{kind=link}

I used to be lately invited to talk on the EconoMe convention in regards to the course of of making extra correct retirement projections. In making ready for my speak, I reviewed Darrow’s intensive work on retirement calculators on this weblog.

I wish to increase upon an idea he’s written about: calculator constancy. Understanding it is step one in selecting the best retirement calculator to fulfill your wants.

Calculator Constancy

In our itemizing of The Finest Retirement Calculators, a method Darrow allowed sorting is by “constancy.” Right here is how he described this idea:

“Credit score goes to Stuart Matthews of Pralana Consulting (affiliate hyperlink) for this useful idea. By constancy we’re referring to how properly every calculator can doubtlessly reproduce actuality — the realism of its simulation.

In a nutshell, to do a greater modeling job, a calculator might want to gather extra knowledge, and extra correct knowledge, from you. So, “constancy” can also be a tough measure of accelerating complexity:

- Low-Constancy — these calculators will characteristic only a dozen enter fields or much less, and normally carry out solely a easy mounted price/common return calculation. They characteristic ease of use, and customarily would require lower than 5 minutes of your time to provide solutions.

- Medium-Constancy — these calculators add extra fields, normally dealing with a number of accounts with completely different asset allocations, and arbitrary monetary “occasions” corresponding to irregular future earnings or bills. Typically they may require 10-20 minutes of your time to provide solutions.

- Excessive-Constancy — these calculators will add much more enter fields, the flexibility to match eventualities, and sometimes Social Safety and tax calculations. Typically they’ll require no less than 30-60 minutes of your time to provide solutions. They usually might simply require a number of hours to grasp all of the choices, and gather and enter all the information to take full benefit of their capabilities. However these calculators have the potential to be most correct, assuming you’re taking the time to enter good knowledge, and assuming your guesses in regards to the future maintain true.”

Totally different Instruments for Totally different Functions

I discover this idea of calculator constancy extraordinarily useful in understanding these instruments and selecting the perfect one on your wants. Nevertheless, it understates simply how completely different they’re, which is “greatest,” and thus which it is best to select.

In my presentation, I used an analogy of a steak knife and a chainsaw to distinction the magnitude of distinction between low and high-fidelity calculators. At their core, a steak knife or a chainsaw is a slicing system. Every serves a goal.

Should you order a pleasant filet mignon, a steak knife is clearly the “greatest” slicing software. But when a wind storm takes down a tree in your yard, the steak knife is ineffective. You need the chainsaw.

That is much like the magnitude of distinction between high and low constancy retirement calculators. They’re each calculators at their core. However they’re very completely different instruments serving completely different functions.

This will greatest be demonstrated with a case examine run on a couple of of the perfect calculators of their class.

Case Examine Parameters

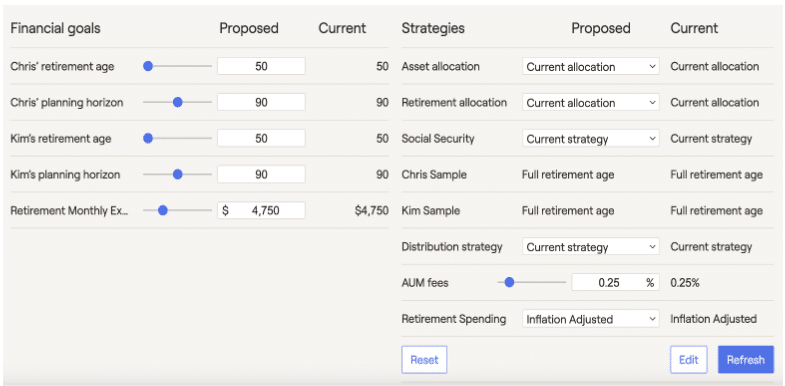

I created a comparatively easy case examine to showcase calculators at completely different constancy ranges. The parameters are as follows:

- A married 50 yr outdated couple at or close to early retirement

- Anticipated life expectancy is 90 years of age (i.e. 40 yr retirement time-frame)

- Bills of $80,000 yr

- Plus funding bills of .25% of their portfolio worth

- $2 million portfolio

- Allocation: 60% inventory/ 35% bonds/ 5% money

- Tax Allocation: 50% tax-deferred, 30% taxable, 20% Roth

- Inflation assumption of three.5%

- Equivalent Social Safety advantages of $1,500 every at their full retirement age (67 y/o)

This case was purposefully simplified for ease of information entry and readability of demonstration. I selected a couple of calculators that I had used up to now, so I had some preexisting data. Nevertheless, I hadn’t used any of those calculators often for no less than two years whereas I used to be centered on different points. This allowed me to have a look at these instruments via new eyes.

I additionally evaluate how calculators obtainable to most of the people evaluate to skilled monetary planning software program I take advantage of with my planning purchasers.

Low Constancy

I began by working this state of affairs on two low constancy calculators:

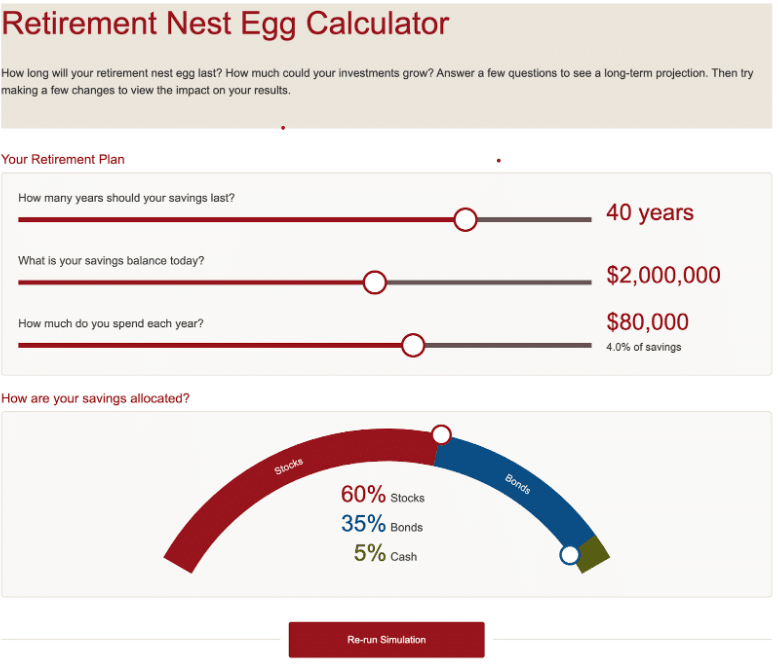

Vanguard

The Vanguard calculator provided solely 4 inputs:

