{kind=link}

On December 1st, 1986, my Mother took me to open my first checking account on the native Greenback Financial institution department. I used to be 11 years outdated and a bit of skeptical of giving the financial institution teller my $21.60.

On December 1st, 1986, my Mother took me to open my first checking account on the native Greenback Financial institution department. I used to be 11 years outdated and a bit of skeptical of giving the financial institution teller my $21.60.

I walked out with a small inexperienced booklet that seemed like a passport.

My dad and mom thought it was the fitting second for me to have an account for the birthday and vacation cash from my aunts and uncles. In addition they wished me to be prepared for once I began incomes my very own earnings down the highway.

That made sense. However the inexperienced e book? That was sudden. What’s a passbook financial savings account?

The second journey to the financial institution department fully blew my thoughts.

How I Realized About Curiosity

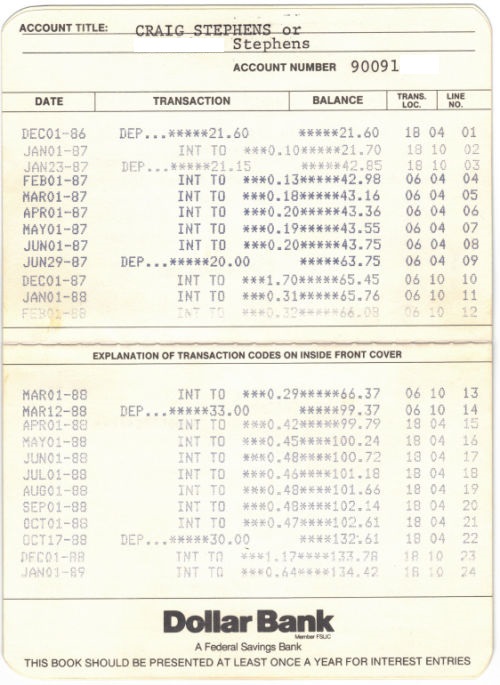

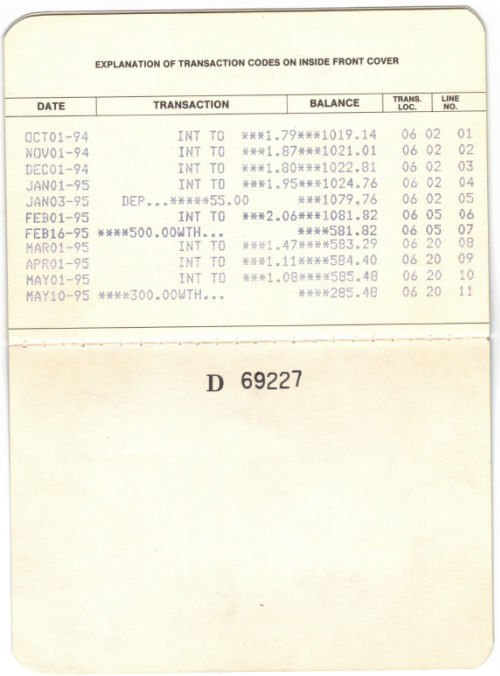

On January twenty third, 1987, I returned to the financial institution to deposit one other $21 and alter. The teller took my passbook, slid it right into a printer, and handed it again.

The primary web page now had three entries:

- The primary deposit: $21.60

- An “INT TO” transaction on January 1st: $0.10

- And the second deposit: $21.15

I requested my Mother what the “INT TO” meant and why the financial institution gave me $0.10.

In my Mother’s very non-financial phrases, she defined that banks pay curiosity while you deposit your cash.

Why would they offer me free cash?

She defined in 11-year-old phrases how banks take deposits and lend cash. I didn’t get the lend half, however this free cash factor was cool.

So that they pay me simply to carry onto my cash?

Greenback Financial institution paid me 5.5% curiosity on my passbook financial savings account. It was the primary curiosity/passive earnings I ever earned.

My 11-year-old mind thought: That is repeatable; this could scale.

