupted power provide to telecom tools, together with sustainable power choices.

- Area Options: Partnering with residential and industrial property house owners to accommodate telecom and energy tools wants.

Subsidiaries: As of FY23, Indus Towers has one subsidiary and no associates or joint ventures.

Development Methods

- Marquee Consumer Base: Enlargement of market share amongst main Telecom Service Suppliers (TSPs) on account of 5G deployment.

- Rural Enlargement: Ongoing rural growth efforts by main purchasers current alternatives for development.

- Document Tower Additions: Achieved the very best yearly tower additions in FY24, surpassing 200,000 towers.

- VIL Dues and Rollout: Maintained 100% assortment towards billing and made progress on previous dues assortment from Vodafone Thought Restricted (VIL).

Monetary Highlights

Q4FY24 Efficiency

- Income: Rs. 7,193 crore (up 7% YoY)

- Core Rental Income: Rs. 4,580 crore (up 7.7% YoY)

- Working Revenue: Rs. 4,072 crore (up 19% YoY)

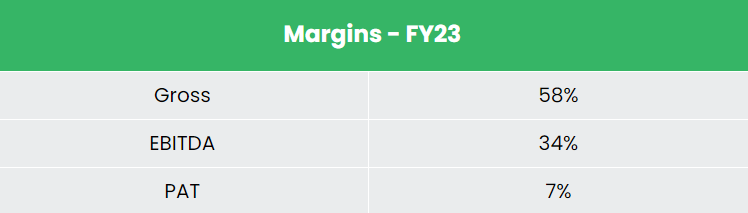

- EBITDA Margin: 57% (up 6 proportion factors YoY)

- Web Revenue: Rs. 1,853 crore (up 32% YoY)

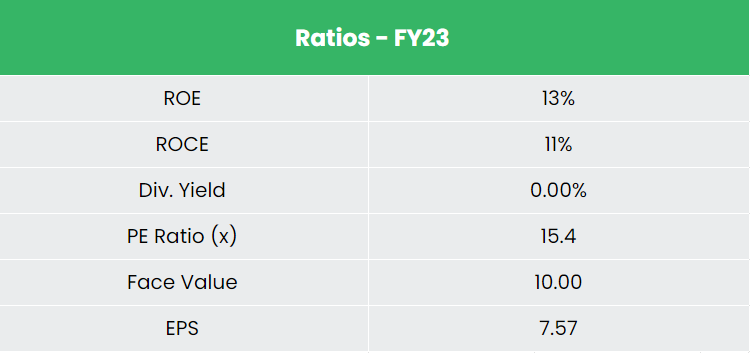

FY19-24 Monetary Efficiency

- Income and PAT CAGR: 33% and 22%

- ROE & ROCE: 22% and 20%

- Debt-to-Fairness Ratio: 0.76

Trade Outlook

- Market Dimension: India is the second-largest telecom market with 1,190.33 million subscribers as of December 2023.

- Inexpensive Tariffs and MNP: Wider availability and roll-out of Cell Quantity Portability enhance the market.

- Authorities Initiatives: Help for digitization and conducive regulatory setting.

- Cell Penetration: Anticipated addition of 500 million new web customers in 5 years.

- Tele-density: General 85.69%, with rural at 59.19% and concrete at 133.72%.

Development Drivers

- 100% FDI is now allowed within the telecom sector with the influx at US$ 39.31 billion between April 2000-December 2023.

- In Union Funds 2023-24, the Division of Telecommunications was allotted Rs. 97,579.05 crore (US$ 11.92 billion).

- India is aiming to fabricate cell phones price $126 Bn by 2025-26.

