{kind=link}

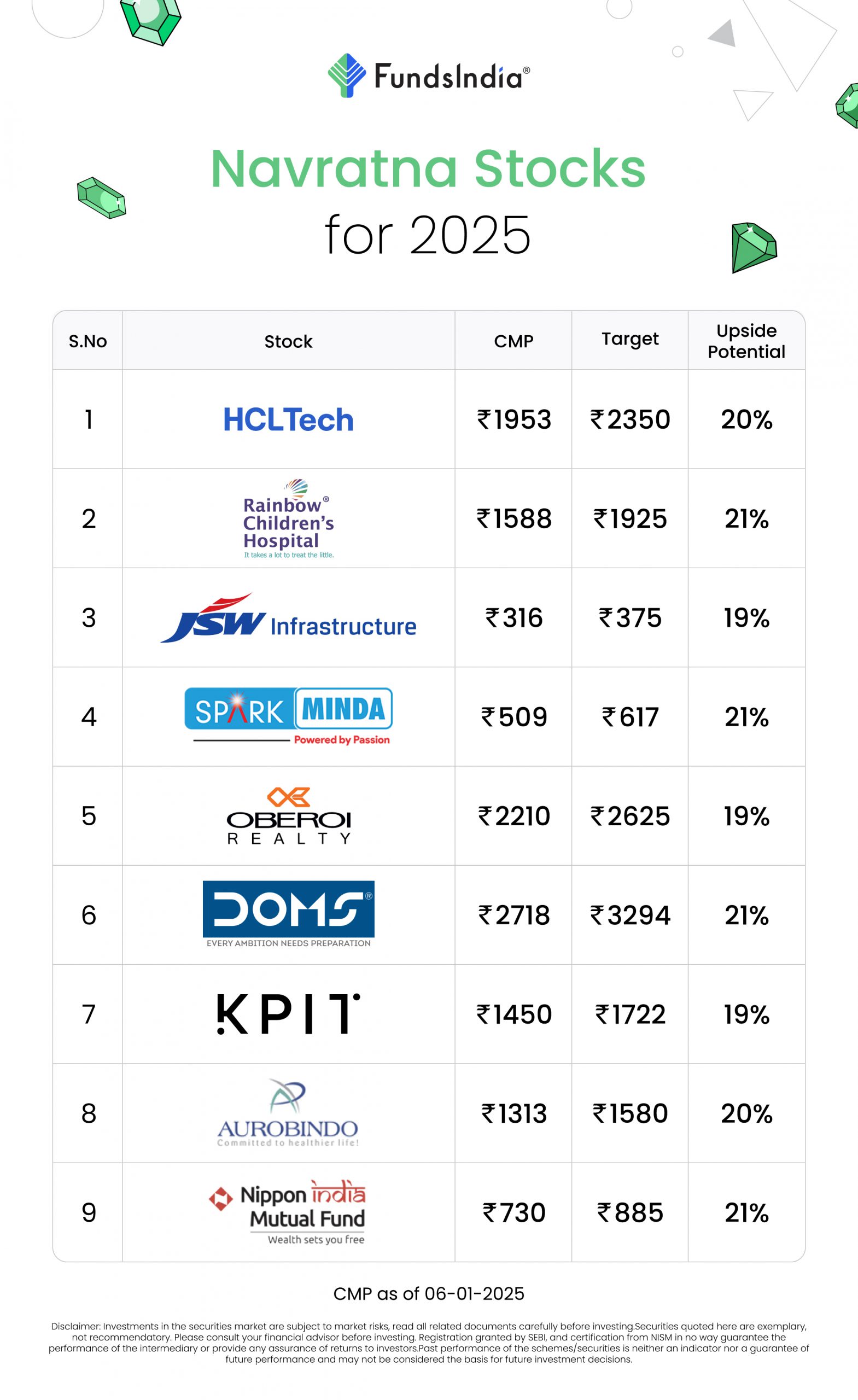

FundsIndia’s Navratna Shares for 2025

As we step into 2025, the FundsIndia Fairness Analysis Desk brings you an unique Prime 9 Inventory Picks for the 12 months, additionally referred to as FundsIndia’s Navratna Shares. Rigorously chosen after in-depth analysis, these shares symbolize a mix of sturdy fundamentals, sturdy development potential, and strategic {industry} positioning. At FundsIndia, we satisfaction ourselves on serving to traders make knowledgeable choices, and our workforce of consultants has labored tirelessly to handpick these gems. Whether or not you’re a seasoned investor or simply beginning your journey, our “Navratna” shares are designed to information you towards reaching your monetary targets.