And so started a lifelong obsession with passive earnings and compound curiosity.

Beginning to Earn

Each few months over the next years, I’d make a deposit anytime I had extra money and a experience to the native strip mall the place the financial institution department was,

Extra thrilling, I’d get new curiosity entries into my passbook financial savings e book.

I picked up a newspaper route once I was 13. I delivered an area paper referred to as the North Hills Information Document on Tuesdays and Thursdays for just a few years, round 1988-1990.

As soon as a month, I’d stroll the route to gather subscription dues, then consolidate the collections and ship a test to the paper firm.

No matter was left over was mine.

You’d assume that my financial savings would begin to surge right here. However sadly, I hated amassing and generally let a buyer or two slide who didn’t have the money.

One home had a nasty canine that might chase me away.

It wasn’t a really worthwhile newspaper route, and it was difficult to proceed extracurriculars with the duty of doing so twice per week. So, across the flip of the last decade, I handed it on to another person.

The financial institution by no means skipped an curiosity fee or chased me down the road.

The First Withdrawal

By the summer season of 1989, the 14-year-old in me noticed a bulging checking account, and it was time to spend a few of it.

I withdrew $50 simply earlier than our summer season trip to Stone Harbor, NJ.

That’s the place I made the most important buy of my life: a Morey Boogie Waimea Professional physique board.

The board was a mannequin from the earlier yr and had a small dent on the again. A good friend was with me and identified a ding to the salesperson, and he negotiated a 15% low cost. The overall price was $79 with tax.

For the quantity of use I acquired out of that board, it’s probably the greatest purchases I’ve ever made. Costco sells boards for $30 now, however I digress.

Higher Paying Gigs and a Journey to Italy

All these years of aggressive swimming and bodyboarding lastly began to repay financially once I started lifeguarding at age 15.

I labored progressively extra hours every summer season by way of the top of my Freshman yr of school. The summer season paychecks began to resemble a gentle earnings.

A quick mall job promoting sneakers for fee at Thom McAn’s gave me some low season earnings to pay for an upcoming journey.

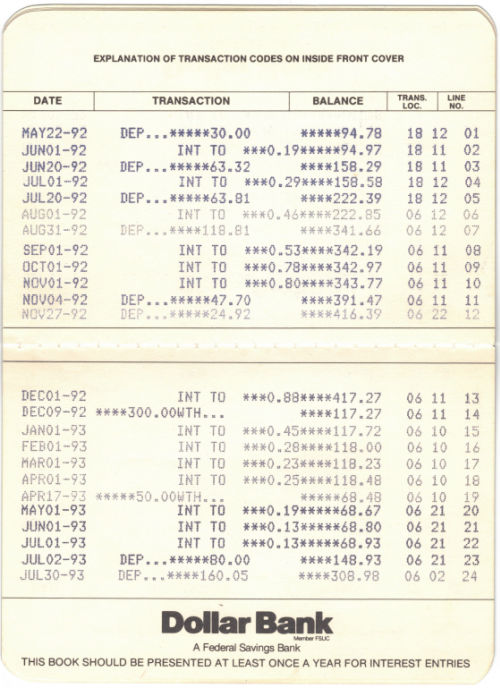

In December 1992, I withdrew $300 for a down fee on a summer season journey to Italy with my Latin class. I’m grateful to my dad and mom, who footed the remainder of the invoice.

Off to Faculty

My father or mother’s associates and neighbors all attended my commencement social gathering and lower checks. It was profitable on the time, but it surely’s costing me as we speak as I really feel obligated to pay it ahead each time somebody graduates.

