")

{kind=link}

Time Technoplast Ltd – Bringing Polymers to Life

Integrated in 1992, Time Technoplast Ltd. is a number one polymer and composite product firm. The corporate has established its place within the trade with the launch of a number of first in India merchandise akin to PE drums, plastic gas tanks for industrial autos, lithium batteries, spray suspension methods and so forth. It’s a multinational conglomerate with operations in Bahrain, Egypt, Indonesia, Malaysia, U.A.E, Taiwan, Vietnam, Saudi Arabia & USA and India. As of FY24, the corporate’s R&D consists of 35 consultants and operates greater than 40 manufacturing amenities throughout the globe.

Merchandise and Providers

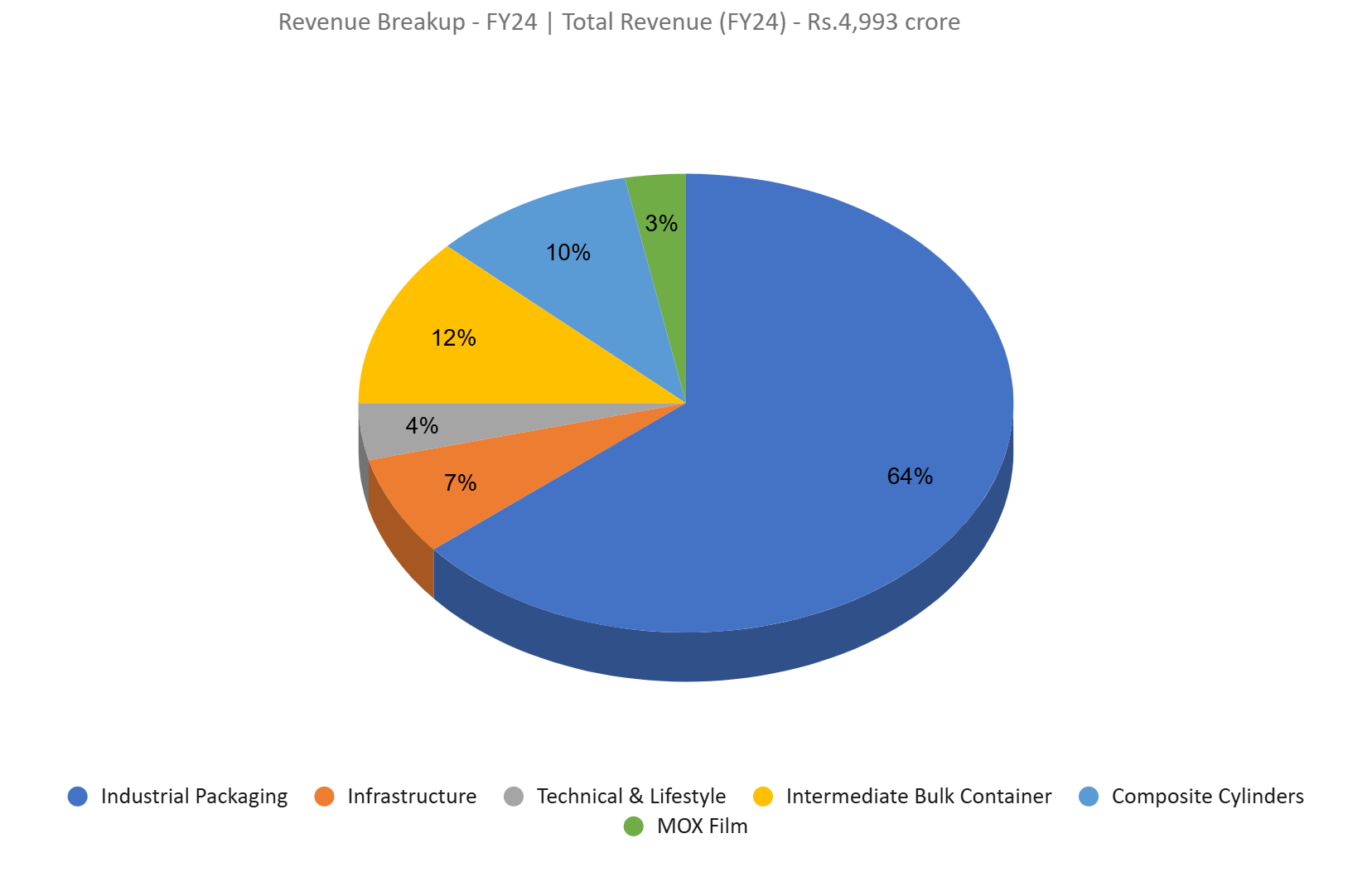

The corporate’s numerous product line contains of intermediate bulk container (IBC), end-to-end materials dealing with merchandise akin to containers, plastic crates and pallets, mox movies, cross laminated movies, composite cylinders akin to LPG cylinders, CNG cylinders and oxygen/scba cylinders, industrial packaging merchandise like drums, containers, conipails and PET sheets, pipes for infrastructure tasks, automotive parts akin to rain flaps, gas tanks, air ducts, life-style merchandise akin to mats, furnishings, bins and protecting face shields.

Subsidiaries: As of FY24, the corporate has 8 subsidiaries and one three way partnership firm.

Funding Rationale

- Diversified operations – The corporate boasts a various portfolio of merchandise that serve a broad spectrum of industries. Its “established merchandise” vary gives modern packaging options for sectors akin to specialty chemical substances, FMCG, textiles, agriculture, development chemical substances, paints and inks, and prescribed drugs. Moreover, the corporate’s “value-added” choices embrace IBCs, composite merchandise like LPG cylinders, CNG cascades, and MOX movies. Within the IBCs enterprise, the corporate is the most important and main participant in most international locations it