{kind=link}

The reply from caregivers is obvious.

Within the U.S. right now, roughly 38 million individuals present unpaid eldercare. That quantity is prone to dramatically enhance sooner or later because the variety of individuals needing care grows. One of many greatest challenges with unpaid care is…nicely, that it’s unpaid – and, in truth, it usually reduces individuals’s earnings. Offering care can require caregivers to take break day work, downshift to versatile jobs, or depart work fully. Given this monetary problem, it isn’t stunning that policymakers have targeted on supporting caregivers. The issue – as some colleagues identified in a new research – is that it isn’t clear which insurance policies would profit caregivers essentially the most.

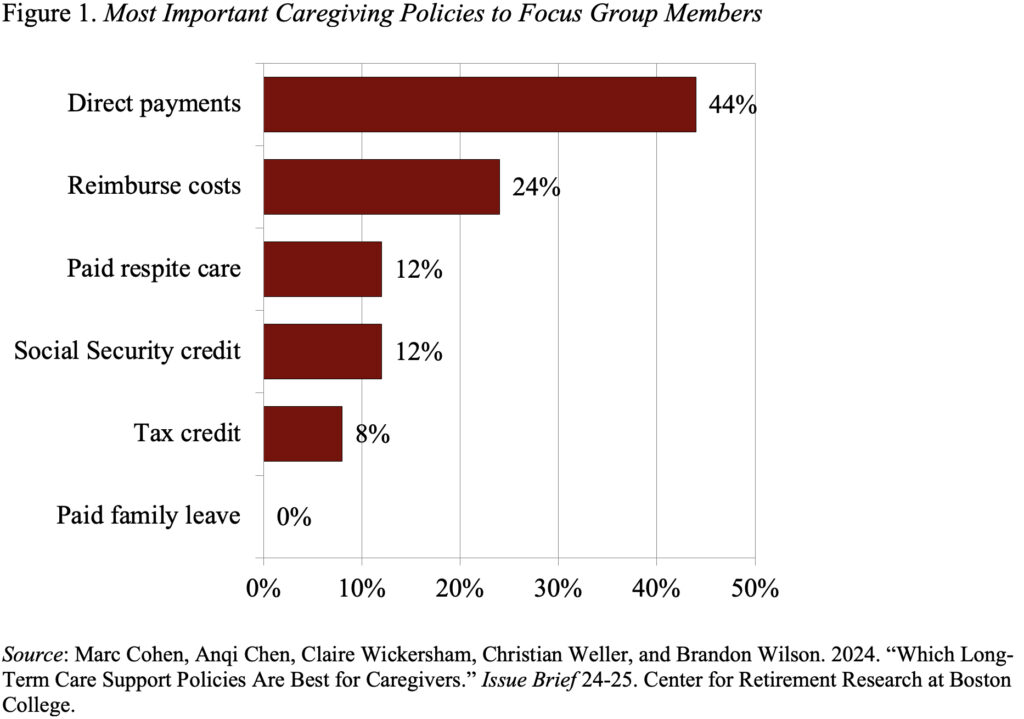

To discover what caregivers need, the research’s authors took a novel method – they requested them! Throughout a sequence of focus teams, the researchers coated six insurance policies: 1) paid household depart; 2) direct fee from the federal government for offering household care; 3) tax credit for offering care; 4) caregiver credit towards Social Safety advantages; 5) paid respite care; and 6) reimbursements for caregiver out-of-pocket prices. The teams included 25 caregivers ranging in age from 26 to 67 who different by earnings, race/ethnicity, and employment standing. Determine 1 summarizes the outcomes. Whereas caregivers appreciated any assist they might get, the highest two insurance policies share one factor in frequent: money, now!

Individuals had a lot much less enthusiasm for a few of the different insurance policies. Having respite care paid for was much less common relative to direct funds for just a few causes. As one caregiver put it succinctly: “I don’t belief many individuals.” Plus, others fearful whether or not the respite caregiver would be capable to work together with the care recipient. Or, as a spotlight group member put it: “[i]f you’re going to ship any individual in that’s not me, they would want physique armor.”

Credit fared even worse. The Social Safety credit score method – mainly caregivers would get a better Social Safety profit even when they don’t work for pay whereas caregiving – fell sufferer to a possible wrongdoer: time. In accordance with one focus group member: “I’m not [going to] retire for an additional 20 years, so I’d relatively have cash now.” Tax credit and prolonged sick depart had been much more unpopular, largely as a result of they’re tied to jobs that caregivers could also be unable to carry.

So, how do present insurance policies stack up in comparison with these caregivers’ preferences? Not too nicely. Whereas most states’ Medicaid packages do provide direct funds to casual caregivers, one focus group member identified the issues: “It’s a really lengthy approval course of, perhaps 4 to 6 months, and the individual you take care of has to obtain state-funded Medicaid.” And, whereas a tax credit score for caregiving bills exists, it’s non-refundable, so it might’t put money within the pocket of a caregiver, simply cut back their tax invoice. In any case, the credit score can solely be used for bills that allow the caregiver to carry a job or search for one – hardly helpful for retired caregivers or caregivers that can’t maintain a paid job.

OK, if present coverage falls quick, how about future coverage? Proper now, the principle motion on the state stage is on paid depart – which accurately nobody within the focus group appeared to prioritize. Some states are additionally investigating pay for respite care, a barely extra common method. On the federal stage, current congressional motion has targeted on Social Safety credit, a a lot much less most well-liked method throughout the focus group.

However, though present and proposed insurance policies fall quick, to me, a optimistic takeaway from these focus teams exists. One of the best ways to assist caregivers is perhaps the best – simply give them money. Tax credit or prolonged sick depart that tie advantages to jobs and Social Safety credit for the longer term miss two essential factors. Caregivers already are working, simply not for pay, and offering a useful service. And, they’re offering that service and struggling the monetary prices now. So, money now makes essentially the most sense.