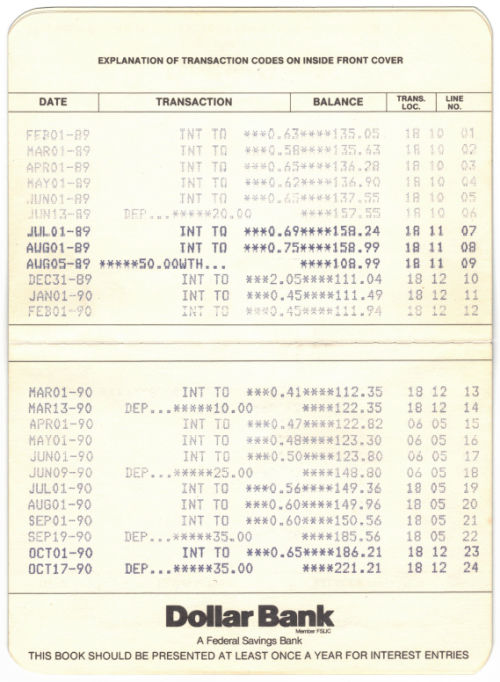

In September 1994, I headed off to East Lansing, Michigan, withdrawing $500 to deposit at my new account with the MSU Credit score Union. It turned my major checking account for the following 4 years.

However I saved the Greenback Checking account open for a while afterward. I’m unsure how lengthy as a result of by 1995, I crammed up the e book and haven’t any extra file of the place the cash went.

I used to be answerable for my very own spending cash in school. I labored in a college pictures lab all 4 years, growing movie and printing photographs for the college e-newsletter.

In the summertime of 1996, I gave up lifeguarding to hire seashore chairs, umbrellas, and bodyboards (in fact).

No matter I might earn made it to the credit score union, however finally went towards $1.25 pitchers of Miller Excessive Life and Shark Bowls on the Landshark and a 60-day 15-country backpacking journey to Europe once I graduated.

It was most likely round 1998 once I closed the passbook financial savings account and moved my cash to PNC Financial institution as a result of it had branches in each Pittsburgh and D.C. Sooner or later, I switched to Wachovia, which quickly fell aside in the course of the 2008 disaster, and Wells Fargo picked up the items.

Wells Fargo was a dependable financial institution till simply final yr once I skilled an extremely idiotic episode with them and sadly needed to go away in 2024.

This brings me to why I went in search of my outdated passbook financial savings account.

Youngsters Banking

This summer season, I used to be curious how outdated I used to be once I acquired my first checking account as a result of my son turned 12 this yr, and it appeared an applicable time to open his first checking account.

Sadly, common on-line household banking merchandise like Greenlight cost a month-to-month payment. That firm contacted RBD way back about being an affiliate companion, however I can’t suggest it.

The place I’m from, banks pay me, not the opposite means round.

So, I looked for a financial institution that doesn’t cost a recurring payment, pays a good rate of interest, and has native branches so my youngsters can expertise what it’s wish to stroll right into a financial institution and make a deposit.

I landed on the Capital One Youngsters Financial savings Account.

Due to its no-fee banking and aggressive financial savings charges, we’re shifting almost all of our banking to Capital One, together with checking, financial savings, and three youngsters financial savings accounts.

My son downloaded the Capital One 360 app, and on this October 1st, he skilled his personal first curiosity fee of $1.01 on a $500 deposit.

It’s not fairly the identical as a passbook financial savings account. I’ve held onto my youngsters’ cash in a spreadsheet with the “financial institution of Dad”, so that they haven’t had a lot duty thus far. Their grandparents give a lot increased sums than I used to obtain.

Capital One solely pays 2.50% on youngsters’ financial savings accounts in comparison with the superb financial savings charges Greenback Financial institution paid again within the day. However there’s a teen debit card account he can finally hyperlink to, and there are not any month-to-month charges or minimums for any of us to fret about.

To my shock, Greenback Financial institution nonetheless has the passbook financial savings account, but it surely solely pays 0.10%, and its finest financial savings account pays simply 2%.

Bodily banks simply don’t pay curiosity like they used to. We’ve to go surfing banks to seek out the highest-yield financial savings accounts. My new Capital One account pays 4.10% as of October 2024, and I’m content material with the comfort of all my household banking underneath one roof.

To get a barely increased yield, I can transfer cash into the M1 Finance high-yield money account (not a financial savings account, technically, however nonetheless FDIC-insured). Robinhood, Webull, Public, and plenty of brokers now provide related merchandise.