- How lengthy financial savings ought to final

- Right this moment’s steadiness

- Annual spending

- Asset allocation (% every to shares, bonds, and money)

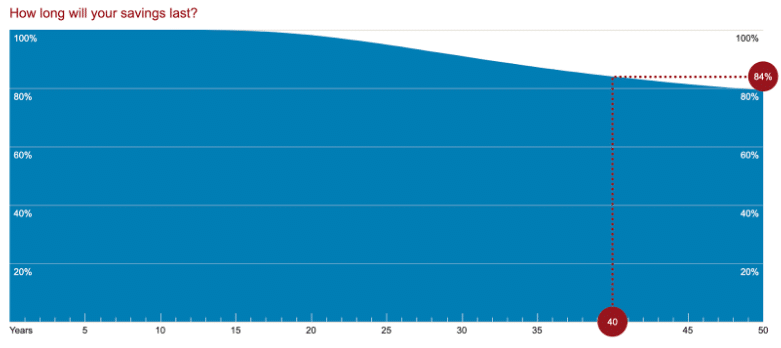

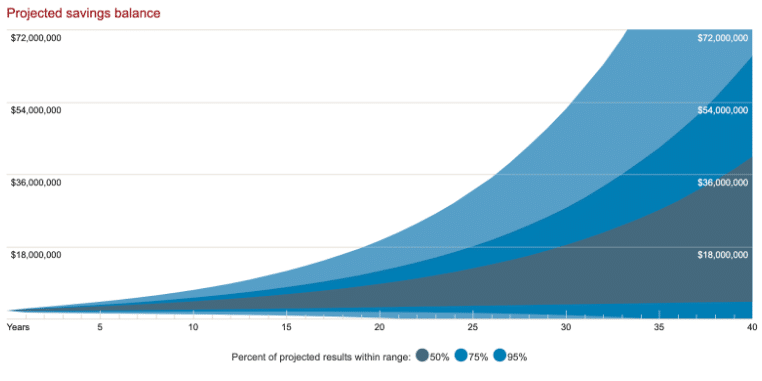

The calculator then carried out a Monte Carlo evaluation of 1,000 eventualities and produced two outputs in graphical type:

- How Lengthy Your Financial savings Will Final

- Projected Financial savings Stability

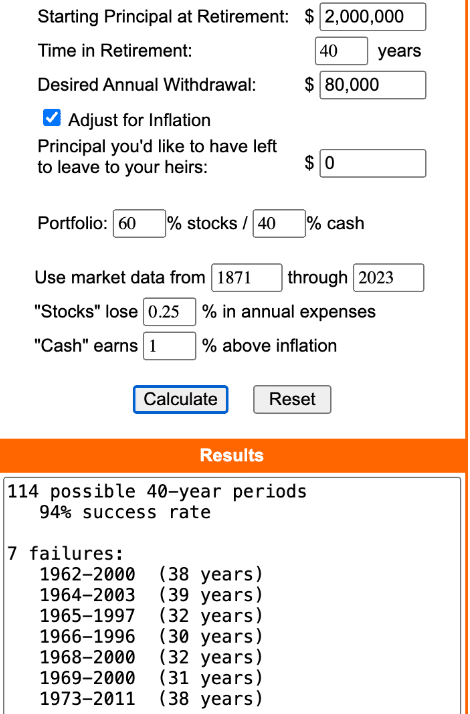

Moneychimp

Moneychimp’s retirement calculator provided a equally easy to make use of and straightforward to grasp interface.

Inputs embody:

- Beginning principal

- Time in retirement

- Desired annual spend (with means to regulate for inflation)

- Desired terminal account steadiness

- Asset allocation (% shares and money with means to mannequin money returns as % above inflation)

- Funding bills

Moneychimp’s calculations are primarily based on historic inventory returns mixed with a person chosen actual (above inflation) price of “money” return.

Inputs and outputs have been in a position to be captured in a single screenshot. This calculator additionally features a good rationalization of strategies and a few suggestions to assist interpret the information.

Low-Constancy Cons

Clearly, low-fidelity calculators have limitations. Neither was in a position to account for even a single enter for Social Safety. Vanguard couldn’t account for funding charges in my easy case.

Neither contemplate if somebody is on observe to retire, account for various retirement dates for spouses, or are in a position to mannequin irregular earnings or bills (sale of a house, buy of autos, working part-time for five years of retirement, and so on.). There is no such thing as a accounting for taxes.

Low-Constancy Execs

That doesn’t imply these instruments are with out worth. Their simplicity makes it straightforward to get began. I spent lower than 5 minutes with every one between touchdown on the internet web page and getting helpful output.

This may be immensely useful for somebody who’s simply beginning and attempting to get a grasp on the important thing variables that decide success or failure in retirement calculations. The affect of small adjustments that movement via and compound over a multi-decade plan will not be intuitive for most individuals.

You possibly can check variables shortly:

- What in case your burn price was a half a % decrease? Or larger?

- Do 1% advisor charges added to your portfolio actually matter?

- How does a extra (or much less) inventory heavy allocation affect outcomes?

- What if my retirement lasts 30 years as an alternative of 40? Or 50?

As a result of the calculations are fast, easy, and crude, it’s clear that you just don’t wish to make main life altering selections primarily based on one, and even a number of of those low-fidelity calculators. However they are often useful for somebody within the early levels of planning to get within the ballpark and get a really feel for retirement calculations with out changing into overwhelmed. For the correct particular person on the proper time, low constancy calculators are a superb software.