HCL Applied sciences Ltd

HCL Applied sciences Ltd. is a worldwide expertise firm delivering industry-leading capabilities centered round digital, engineering, cloud and AI, powered by a broad portfolio of expertise providers and merchandise. The corporate caters to shoppers throughout main verticals, offering {industry} options for Monetary Providers, Manufacturing, Life Sciences and Healthcare, Know-how and Providers, Telecom and Media, Retails and Shopper Packaged Items (CPG) and Public Providers. The corporate generated income and internet revenue CAGR of 13% and 12% over the interval of three years (FY21-24). Common 3-year ROE & ROCE is round 23% and 28% for FY 21-24 interval. The corporate has a strong capital construction with a debt-to-equity ratio of 0.08.

The corporate has secured quite a few offers throughout the US, Europe, Asia, and Africa in AI and GenAI platforms. The Whole Contract Worth (TCV) for Q2FY25 stands at $2.2 billion, with a robust mixture of shoppers from varied sectors together with monetary providers, medical expertise, biopharma, telecom, semiconductor, and energy & vitality distribution. Just lately, the corporate acquired Zeenea, a Paris-based software program agency specializing in knowledge catalog and governance options, additional enhancing its knowledge and analytics enterprise. Administration is optimistic that GenAI will considerably enhance income streams. The strategic acquisitions and enlargement initiatives are anticipated to strengthen the corporate’s world market presence. We anticipate that HCL Applied sciences Ltd. will preserve its development trajectory, supported by its numerous order wins and execution capabilities.

Dangers:

- Foreign exchange Threat – The corporate has important operations in international markets and therefore is uncovered to foreign exchange danger. Any unexpected motion within the foreign exchange market can adversely have an effect on the corporate.

Rainbow Childrens Medicare Ltd

Integrated in 1998 and headquartered in Hyderabad, Rainbow Youngsters’s Medicare Ltd. is a number one pediatric multi-speciality and perinatal care hospital chain within the nation. The corporate is a complete supplier of pediatric and perinatal care providers providing holistic healthcare options that cowl the whole spectrum from fertility until conception, maternal care throughout being pregnant to foetal well being, new child via childhood care and gynecology providers. The income and internet revenue CAGR of the corporate for the previous 3 years is round 26% and 75% between FY21-FY24. The three-year common ROE and ROCE for the corporate is round 22% every for the previous 3 years. The corporate has a wholesome capital construction with a debt-to-equity ratio of 0.57.

The corporate is increasing its capability by including new beds in present amenities in addition to establishing new amenities throughout a number of places. With an purpose to reinforce retail expertise inside hospital amenities, the corporate is planning to launch “Butterfly Necessities,” a specialised retail retailer for ladies and kids. Its operational technique and enlargement plan are aimed toward capitalizing on important alternatives within the maternity and pediatric sectors. The expansion of its hospital community has pushed income development, and we anticipate the corporate to keep up this momentum. With its sturdy market place and futuristic enterprise methods, we’re assured that the corporate will proceed to develop alongside the huge potential in pediatric and maternity care.

Dangers:

- Regulatory danger – Healthcare is a extremely regulated {industry}, and modifications in healthcare and related insurance policies can affect money flows.

JSW Infrastructure Ltd

JSW Infrastructure Ltd. stands because the second-largest personal port operator in India with a cargo dealing with capability of 170 MTPA and a purpose to reinforce the capability to 400 MTPA by 2030. The corporate has 10 port and terminals amenities strategically positioned at key places alongside the East and West coasts of India together with multi-modal evacuation channels. The corporate’s monetary efficiency is powerful with a 3-year (FY21-24) income and internet revenue CAGR of 33% and internet revenue CAGR of 59% respectively, common 3-year ROE of 17% and ROCE of 15% backed by a wholesome capital construction with debt-to-equity ratio of 0.56.

