{kind=link}

Vijaya Diagnostic Centre Ltd – Empowering well being by diagnostics

Established in 1981 and headquartered in Hyderabad, Vijaya Diagnostic Centre Ltd. is a number one supplier of diagnostic companies in India providing a variety of pathology and radiology companies. As of FY24, the corporate operates an enormous community of 149 diagnostic centres (39 hubs and 110 spokes) and 21 reference laboratories throughout 23 cities, together with Telangana, Andhra Pradesh, Maharashtra, Karnataka, West Bengal and the Nationwide Capital Area. The corporate’s crew of 250+ medical doctors, 1,400+ technical employees and 1,100+ help employees has served over 100 million + prospects (as of FY24).

Merchandise and Companies

Vijaya provides diagnostics companies comparable to CT scan, MRI scan, ultrasound, MRI-3T, x-ray in numerous fields of medication comparable to medical pathology, microbiology, haematology, serology, biochemistry, molecular diagnostics, cardiology, gastroenterology and so forth.

Subsidiaries: As of FY24 the corporate has 4 subsidiaries and no affiliate corporations/joint ventures.

Funding Rationale

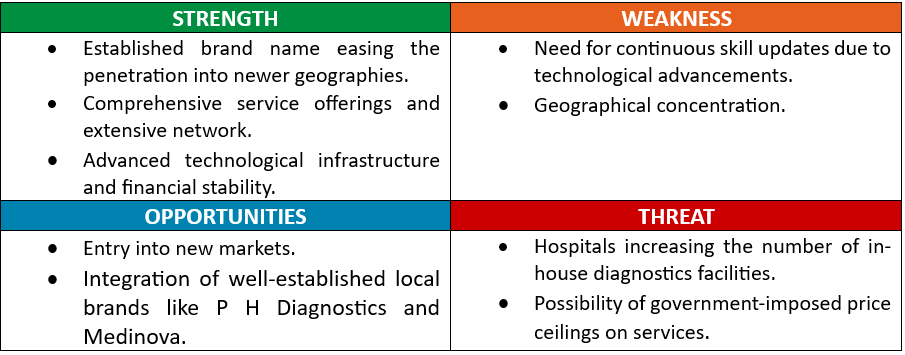

- Strategic enterprise initiatives – The corporate has acquired a 100% stake in PH Diagnostics, the most important B2C built-in diagnostics chain in Pune, which operates 3 hubs, 3 spokes, and 12 assortment centres. Following the acquisition, the corporate launched its first spoke centre at Pimple Saudagar beneath the Vijaya PH model throughout Q3FY25. Moreover, Vijaya has proposed the merger of Medinova Diagnostic Companies Restricted with the corporate. Medinova offers a variety of diagnostic companies, together with pathological investigations, radiology and imaging, and diagnostic cardiology. The corporate can be specializing in progress by forming partnerships with corporates for worker well being checkups. Moreover, it’s investing in enhancing its technological capabilities throughout each present and new amenities, as evidenced by the introduction of PET-CT on the Tirupati centre and 3T MRI and CT scans at a brand new facility in Nizamabad.

- Penetration to newer geographies – To increase its buyer base, the corporate is establishing its presence in new geographies. In Andhra Pradesh and Telangana, it’s focusing on extra Tier 1 and Tier 2 cities. Current successes in newly entered areas comparable to Tirupati, Rajahmundry, and Mahbubnagar spotlight the effectiveness of this technique. Moreover, the corporate has launched its first hub in Kolkata, the place it goals to copy the hub-and-spoke mannequin. The corporate has additionally targeted on the western Indian market, beginning with the acquisition of PH Diagnostics, and has just lately entered Karnataka with a brand new hub in Kalaburagi.

- Q3FY25 – The corporate reported a income of Rs.169 crore marking a rise of 27% in comparison with the Rs.133 crore income of Q3FY24. Natural progress excluding the income from PH is at 20%. EBITDA stood at Rs.67 crore in opposition to the Rs.52 crore of Q3FY24, a progress of 29% YoY. Web revenue stood at Rs.35 crore which is a progress of 35% as in comparison with the Rs.26 crore of the identical interval within the earlier yr. Notably, the corporate achieved margin enlargement through the quarter with EBITDA margin bettering from 39% to 40% and internet revenue bettering from 20% to 21%. Through the quarter affected person footfall elevated by 19% to 1.05 million and income per footfall elevated by 7%.