Medium Constancy

Subsequent, I ran my state of affairs via two medium constancy calculators:

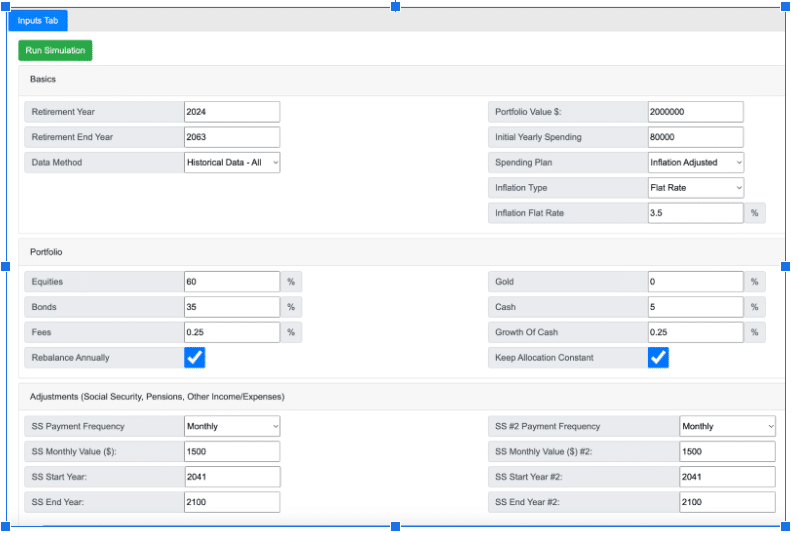

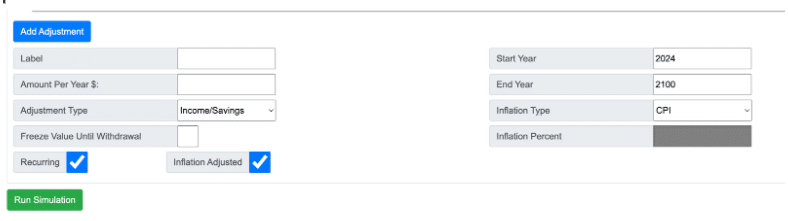

cFIREsim

cFIREsim simply dealt with all the variables in my easy state of affairs besides one. It couldn’t account for various taxation of tax-deferred, taxable, and Roth accounts. Along with taking up the remainder of the variables, it had the capability to deal with significantly extra modeling complexity.

The inputs I wanted have been all captured on one screenshot (when undefined by my case, I went with calculator defaults):

This software can also mannequin irregular earnings, saving, and spending occasions:

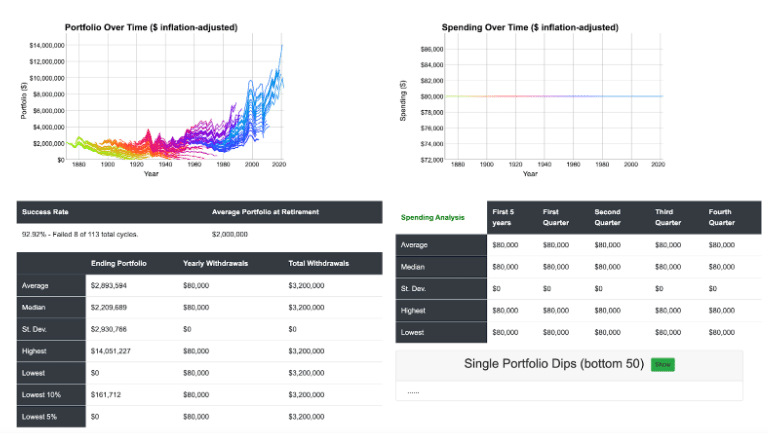

cFIREsim gives concise graphical and tabular outputs. In my case, I chosen modeling historic returns. As you possibly can see, the correct aspect of the outputs have been pointless for my easy state of affairs, demonstrating the flexibility of this software to deal with extra complicated modeling.

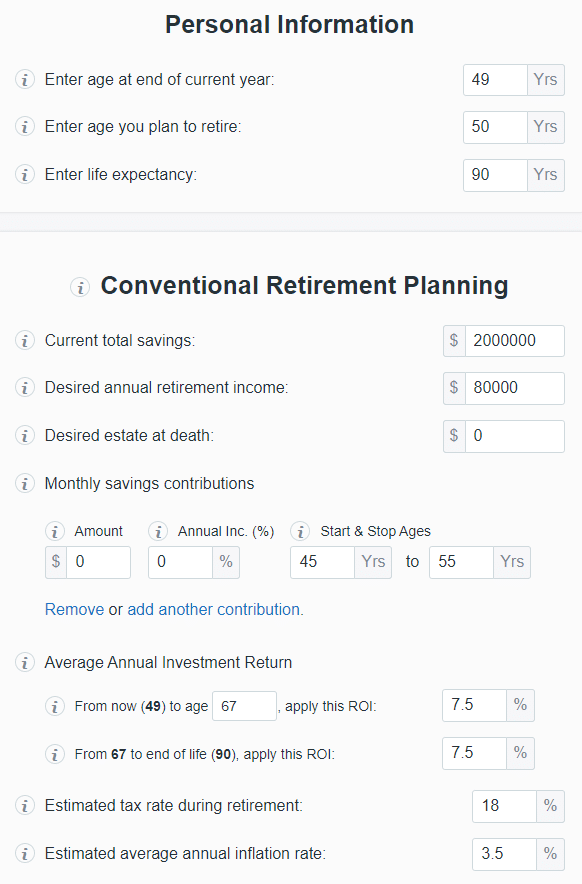

Monetary Mentor

This medium constancy software additionally dealt with many of the variables from my easy case. Like cFIREsim, it had the capability to deal with significantly extra modeling complexity than my easy case examine offered. Nevertheless, it additionally didn’t account for taxation of various account varieties. This explicit software additionally doesn’t have a immediate to account for funding bills.