operates in. Past these, the corporate additionally helps industries akin to railways, photo voltaic vitality, automotive, and life-style merchandise. Its presence throughout a number of sectors enhances resilience to market fluctuations, ensures secure income streams, and permits the leveraging of trade insights for steady innovation and development.

- Potential of composite merchandise – The corporate goals to spice up the proportion of margin-accretive, value-added, and composite merchandise in its portfolio, with a concentrate on CNG, LPG, and hydrogen. It has obtained approval to fabricate the high-pressure Kind 4 composite cylinder prototype for hydrogen, turning into the primary firm in India to safe this approval. As well as, it has efficiently developed the Kind-III Composite Cylinder for Respiration Air/Medical Oxygen, marking the primary domestically produced cylinder for this goal. The corporate can be engaged on the event of composite hearth extinguishers and composite water heaters. In Q2FY25, sturdy demand for its Kind-4 Composite Cylinders for CNG cascades resulted in an order guide valued at Rs.185 crore. The corporate’s subsidiary NED Vitality Ltd. is creating E-rickshaw batteries with the prototype already developed and submitted for approval.

- Q2FY25 – The corporate generated a income of Rs.1,372 crore, attaining a rise of 15% as in comparison with the Rs.1,195 crore of Q2FY24. Volumes elevated by an general 17% in the course of the quarter. EBITDA improved by 18% YoY, from Rs.167 crore to Rs.197 crore. Web revenue stood at Rs.98 crore, an upsurge of 40% from Rs.70 crore of Q2FY24. The worth-added merchandise grew by 21% in the course of the quarter, whereas established merchandise grew by 13%.

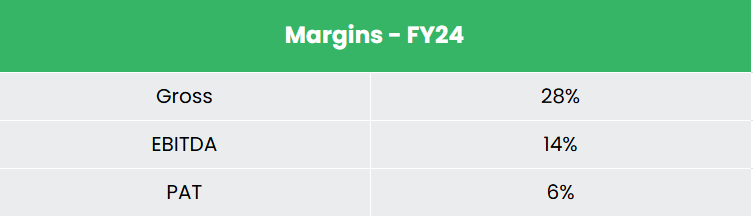

- FY24 – The corporate generated income of Rs.4,993 crore, a rise of 16% in comparison with FY23 income. Working revenue is at Rs.705 crore, up by 21% YoY. The corporate posted web revenue of Rs.316 crore, a leap of 41% YoY.