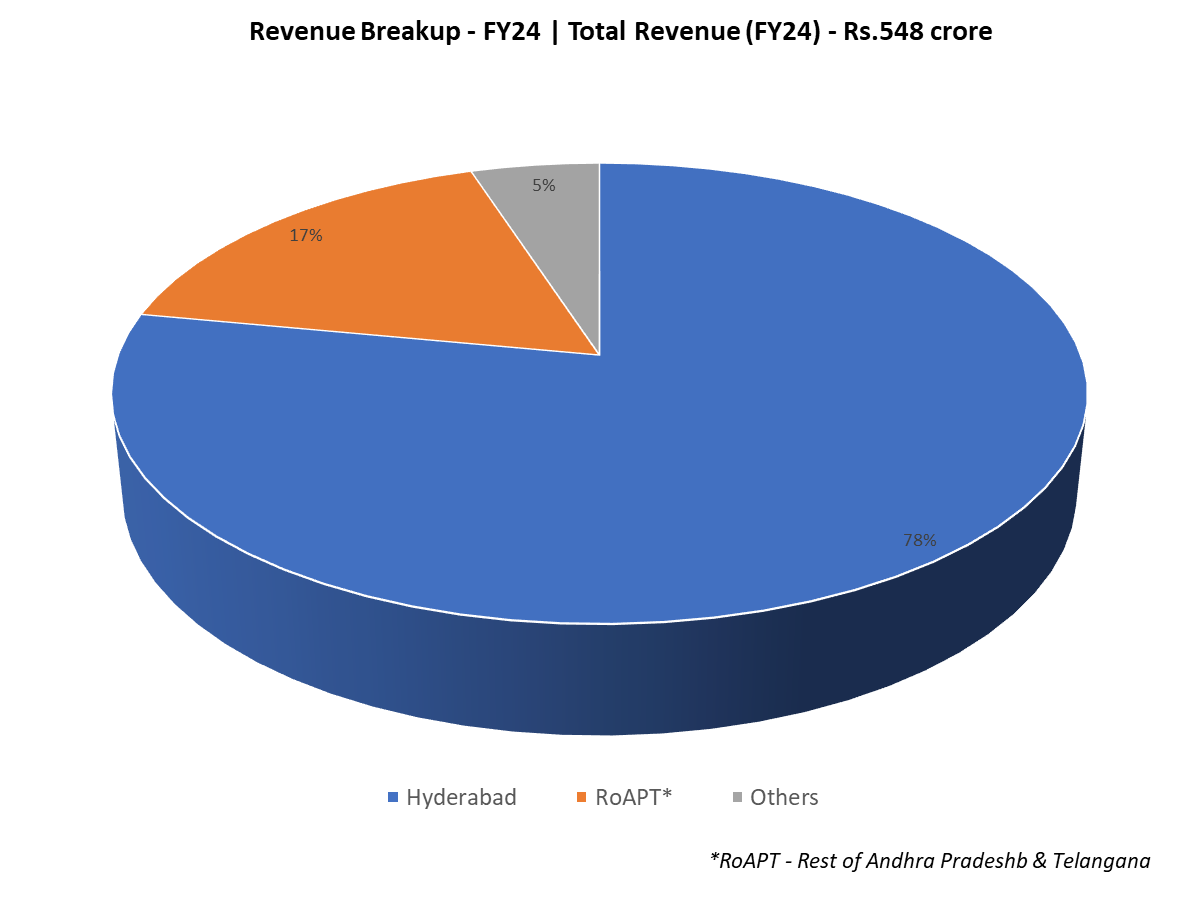

- FY24 – The corporate generated income of Rs.548 crore throughout FY24, a rise of 19% in comparison with the FY23 income. EBITDA was at Rs.221 crore, up by 21% YoY. The corporate reported internet revenue of Rs.119 crore, a rise of 40% YoY.