The Monetary Mentor calculator runs projections primarily based on a gentle price of return all through the calculations, leading to a distinct feel and look with the outputs. This explicit calculator additionally gives tabular output (not proven) with yr by yr starting and ending balances in addition to the account development, additions, and spending that lead from one to the opposite.

Medium Constancy Cons

The most important weak spot of this class of calculators is the lack to supply a lot help to the person relating to taxes. The Monetary Mentor software explicitly requires you to estimate a tax-rate which runs via your total state of affairs. It does present a default. Nevertheless it might significantly over or underestimate your tax burden via your life cycle.

Taxes are addressed by cFIREsim on this single sentence in a tutorial on the location: “Vital Observe: It’s best to finances for some quantity of “taxes” in your spending. cFIREsim doesn’t bear in mind taxes in any means.” No additional steerage is supplied.

Darrow has written why taxes are one retirement quantity you possibly can’t afford to get incorrect. I’ve proven how wildly individuals can misestimate their retirement tax price and the way a lot it could differ from yr to yr primarily based in your particular person circumstances. After studying these two posts, you’ll get a way of the significance of this variable and why you wish to do higher than guessing at it.

The opposite weak spot frequent to medium constancy instruments is that in retaining the inputs easy, it’s not at all times intuitive how one variable will affect others. For instance, you possibly can mannequin promoting a house by getting into the proceeds as non-recurring earnings.

However will you then pay hire? If shopping for, will you pay money or get a mortgage? Will you progress to a brand new state with a distinct tax code? You need to keep in mind to account for these variables and others by yourself with out intuitive prompts.

Medium Constancy Execs

These instruments each supply appreciable will increase in performance, management, and customization of variables, and skill to mannequin extra complicated eventualities in comparison with low constancy calculators. On the similar time, the inputs and outputs are easy sufficient that they don’t seem to be overwhelming. I used to be in a position to enter my inputs and get helpful output from every in about 10 minutes apiece.

These calculators enable for fast if/then state of affairs evaluation of the identical variables that low constancy calculators do. Calculators on this class may mannequin elements corresponding to:

- Irregular massive purchases (automotive buy, bucket record journeys, dwelling remodels, and so on.)

- Irregular earnings (part-time retirement work, promoting an asset, staggered retirement dates for a pair, and so on.)

- Actual property methods (upsizing, downsizing, rental earnings, and so on.)

- Altering asset allocations over time.

Medium constancy instruments supply a big step up in performance and helpful insights that you would be able to’t get from a low constancy software. That performance comes with out the largest downside of excessive constancy calculators….complexity.

Excessive Constancy

Lastly, I ran my case examine via our affiliated excessive constancy calculators, NewRetirement PlannerPlus and Pralana Gold.

I additionally ran the state of affairs in RightCapital, the skilled planning software program I take advantage of with monetary planning purchasers.

My hope is that you would be able to get a way of the same performance between these excessive constancy calculators {and professional} software program. Additionally, you will shortly see the calls for on the person when utilizing these excessive constancy calculators in comparison with decrease constancy instruments.

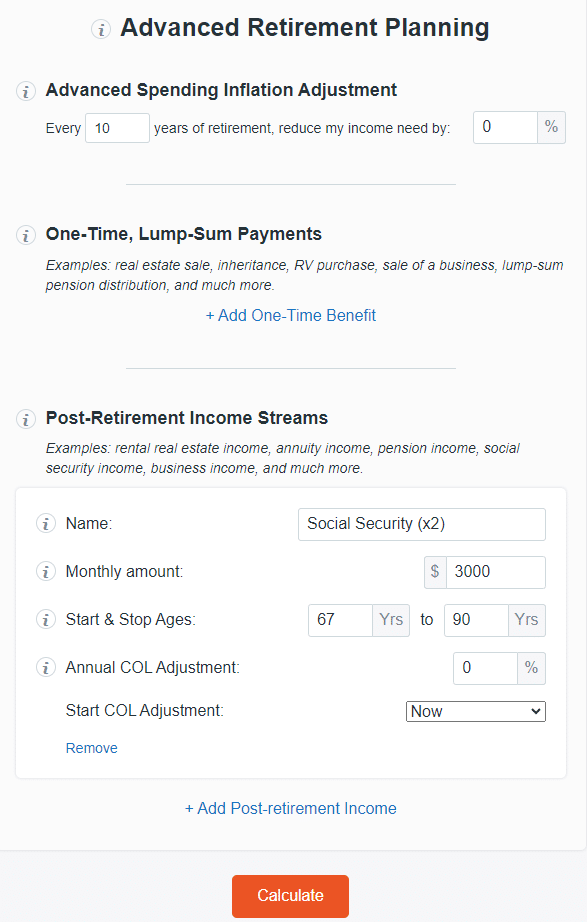

NewRetirement First Inputs

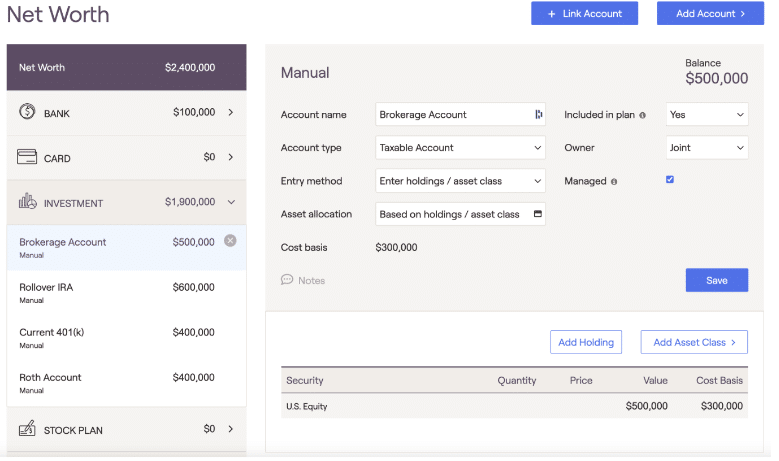

From the phrase go, the distinction between these excessive constancy instruments and decrease constancy calculators is clear. The primary enter in NewRetirement was to begin including accounts. The straightforward act of getting into my money required understanding the tax remedy of this holding and getting into optimistic and pessimistic charges of return. It additionally requires understanding whether or not I’m to enter nominal (what you see in your statements) vs. actual (inflation adjusted) returns.

