{kind=link}

For those who’ve been paying consideration, you will have observed that mortgage charges have quietly crept again as much as practically 7%.

Whereas it appeared that these 7% mortgage charges have been a factor of the previous, they appeared to return simply as shortly as they disappeared.

For reference, the 30-year fastened averaged round 8% a 12 months in the past, earlier than starting its descent to just about 6% in early September.

It appeared we have been destined for five% charges once more, then the Fed charge minimize occurred. Whereas the Fed itself didn’t “do something,” their pivot coincided with some constructive financial stories.

Mixed with a “promote the information” occasion of the Fed minimize itself, charges skyrocketed. Nonetheless, now is likely to be a superb time to remind you that charges do are likely to fall for some time after charge cuts start.

Falling Charges Typically Play Out Over Years, Not Months

As famous, the Fed pivoted, aka lowered its personal fed funds charge, in September. They did so after growing their charge 11 occasions throughout a interval of tightening.

Therefore the phrase “pivot,” as they change from elevating charges to decreasing charges.

In brief, the Fed decided financial coverage was sufficiently restrictive, and it was time to loosen issues up. This tends to lead to decrease borrowing charges over time.

Whereas many falsely assumed the pivot would result in even decrease mortgage charges in a single day, these “within the know” knew these cuts have been largely already baked in, at the least for now.

So when the Fed minimize, mortgage charges really drifted a bit of increased, although not by a lot. The actual transfer increased post-cut got here after a better-than-expected jobs report.

These days, unemployment has taken heart stage, and a sturdy labor report tends to level to a resilient financial system, which in flip will increase bond yields.

And since mortgage charges observe the 10-year bond yield very well, we noticed the 30-year fastened soar increased.

After practically hitting the high-5s in early September, it fully reversed course and is now knocking on the 7% door once more.

How is that this potential? I assumed the excessive charges have been behind us. Effectively, as I wrote earlier this month, mortgage charges don’t transfer in a straight line up or down.

They will fall whereas they’re rising, and climb when they’re falling. For instance, there have been occasions after they moved down a whole share level throughout their ascent in 2022.

So why is it now shocking that they wouldn’t do the identical factor when falling? It shouldn’t be in the event you zoom out a bit of, however most can’t keep the course and include their feelings from dramatic strikes like this.

It Can Take Three Years for Mortgage Charges to Transfer Decrease After a Fed Pivot

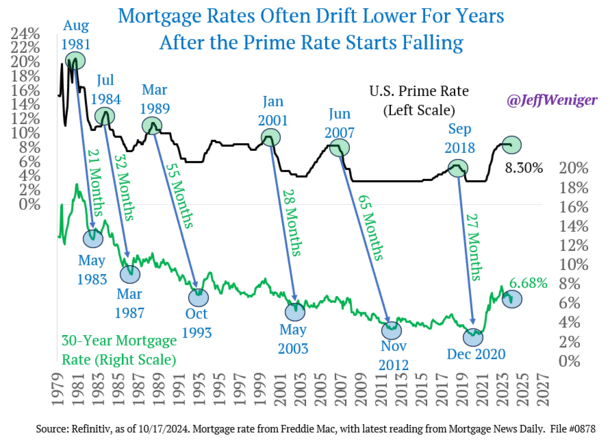

WisdomTree Head of Equities Jeff Weniger crafted a very attention-grabbing chart lately that checked out how lengthy mortgage charges are likely to fall after the prime charge begins falling.

He graphed six cases when charges got here down from 1981 by 2020 after prime was lowered. And every time, apart from in 1981, it took at the least two years for charges to hit their cycle backside.

If we mix all these falling mortgage charge durations and use the typical, it took 38 months for them to maneuver from peak to trough.

In different phrases, greater than three years for charges to hit their lowest level after an preliminary Fed minimize.

Because it stands now, we’re solely a month into the prime charge falling. However it’s vital to notice that charges had already fallen from round 8% a 12 months in the past.

They’ve now drifted again as much as round 6.875%, and it’s unclear in the event that they’ll proceed to maneuver increased earlier than coming down once more.

However the takeaway for me, in agreeing with Weniger, is that we stay in a falling charge surroundings.

Even when 30-year fastened charges hit 7% once more, it’s decrease highs over time as charges proceed to descend.

Which means we noticed 8% in October, 7.5% in April, and maybe we’ll see 7% this month. However that’s nonetheless a .50% decrease charge every time.

The following cease might be 6.5% once more, then 6%, then 5.5%. Nonetheless, it gained’t be a straight line down.

Nonetheless, it’s vital to concentrate to the longer-term pattern, as an alternative of getting caught up within the day-to-day motion.

Mortgage Lenders Take Their Time Reducing Charges!

I’ve stated this earlier than and I’ll say it once more for the umpteenth time.

Mortgage lenders will all the time take their candy time decreasing charges, however gained’t hesitate in any respect when elevating them.

From their perspective, it makes good sense. Why would they stick their neck out unnecessarily? Would possibly as properly gradual play the decrease charges in the event that they’re undecided the place they’ll go subsequent.

As a lender, in the event you’re in any respect fearful charges will worsen, it’s finest to cost it in forward of time to keep away from getting caught out.

That’s possible what is occurring now. Lenders are being defensive as normal and elevating their charges in an unsure financial surroundings.

If and after they see softer financial knowledge and/or increased unemployment numbers, they’ll start decreasing charges once more.

However they’ll by no means be in any rush to take action. Conversely, even a single constructive financial report, similar to the roles report that bought us into this case, will probably be sufficient for them to lift charges.

In different phrases, we would want a number of gentle financial stories to see mortgage charges transfer meaningfully decrease, however only one for them to bounce increased.

So in the event you’re ready for decrease mortgage charges, be affected person. They’ll possible come, simply not as shortly as you’d count on.

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) residence consumers higher navigate the house mortgage course of. Observe me on Twitter for warm takes.