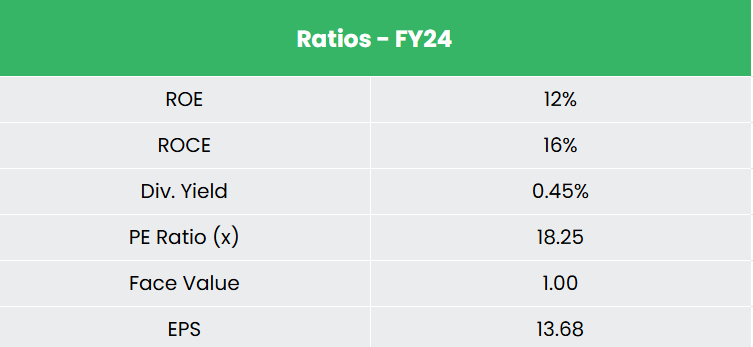

- Monetary efficiency – The corporate has generated income and web revenue CAGR of 18% and 43% over the interval of three years (FY21-24). Common 3-year ROE & ROCE is round 11% & 14% for FY21-24 interval. The corporate has a debt-to-equity ratio of 0.29.

Trade

Packaging trade stands because the fifth largest trade in India and the federal government is specializing in a number of initiatives that concentrate on sustainable manufacturing strategies. The growth of the center class, enhancements in provide chain infrastructure, and the rise of e-commerce platforms are main elements driving the packaging trade’s development trajectory. The worldwide Packaging Market measurement is estimated to be USD 1.14 trillion in 2024, projected to succeed in USD 1.38 trillion by 2029, rising at a CAGR of three.89% (20242029). The India Packaging Market measurement is estimated at USD 84.37 billion in 2024, and is anticipated to succeed in USD 142.56 billion by 2029, rising at a CAGR of 11.06% (20242029).

Development Drivers

- 100% International Improvement Funding (FDI) allowed beneath automated route within the packaging sector.

- Pushed by the expansion of allied industries akin to shopper items, prescribed drugs, meals processing, manufacturing trade, FMCG, healthcare and so forth.

- Initiatives to advertise using LNG & CNG by the federal government akin to speedy growth of fuel infrastructure together with pure fuel grid, liquefied pure fuel (LNG) import terminals and metropolis fuel distribution (CGD) community within the nation.

Peer Evaluation

Opponents: Supreme Industries Ltd

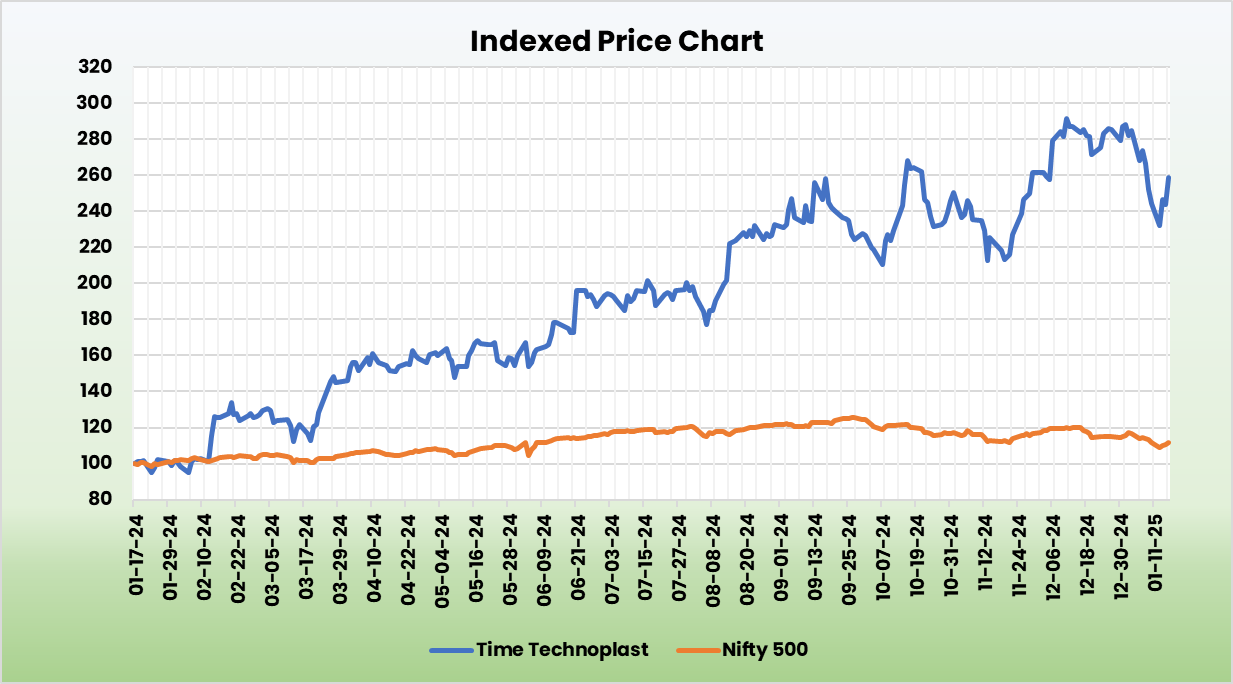

In comparison with its competitor, Time Technoplast is undervalued with a constant development in income and secure returns from the capital invested capital.