This single, seemingly easy, enter took me longer to enter than working my state of affairs from begin to end on a low constancy calculator.

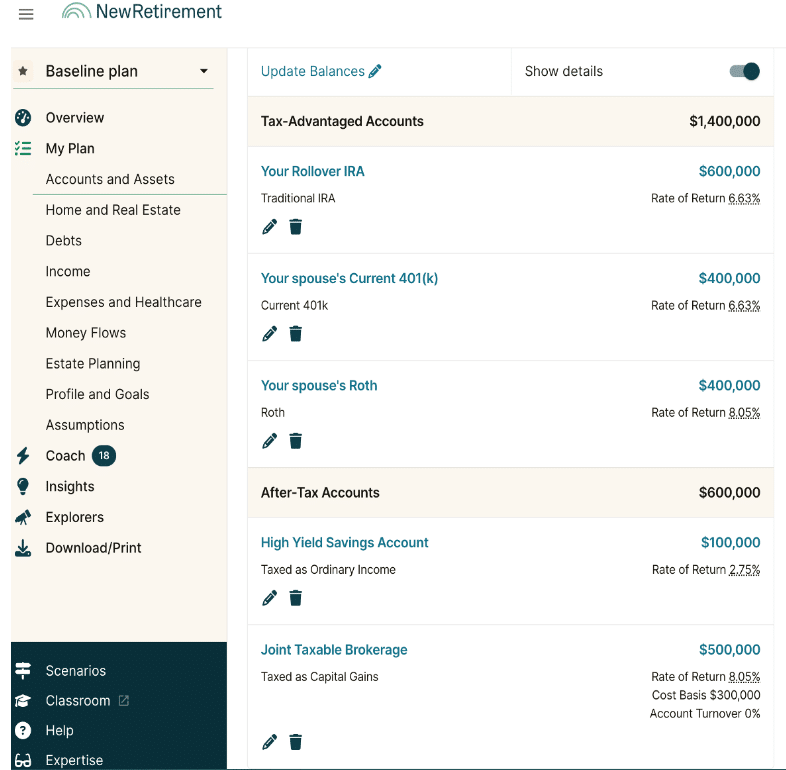

I then needed to enter every account individually and estimate each an optimistic and pessimistic price of return primarily based on the allocation of that specific account in addition to choosing the suitable tax remedy and price foundation primarily based on the holdings in taxable accounts.

Associated: The Advantages and Drawbacks of Taxable Accounts

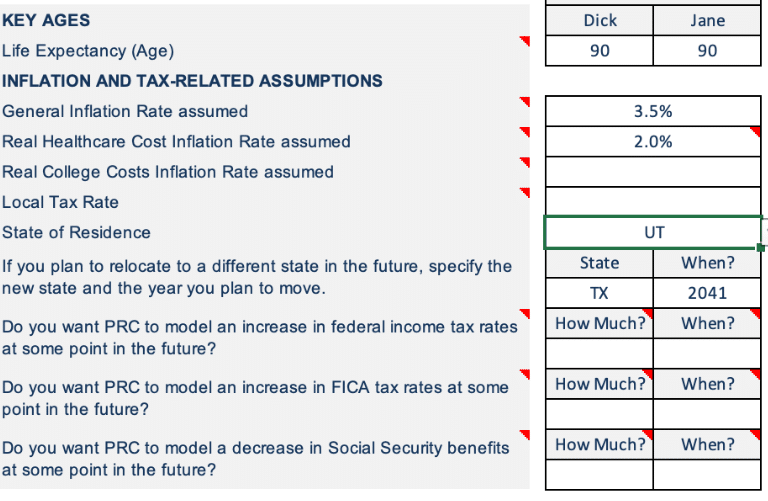

Pralana First Inputs

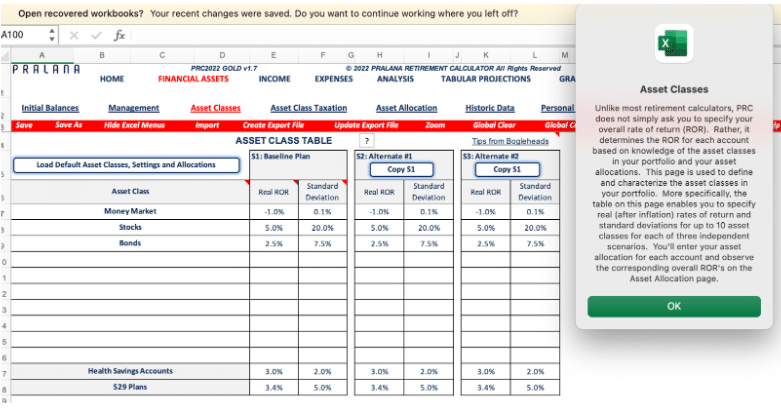

Pralana Gold equally permits detailed inputs. Pralana not solely permits you to create your personal inflation assumption, it will get you fascinated by completely different charges of inflation (healthcare and training) and permits completely different assumptions on for every on the primary enter web page. It not solely permits you to mannequin Social Safety and tax projections, it asks whether or not you wish to mannequin adjustments in charges and advantages sooner or later.

Like NewRetirement, Pralana requires you to decide on the speed of return on completely different asset lessons. On this case, your inputs are in actual (inflation adjusted) phrases.

All of that is clearly defined and assets are provided to help you. Even so, it is a appreciable demand on a brand new person of the software, and will shortly be overwhelming for somebody simply familiarizing themselves with retirement calculations.

