{kind=link}

Effectively, right here we’re. It took longer than anticipated, however mortgage charges have lastly strung collectively a good rally after practically three years of will increase.

They fell under year-ago ranges per week or two in the past, per Freddie Mac, and took one other massive leg down after a softer-than-expected jobs report on Friday.

As for why, fewer new hires, elevated unemployment, and slowing wage progress all level to a slowing financial system. And rates of interest are likely to drop when the financial system cools.

As well as, the Fed is predicted to pivot and start slicing charges, which may act as one other tailwind for decrease mortgage charges.

This has many considering we’ll see one other surge of residence purchaser demand, and probably a giant soar in residence costs. However is it true?

Do Decrease Curiosity Charges Really Improve Dwelling Costs?

It’s solely logical on the floor. If one thing folks need turns into cheaper in a single day, demand for it ought to hypothetically enhance.

And if demand will increase, the value may rise as provide decreases, particularly if there are already too few houses on the market.

But when that had been true for single-family houses, why didn’t asking costs crash over the previous 12 months and alter?

In spite of everything, charges on the 30-year mounted mortgage practically tripled from its report lows within the mid-2s in early 2021 earlier than peaking at simply above 8% final fall.

Utilizing the identical logic above, residence costs would certainly nosedive as consumers fled the market, main to an enormous provide glut.

As an alternative, residence value appreciation merely cooled off and residential costs continued to extend in most components of the nation.

In actual fact, if you happen to have a look at many residence value indices, we have now new all-time excessive residence costs just about each month.

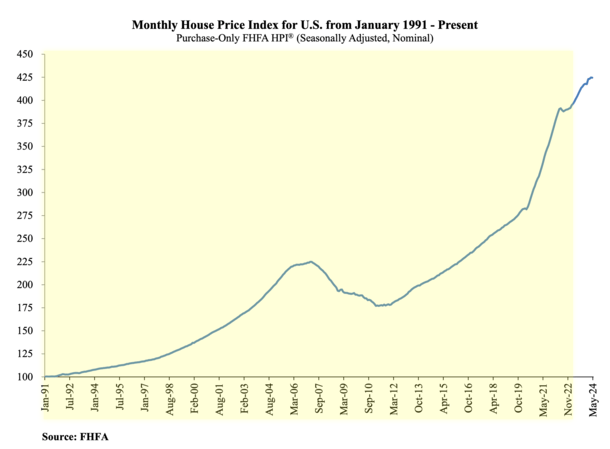

Dwelling Costs Continued to Rise as Mortgage Charges Practically Tripled

Simply take this chart from the Federal Housing Finance Company (FHFA), which oversees Fannie Mae and Freddie Mac.

Their newest report launched on July thirtieth revealed that residence costs elevated a strong 5.7% from Might 2023 to Might 2024.

Nonetheless, residence costs had been flat month-to-month from April after rising 0.3% a month earlier.

Nonetheless, if you happen to have a look at the chart, you’ll see that residence costs didn’t gradual a lot as mortgage charges started their ascent at the beginning of 2022.

There was a quick pause because the housing market digested the near-tripling in charges, however then costs continued their ascent unabated.

So if we wish to argue that there’s an inverse relationship between charges and costs, this previous couple of years wouldn’t be an excellent instance of that.

All we’ve actually seen is a constructive correlation between charges and costs, by which BOTH have risen collectively.

And now that mortgage charges seem poised for a little bit of a rally, ought to we ignore that and say they’ve a unfavourable relationship?

Can we are saying costs ought to have fallen when charges went up, however now that charges are falling they need to go up much more?

Perhaps There’s Simply Not A lot of a Correlation at All

As an alternative of attempting to invent a relationship between mortgage charges and residential costs, possibly we should always simply come to phrases with the actual fact there isn’t a robust one.

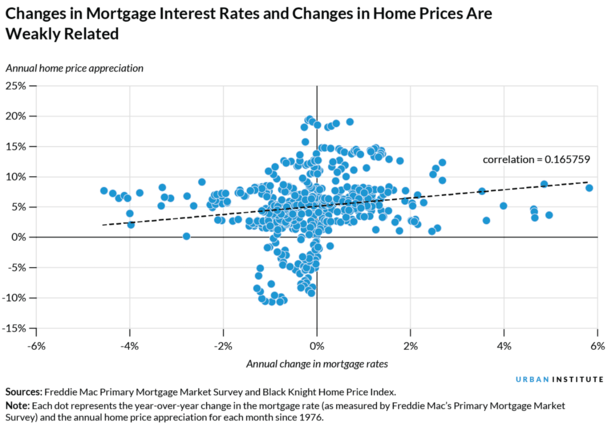

And there’s nothing mistaken with that. When you have a look at historical past, adjustments in mortgage charges and residential costs are weakly associated, this in keeping with the City Institute.

I’ve posted this chart earlier than, however right here it’s once more if you happen to don’t imagine it. You’ll see all sorts of combos of annual mortgage fee and residential value adjustments.

These little dots received’t make it simple to make the argument that when mortgage charges fall, residence costs rise. Or vice versa.

As an alternative, you’ll see situations after they rose collectively, fell collectively, or generally, to suit the favored narrative that isn’t essentially true, went in reverse instructions.

In fact, nominal residence costs (not adjusted for inflation) hardly ever go down to start with, so we don’t even have that many examples to have a look at.

Why Would Dwelling Costs Fall If Mortgage Charges Bought Cheaper?

Effectively, simply have a look at the financial system…certain, mortgage charges are essential as a result of they’ll make a big effect on affordability.

The decrease the speed, the extra a house purchaser can afford, all else equal. In actual fact, a 1% drop in mortgage charges is value an 11% lower in value.

However this simplistic view ignores money consumers. And it ignores the monetary well being of potential residence consumers who must get authorized for a mortgage.

Simply take into account the previous couple of days. The inventory market has gotten hammered, with the Dow Jones falling greater than 1,000 factors immediately and the Nasdaq off practically 600 factors.

This sell-off was sparked by issues in regards to the well being of the financial system, with weaker information anticipated to usher in Fed fee cuts.

There’s an excellent likelihood that softer information will likely be accompanied by decrease mortgage charges too.

Merely put, indicators of a slowing financial system improved the percentages for a Fed fee lower, and likewise gave bonds a lift, that are a secure haven for buyers when instances get powerful.

But when households are in worse form due to mentioned information, you’re going to have fewer residence consumers on the market. You possibly can even have extra sellers, even perhaps distressed ones.

Taken collectively, we would have a state of affairs the place the provision of houses on the market rises and costs fall, regardless of a giant enchancment in mortgage charges.

So sure, residence costs may the truth is go down, even when mortgage charges are decrease!

However that’s not a foregone conclusion both, and can seemingly be extremely variable primarily based on financial power and particular person market dynamics all through the nation.

The primary message right here is there’s no robust correlation any which manner. Considering in any other case may merely result in disappointment.

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and current) residence consumers higher navigate the house mortgage course of. Comply with me on Twitter for decent takes.