The corporate has secured a number of orders from each authorities and non-government entities, each domestically and internationally, together with for railways and port operations, positioning it to fulfill its FY25 quantity development goal of 10-12%. It has additionally acquired a 70.37% stake in Navkar Company Ltd., a cargo transit service supplier. With important progress towards its long-term goal of enhancing logistics and last-mile connectivity throughout India, the corporate has set a capex steerage of Rs. 13,000-14,000 crore for the following three years. We imagine the corporate is strategically positioned to profit from the rising Indian financial system, substantial infrastructure growth, and powerful cargo development potential.

Dangers:

- Trade danger – A discount in financial exercise or slowdown in vital sectors could result in decreased cargo motion, probably impacting port utilization and income predictability.

Minda Company Ltd

Minda Company Ltd. is a number one auto-ancillary main catering to passenger and industrial autos, bikes, off-road autos and Tier 1 vehicle producers. With product portfolio spanning throughout Mechatronics, Electrical Distribution System, Inside Plastic Division, Drivers Info System and many others., the corporate has presence in India in addition to worldwide markets corresponding to Indonesia, Vietnam, Europe, Japan and Uzbekistan. The corporate has generated income and internet revenue CAGR of 25% and 35% over the interval of three years (FY21-24). Common 3-year ROE & ROCE is round 15% every for FY21-24 interval. The corporate has a strong capital construction with a debt-to-equity ratio of 0.25.

The corporate is making important investments to broaden its manufacturing capability. Within the first half of FY25, the full lifetime order guide surpassed Rs.4,750 crore, and the variety of patents exceeded 285, with 14 new patents filed through the interval. Moreover, the corporate has entered right into a expertise license settlement with SANCO (China) to enhance its wiring harness product for the electrical automobile (EV) market. To fulfill the growing demand, the corporate is establishing 4 new amenities – two in diecasting, one within the instrument cluster division, and one within the wiring harness element division. By aligning with future developments and growing manufacturing capabilities, we imagine the corporate is positioning itself for long-term development.

Threat:

- Socio-economic danger – Any socio-economic instability that might end in a rise in enter prices corresponding to uncooked materials, freight prices, and many others. may negatively affect the margins and profitability.

Oberoi Realty Ltd

Integrated in 1998 and headquartered in Goregaon, Oberoi Realty Ltd. is targeted on premium developments in residential, workplace area, retail, hospitality and social infrastructure tasks. The corporate is among the strongest manufacturers in Mumbai Metropolitan Area (MMR). The corporate generated income and PAT CAGR of 30% and 34% over the interval of three years (FY21-24). The common 3-year ROE & ROCE is at 14% every for FY21-24. The corporate has a robust stability sheet with a strong debt-to-equity ratio of 0.14.

The corporate has a strong pipeline of upcoming launches in key places, together with two towers in Goregaon, one in Borivali, and two in Thane (Kolshet and Pokhran). Development is already underway, with work progressing on flooring 10 to fifteen. As well as, the corporate is on the lookout for alternatives to broaden past the MMR area, significantly concentrating on Delhi NCR. It’s anticipated to boost Rs.6,000 crore, which is anticipated to generate a Gross Improvement Worth (GDV) of Rs.70,000-80,000 crore over the following few years. We imagine the corporate will preserve its development trajectory because of its sturdy market place, environment friendly execution, wholesome cashflows, and a stable pipeline of upcoming tasks, making certain clear income visibility for the longer term.

Threat:

- Macro-economic situations – Modifications in macro-economic situations corresponding to excessive inflation, financial slowdown, excessive rates of interest and many others. may have an effect on the corporate turnover.

Doms Industries Ltd

Integrated in 2006, DOMS Industries Ltd. is a stationery and artwork product firm primarily engaged in designing, creating, manufacturing, and promoting a variety of those merchandise below the flagship model, DOMS. The merchandise provided by the corporate embrace pencil and equipment, drawing, colouring and paper stationery, mathematical drawing devices, marker pens and many others. The corporate has generated a income and internet revenue CAGR of 56% and 190% over the interval of three years (FY21-24). Common 3-year ROE & ROCE is round 24% and 25% for FY21-23 interval. The corporate has a robust stability sheet with a strong debt-to-equity ratio of 0.23.