Different Excessive Constancy Inputs

I’ll spotlight a couple of different inputs, using NewRetirement PlannerPlus, as a result of the person interface gives for higher screenshots to share. The variety of inputs and outputs obtainable on both software are far too many to go over each one on this weblog put up. I’ll spotlight just some.

Observe: We do have in depth critiques of each Pralana Gold and NewRetirement PlannerPlus on the location.

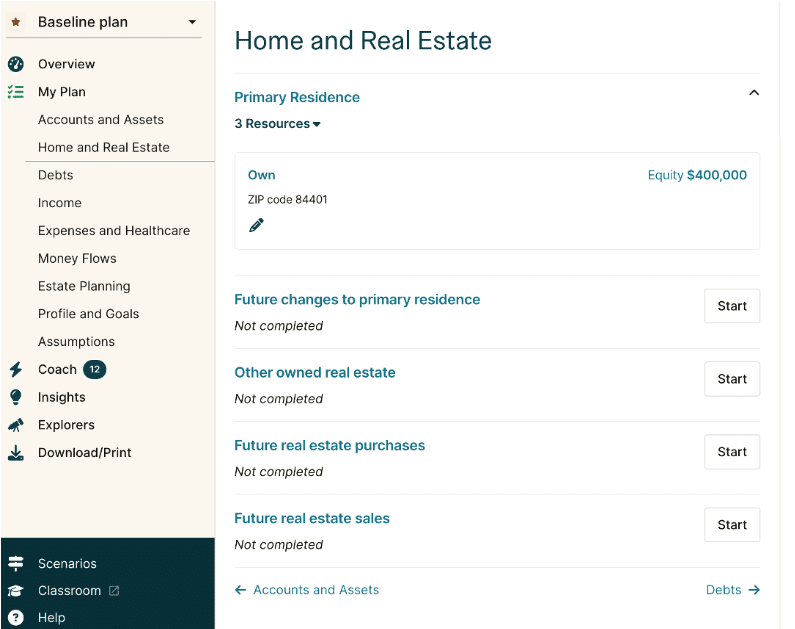

These instruments enable modeling actual property adjustments (downsizing, relocating to a distinct state, switching from proprietor to renter or vice versa, and so on.) in addition to modeling rental earnings.

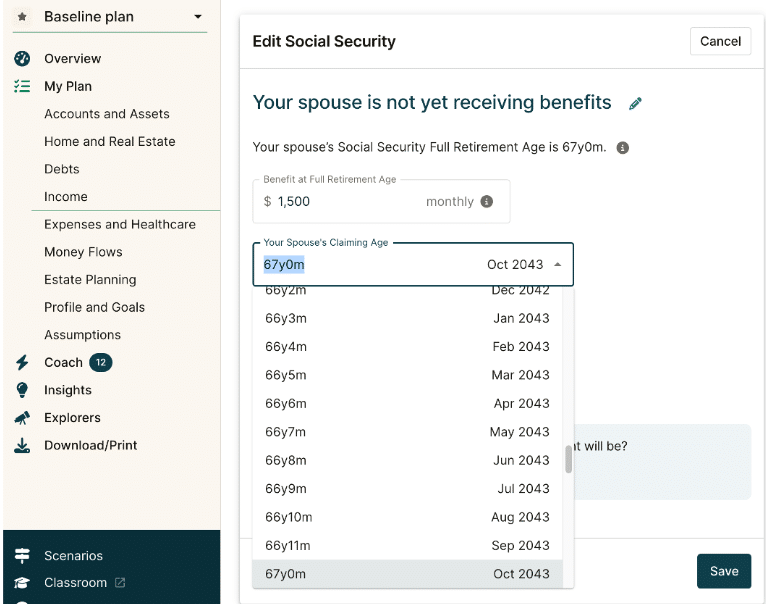

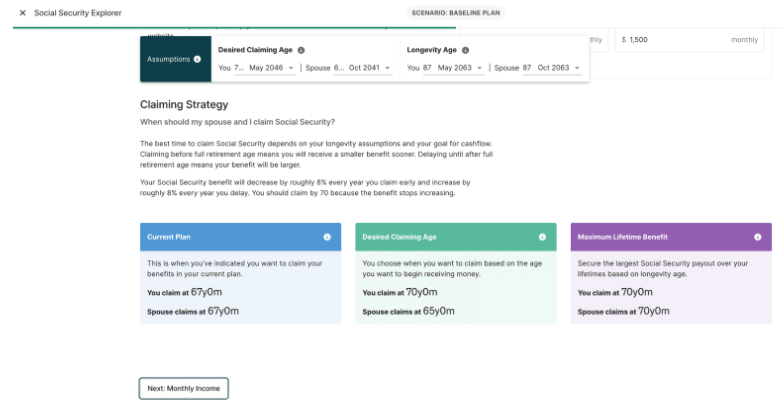

These instruments not solely allow getting into Social Safety values, however allow modeling completely different claiming methods with nice specificity.