Tidbits

Just a few issues made me giggle about this, particularly depositing $0.60 and $.15 on my first two visits.

I confirmed the e book to my neighbor, who works for the FDIC, and he seen that this account was initially insured by the Federal Financial savings and Mortgage Insurance coverage Company (FSLIC).

FSLIC turned bancrupt in the course of the financial savings and mortgage disaster of the Eighties. FSLIC was abolished, and the deposit insurance coverage duty was transferred to the FDIC. Greenback Financial institution survived.

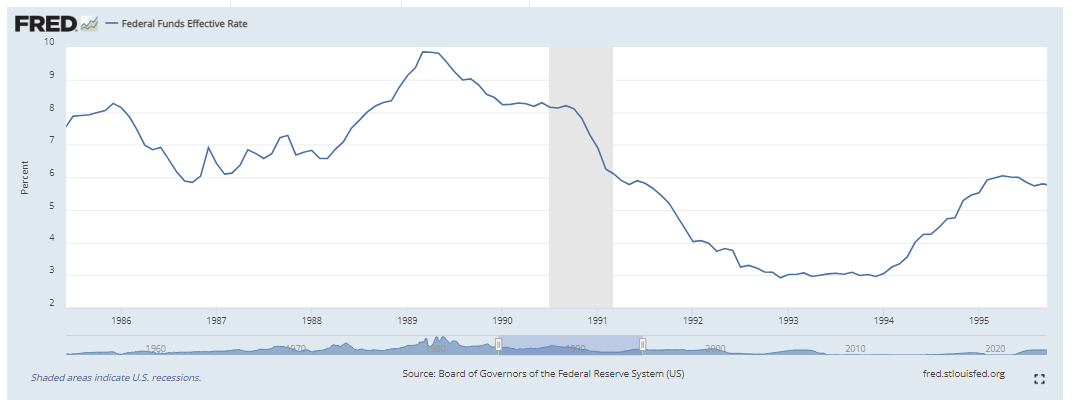

It’s additionally shocking to see the excessive financial savings yields at a bodily financial institution department. It’s almost unthinkable as we speak, because the highest-yielding financial savings accounts are on-line banks.

That is only some years after the aggressive Fed motion within the early 80s led by Paul Volker. The financial institution paid me 5.75% when charges peaked once more in April 1989. Under is a chart of the approximate lively timeline for this account.

Conclusion

I assumed this passbook financial savings e book was lengthy gone, however I discovered it in a field alongside some highschool memorabilia.

One of the best half about my passbook financial savings account is it taught me about banking, curiosity, and the foundations of constructing wealth. That first $0.10 was small, but it surely was step one on a protracted path towards the place I’m as we speak.

The joy I acquired from financial institution curiosity partly led me to check finance in school, the place I realized about shares and different investments. Enterprise courses launched me to monetary formulation, monetary modeling, and the economics that drive wealth.

My Uncle gave me my first inventory share throughout my Sophomore yr. Then, I began contributing to my company 401(ok) the day I began working.

Digitalization makes banking much less tangible for youths as of late. We’ll head to the native department subsequent time he receives a test. I hope that this new checking account begins to nudge my son on his personal path to wealth. His two sisters are subsequent.

Craig Stephens

Craig is a former IT skilled who left his 19-year profession to be a full-time finance author. A DIY investor since 1995, he began Retire Earlier than Dad in 2013 as a artistic outlet to share his funding portfolios. Craig studied Finance at Michigan State College and lives in Northern Virginia along with his spouse and three youngsters. Learn extra.

Favourite instruments and funding providers proper now:

Boldin — Spreadsheets are inadequate. Construct monetary confidence. (overview)

Certain Dividend — Analysis dividend shares with free downloads (overview):

Fundrise — Easy actual property and enterprise capital investing for as little as $10. (overview)

M1 Finance — A high on-line dealer for long-term traders and dividend reinvestment. (overview)