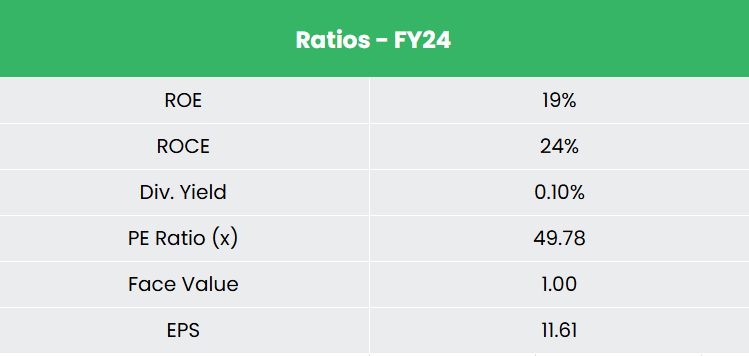

- Monetary Efficiency – The income and internet revenue CAGR of the corporate for the previous 3 years is round 13% and eight% between FY21-FY24 with the TTM progress being 29% and 24%. The three-year common ROE and ROCE for the corporate is round 20% and 22% for the previous 3 years. The corporate has a strong capital construction with a debt-to-equity ratio of 0.40.

Trade

The Indian healthcare sector, one of many nation’s largest when it comes to each income and employment, is increasing quickly attributable to enhanced protection, improved companies, and growing investments from each private and non-private sectors. The affordability of medical companies has fuelled the expansion of medical tourism, drawing sufferers from across the globe. Elements comparable to rising incomes, an ageing inhabitants, larger well being consciousness, a shift towards preventive care, and wider medical insurance protection are anticipated to drive demand for healthcare companies sooner or later. India’s hospital market which was valued at US$ 98.98 billion in 2023 is projected to develop at a CAGR of 8.0% from 2024 to 2032, reaching an estimated worth of US$ 193.59 billion by 2032. The nation has additionally grow to be one of many main locations for high-end diagnostic companies with super capital funding for superior diagnostic amenities, thus catering to a larger proportion of the inhabitants.

Development Drivers

- Rising healthcare consciousness, rising demand for preventive healthcare and developments in diagnostics applied sciences.

- India’s Union Finances 2025-26 emphasizes reworking the healthcare sector by elevated digital infrastructure and a revised well being expenditure of Rs.89,287 crore (US$ 10.70 billion), aiming to boost accessibility and innovation in healthcare companies.

- Authorities initiatives comparable to Ayushman Bharat, MedTech Mitra, The Pradhan Mantri Jan Arogya Yojana and so forth, aimed to boost healthcare high quality, ease of doing enterprise and decreased import dependence whereas fostering indigenous growth of inexpensive and high-quality diagnostics gadgets.

Peer Evaluation

Opponents: Dr Lal Pathlabs Ltd, Thyrocare Applied sciences Ltd, and so forth.

As in comparison with the above rivals, along with producing a constant progress in income and secure returns from the invested capital, the corporate is ready to obtain increased revenue margins highlighting its potential for increased earnings enlargement.

Outlook

The corporate is executing a strategic roadmap to increase its community by each natural and inorganic progress, with a main concentrate on growing quantity. Throughout Q3FY25, the income progress was primarily pushed by quantity enlargement in radiology and pathology section. It has already commissioned 9 hubs through the 9MFY25 and is on monitor to fee 9 extra hubs and 6 spokes in subsequent 6 months. The newly launched centres are reaching breakeven inside a span of 2-3 quarters, reflecting robust buyer model choice. The corporate can be capable of supply machines from its distributors on a pay-per-use foundation, indicating the robustness of its enterprise methods. A capex plan of Rs.200-220 crore over the subsequent two years, primarily funded by inner accruals, is in place. With 93% of income from B2C, the corporate is well-positioned for margin enlargement. Moreover, strategic acquisitions are anticipated to consolidate the corporate’s market place and creating synergies in operations.