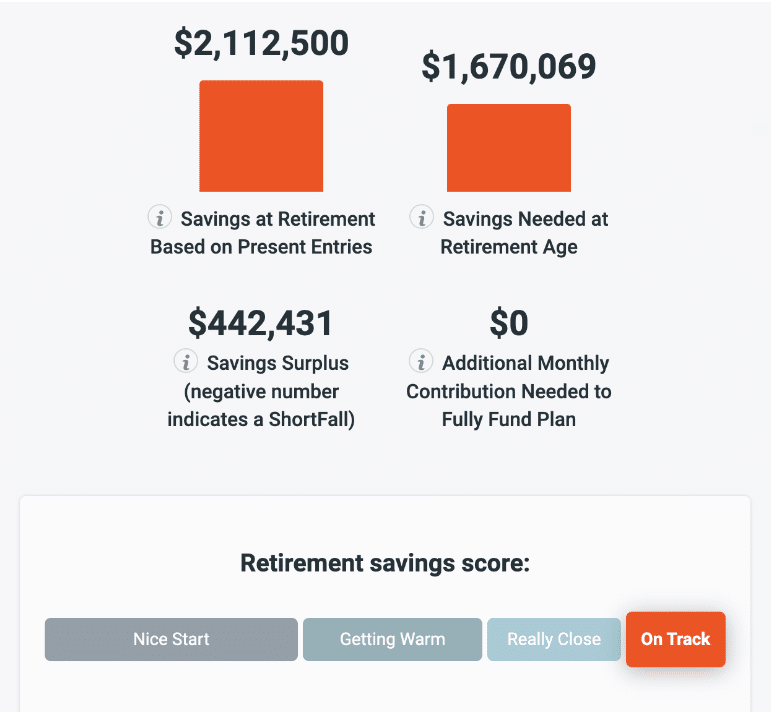

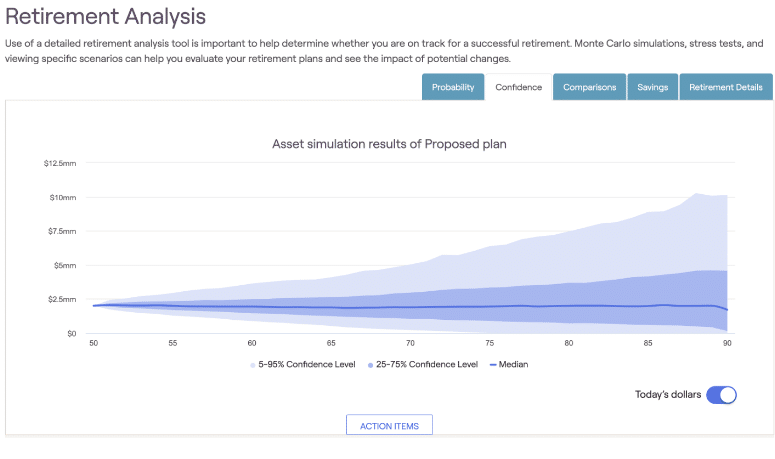

Excessive Constancy Outputs

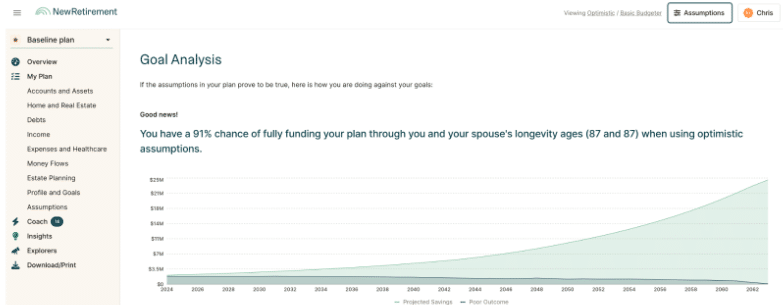

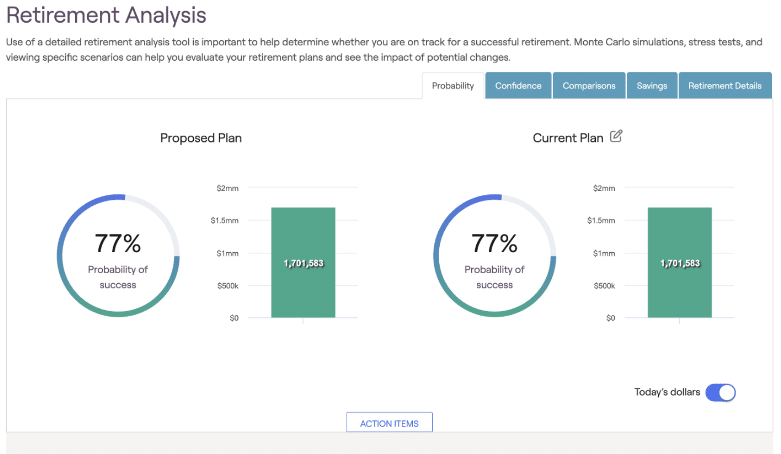

Very similar to low and medium constancy instruments, excessive constancy instruments finally provides you with a chance of retirement success usually expressed as a chance and median terminal account steadiness.

Nevertheless, the outcomes are rather more sturdy in comparison with low constancy instruments. They embody detailed tax projections yr by yr at each the federal and state ranges.

These instruments additionally present insights into actions like selecting the perfect Social Safety claiming technique and exploring the affect of Roth conversions.

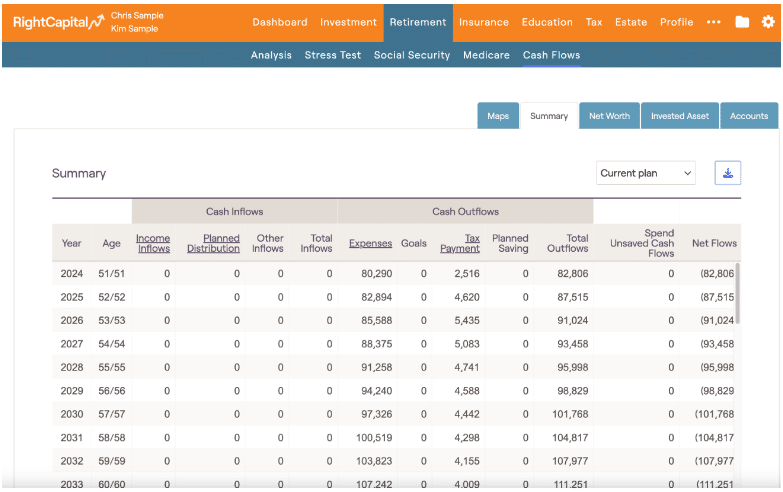

Skilled Software program Inputs and Outputs

Lastly, I’ll share what my case seems like when run via skilled software program. The person interface, the best way the information is entered, and the exact means knowledge is analyzed and offered in output differs from software to software. Every software has options that you could be like roughly than the opposite.