Outlook

The corporate has given a income development steering of 15% for the following 2-3 years. It has put aside a capex allocation of Rs.180 to Rs.200 crore for FY25. The corporate aspires to be the most important composite product firm within the nation. It has a pipeline of excessive enterprise potential merchandise for launch. The brand new merchandise are anticipated to enhance margins and earnings potential. Additionally it is endeavor automation and reengineering initiatives in its present amenities to extend productiveness with a subsequent discount in in price. Additionally it is concentrating on to extend the share of value-added merchandise from present 27% to 35% within the subsequent 2-3 years. The corporate goals to turn into a debt-free firm by FY26. It’s sustaining a robust stability sheet with web money stability of Rs.902 crore (as of Q2FY25).

Valuation

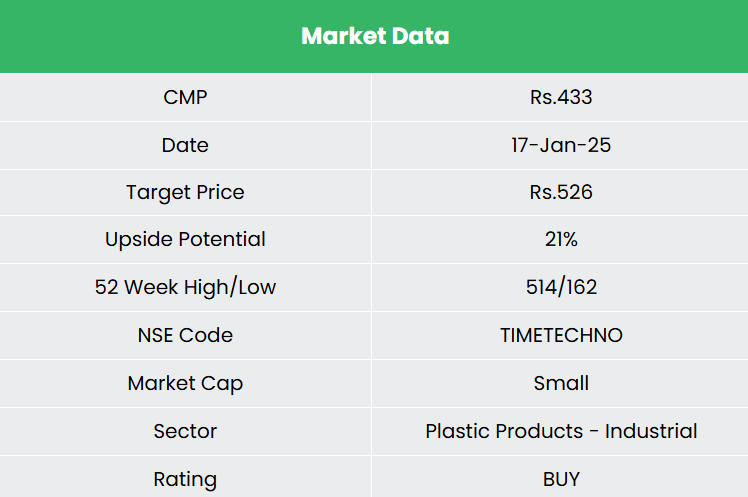

We count on the corporate to maintain its development momentum given its first mover benefit backed by sturdy execution capabilities. We advocate a BUY ranking within the inventory with the goal worth (TP) of Rs.526, 23x FY26E EPS.

Threat

- Launch of latest merchandise – Delay within the launch or failure of latest merchandise might influence profitability.

- Change in regulatory surroundings – The corporate operates in an trade with stricter regulatory surroundings (e.g., restrictions on using plastic), which might have an effect on its operations.

Word: Please be aware that this isn’t a suggestion and is meant just for instructional functions. So, kindly seek the advice of your monetary advisor earlier than investing.

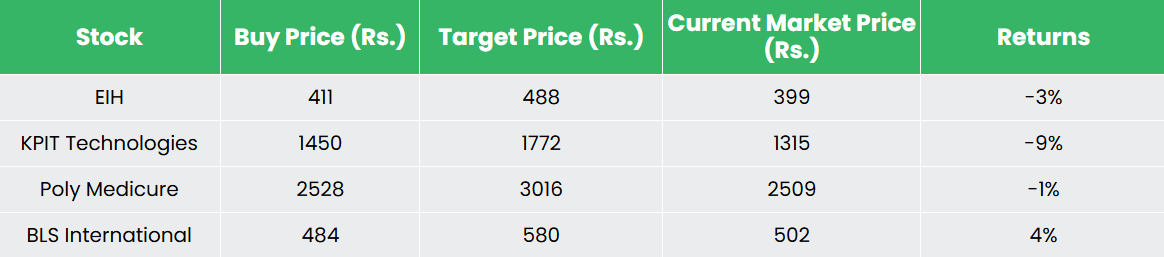

Recap of our earlier suggestions (As on 17 January 2024)

Different articles it’s possible you’ll like