Valuation

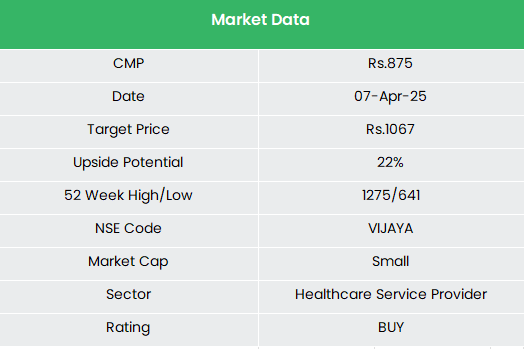

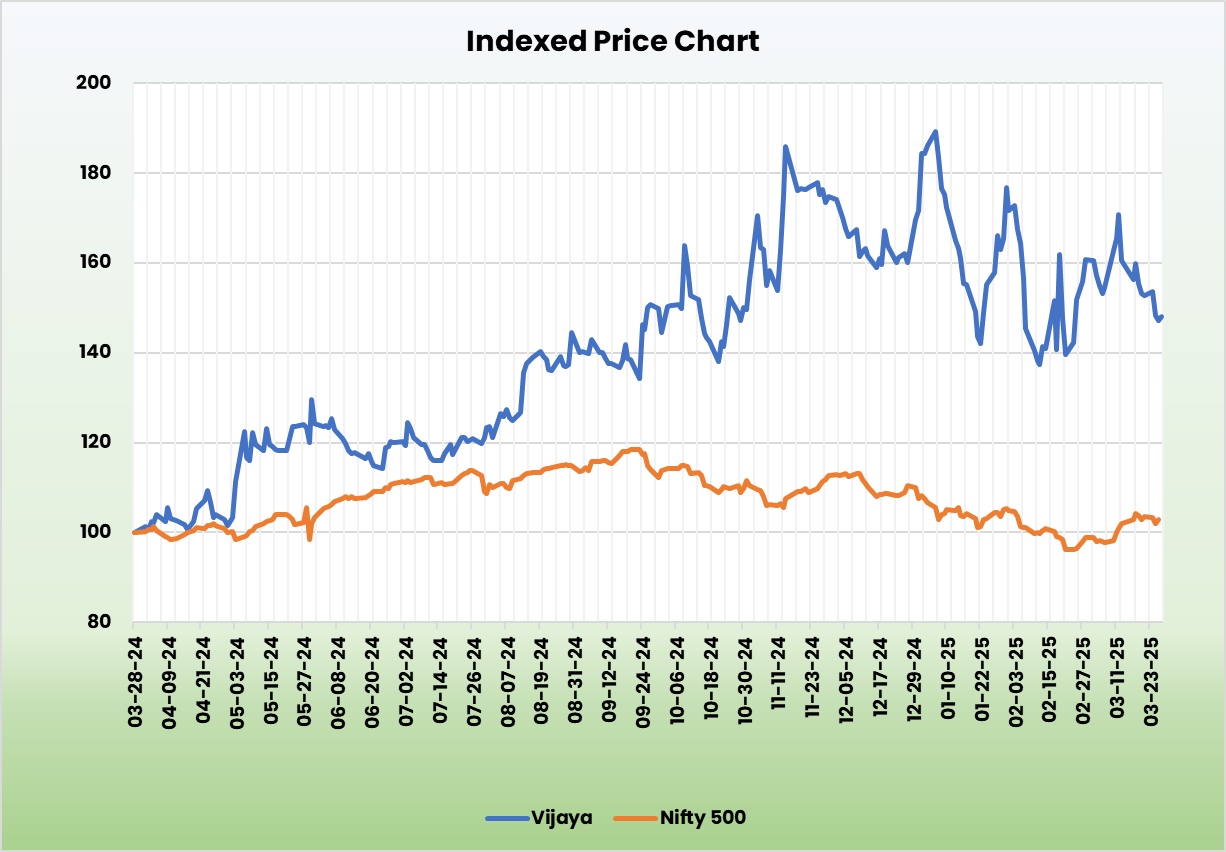

We imagine Vijaya’s aggressive community enlargement efforts will assist the corporate speed up its progress momentum. We suggest a BUY ranking within the inventory with the goal value (TP) of Rs.1,067, 53x FY26E EPS.

SWOT Evaluation

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please word that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles chances are you’ll like