The take dwelling message I hope to offer is that there isn’t any “secret method” that skilled software program has in comparison with excessive constancy client grade retirement calculators. The bottom line is studying the software you finally select in and out. This fashion, you possibly can place an acceptable degree of belief within the outcomes so it’s helpful in bettering resolution making.

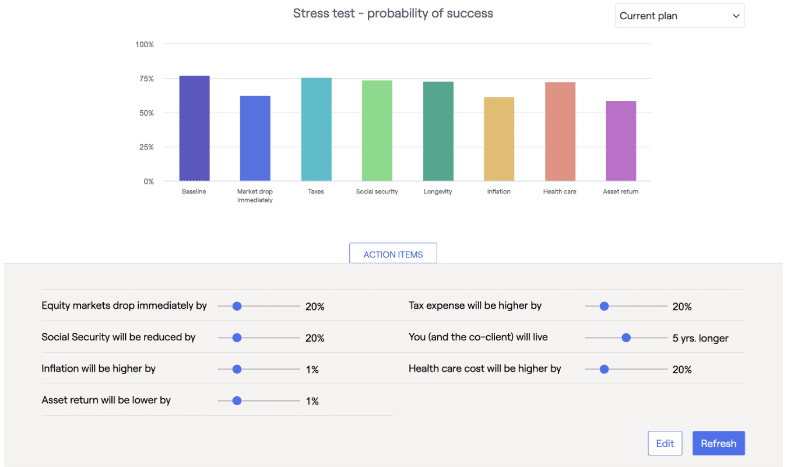

Excessive Constancy Strengths

A excessive constancy calculator is on par with skilled grade software program with reference to the eventualities it is ready to mannequin and the standard of the output it gives. To reiterate, every software has barely completely different options, person interface, and so on. that will make you want one higher than the opposite. As a category, these are highly effective instruments able to detailed modeling. They may help you make extra knowledgeable knowledge pushed selections.

Excessive Constancy Weaknesses

This isn’t to say that these instruments are with out weaknesses. They shouldn’t be neglected.

The primary is that these instruments will be difficult to navigate, even for individuals who have a agency grasp on the fundamentals of compounding, funding returns, inflation, their present spending, and so on. Somebody beginning out could shortly be overwhelmed and throw their palms up if beginning with excessive constancy calculators earlier than mastering fundamentals.

Second, not like low constancy calculators, excessive constancy instruments require some funding. The monetary price is minimal, round $100. The time funding is important.

Anticipate to spend no less than an hour getting a really feel for the software and getting into sufficient knowledge to get any significant output. The very best use of those instruments is an iterative course of the place you achieve mastery of the software program and your personal state of affairs over time.

Third, each calculator is making assumptions. Some are made by the software. Others are left as much as the person. It’s good to have the ability to select the way you wish to mannequin future funding returns, inflation charges, and adjustments to legal guidelines and social applications you assume will materialize. However do you acknowledge your biases and the challenges of predicting the longer term?

A crude easy software gained’t seemingly encourage nice confidence. Having a excessive constancy software that’s so highly effective and detailed can result in overconfidence in your outcomes. Even the perfect software with a educated person can’t predict the longer term.

The important thing variables that decide the end result to retirement calculations are lifespan, bills (together with taxes and well being care prices), funding returns, and inflation. All are unknowable. Humility is required.

Selecting the Proper Calculator

There is no such thing as a single “greatest” retirement calculator for everybody. Every affords completely different options and has its personal strengths and weaknesses. Calculator constancy is a good first filter to discovering the correct software to fulfill your wants.

Calling each low constancy and excessive constancy instruments “retirement calculators” is akin to calling steak knives and chainsaws “slicing gadgets.” On the most basic degree, that is true. In follow, they’re vastly completely different instruments. Select properly.

* * *

Precious Sources

- The Finest Retirement Calculators may help you carry out detailed retirement simulations together with modeling withdrawal methods, federal and state earnings taxes, healthcare bills, and extra. Can I Retire But? companions with two of the perfect.

- Free Journey or Money Again with bank card rewards and enroll bonuses.

- Monitor Your Funding Portfolio

- Join a free Empower account to realize entry to trace your asset allocation, funding efficiency, particular person account balances, web price, money movement, and funding bills.

- Our Books

* * *

[Chris Mamula used principles of traditional retirement planning, combined with creative lifestyle design, to retire from a career as a physical therapist at age 41. After poor experiences with the financial industry early in his professional life, he educated himself on investing and tax planning. After achieving financial independence, Chris began writing about wealth building, DIY investing, financial planning, early retirement, and lifestyle design at Can I Retire Yet? He is also the primary author of the book Choose FI: Your Blueprint to Financial Independence. Chris also does financial planning with individuals and couples at Abundo Wealth, a low-cost, advice-only financial planning firm with the mission of making quality financial advice available to populations for whom it was previously inaccessible. Chris has been featured on MarketWatch, Morningstar, U.S. News & World Report, and Business Insider. He has spoken at events including the Bogleheads and the American Institute of Certified Public Accountants annual conferences. Blog inquiries can be sent to chris@caniretireyet.com. Financial planning inquiries can be sent to chris@abundowealth.com]

* * *

Disclosure: Can I Retire But? has partnered with CardRatings for our protection of bank card merchandise. Can I Retire But? and CardRatings could obtain a fee from card issuers. Some or all the card affords that seem on the web site are from advertisers. Compensation could affect on how and the place card merchandise seem on the location. The positioning doesn’t embody all card firms or all obtainable card affords. Different hyperlinks on this web site, just like the Amazon, NewRetirement, Pralana, and Private Capital hyperlinks are additionally affiliate hyperlinks. As an affiliate we earn from qualifying purchases. Should you click on on certainly one of these hyperlinks and purchase from the affiliated firm, then we obtain some compensation. The earnings helps to maintain this weblog going. Affiliate hyperlinks don’t improve your price, and we solely use them for services or products that we’re aware of and that we really feel could ship worth to you. Against this, we’ve restricted management over many of the show advertisements on this web site. Although we do try to dam objectionable content material. Purchaser beware.