With 16 manufacturing amenities throughout 4 places supported by a community of 11,500+ staff and 4,750+ distributors, the corporate sells its merchandise throughout 50+ international locations. The corporate has accomplished the acquisition of practically 52% stake in Uniclan Healthcare, a producer of child hygiene merchandise. The corporate can also be endeavor a 20% capability enlargement in mathematical instrument bins, initiatives to enhance the utilization of its third pen plant to most capability of 1 million pens per day and a 20% enhance in guide manufacturing capability. The corporate’s continued give attention to launching new merchandise and enlargement into new product classes backed by strong distribution community are anticipated to be key development drivers.

Threat:

- Uncooked materials value volatility – Volatility in uncooked supplies costs could have an effect on the earnings and revenue margins.

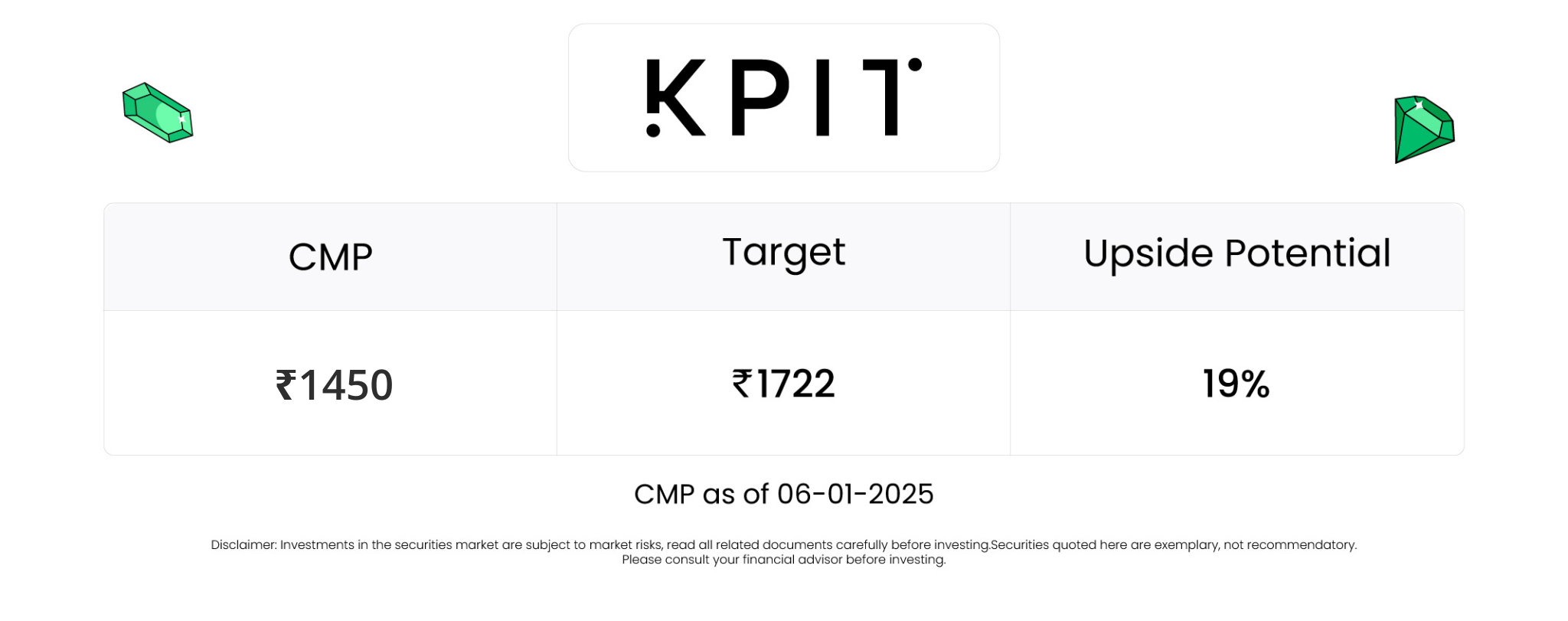

KPIT Applied sciences Ltd

Based in 2018 and based mostly in Pune, KPIT Applied sciences Ltd. is a number one software program and system integration associate for the worldwide mobility ecosystem. The corporate is a trusted collaborator for main automotive {industry} leaders, having established over 25 strategic partnerships with Authentic Gear Producers (OEMs) and Tier 1 suppliers to drive mobility transformation. The corporate has generated income and PAT CAGR of 34% and 61% over the interval of three years (FY21-24). Common 3-year ROE & ROCE is round 27% and 31% for FY 21-24 interval. The corporate has a strong capital construction with a debt-to-equity ratio of 0.14.

The corporate plans to spice up profitability by securing extra fixed-price tasks. Administration can also be specializing in strategic partnerships and potential acquisitions to strengthen its market place. Leveraging its experience in rising applied sciences, together with deep shopper relationships and trusted partnerships, has led to important deal wins. Along with buying new offers from the prevailing shoppers, the corporate is in discussions with new shoppers from Europe and America to construct long-term giant engagements.

Threat

- Foreign exchange danger – The corporate has important operations in international markets and therefore is uncovered to foreign exchange danger. Any unexpected motion within the foreign exchange market can adversely have an effect on the corporate.

Aurobindo Pharma Ltd

Integrated in 1986 and headquartered in Hyderabad, Aurobindo Pharma Ltd. is an built-in world pharmaceutical firm engaged within the growth, manufacturing, and commercialization of a variety of generic prescribed drugs, branded specialty prescribed drugs, and lively pharmaceutical elements (APIs) worldwide. The corporate has generated income and PAT development of 12% and 54% during the last twelve months (TTM). The common 3-year ROE & ROCE is round 10% and 12% FY21-24 interval. The corporate has a strong capital construction with a debt-to-equity ratio of 0.27.