Aggressive Benefit

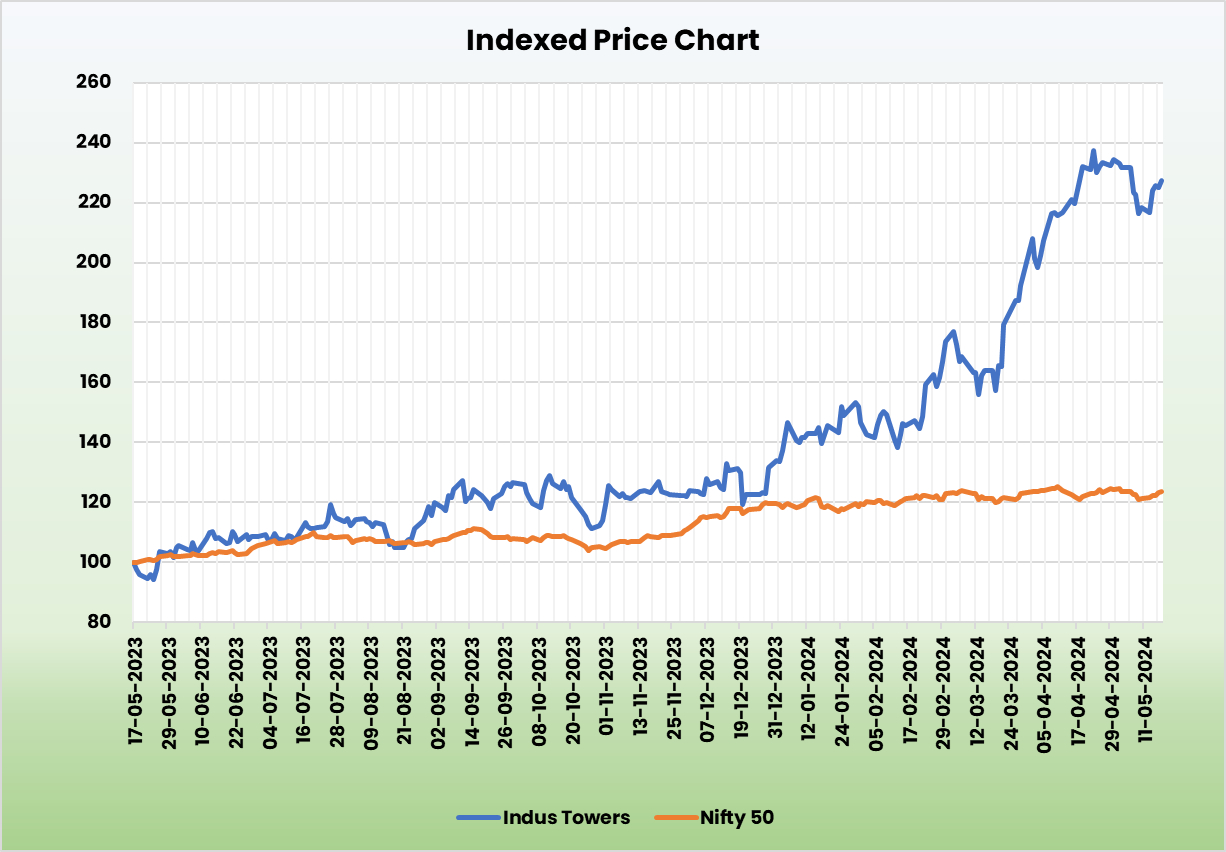

Indus Towers is probably the most undervalued inventory within the large-cap phase, persistently translating regular gross sales development into increasing margins and earnings in comparison with rivals like Suyog Telematics Ltd and Sar Televenture Ltd.

Outlook

- Market Share Features: Aiming to extend market share.

- Price Effectivity: Optimizing diesel consumption for value financial savings.

- Community Uptime: Guaranteeing excessive community uptime.

- Sustainability: Centered on sustainable practices.

- 5G Rollout: In depth 5G deployment resulting in elevated income streams.

- Development Alternative: Positioned to capitalize on the intersection of heightened information utilization and fast 5G adoption.

Valuation

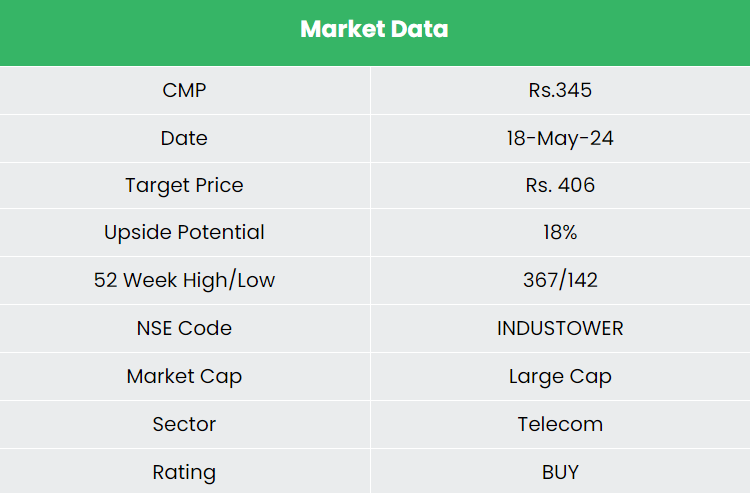

The wholesome demand outlook for telecom infrastructure, pushed by sturdy information consumption, accelerated 5G rollouts, and gaps in 4G companies, positions Indus Towers effectively for development. We advocate a BUY score within the inventory with the goal worth (TP) of Rs. 406, 14x FY26E EPS.

Dangers

- Monetary Stability of TSPs: Investments in 5G rollouts and spectrum acquisitions might pressure TSPs’ financials, affecting funds to Indus Towers.

- Contract Renewal Phrases: Unfavorable alterations to contract phrases with purchasers, akin to diminished pricing or escalations, pose dangers.

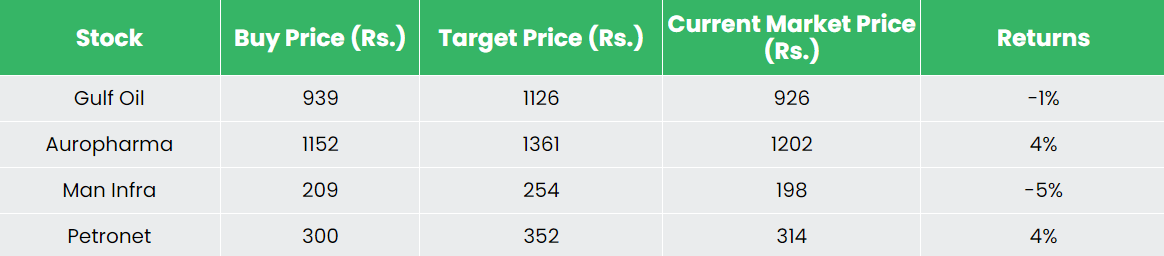

Recap of our earlier suggestions (As on 18 Might 2024)

Different articles you could like

Submit Views:

1,849