The corporate launched 14 merchandise and obtained approval for 8 ANDAs throughout Q2FY25. It’s actively increasing its capacities in China and throughout product segments like Penicillin G, 6-APA, and Granulation, which can enhance operational efficiencies and assist obtain development goals within the upcoming quarter. Penicillin G product facility is predicted to break-even by Q4FY25 and begin contributing positively from FY26 onwards. The corporate is concentrating on EBITDA margin of 21-22% in FY25. The administration is assured in sustaining development momentum, supported by elevated volumes, new product launches and secure pricing dynamics.

Threat:

- Regulatory danger – Vulnerability to regulatory modifications, particularly scrutiny by companies like USFDA may affect operations.

Nippon Life India Asset Administration Ltd

Established in 1995, Nippon Life India Asset Administration Ltd. is engaged in managing mutual funds together with trade traded funds (ETFs), managed accounts, together with portfolio administration providers, various funding funds and pension funds; and offshore funds and advisory mandates. It’s the 4th largest AMC based mostly on Quarterly Common Property Below Administration (QAAUM). Additionally it is ranked no 1 non-bank sponsored MF in India.

Throughout Q2FY25 (YoY comparability), the corporate’s SIP folio elevated from 71 million to 99 million, a 39% development. SIP AUM elevated by 59% YoY to Rs.13,817 crore from Rs.8,704 crore of corresponding quarter within the earlier 12 months. The corporate’s income elevated by 44% to Rs.5,713 million, core working revenue elevated by 57% to Rs.3,653 million and internet revenue elevated by 47% to Rs.3,601 million.

Threat:

- Regulatory Threat – Any hostile change of laws may adversely affect the enterprise.

The Finish Be aware

2025 guarantees to be a 12 months crammed with alternatives, and we at FundsIndia are excited to stroll this journey with you. The FundsIndia’s Navratna inventory picks may be your approach of beginning the 12 months crammed with development, stability, and prosperity on your investments. Keep dedicated, keep invested, and let’s make this 12 months a milestone in your monetary journey. We want a profitable and affluent 2025 for all our traders!

Be aware: Please notice that this isn’t a advice and is meant just for academic functions. So, kindly seek the advice of your monetary advisor earlier than investing.

Different articles you might like

Submit Views:

282